Yen slides as BoJ cuts growth forecastThe Japanese yen continues to lose ground and is sharply lower on Thursday. In the European session, USD/JPY is trading at 144.36, up 0.92% on the day. Earlier, the yen weakened to 144.74, its weakest level since April 10.

There were no surprises from the Bank of Japan, which maintained its key interest rate at 0.5% in a unanimous vote. The BoJ has signaled that it plans to continue hiking rates and normalize policy, but the turmoil caused by US President Trump's tariff policy may delay the next rate increase until after the summer.

The BoJ board cut its growth and inflation forecasts in its quarterly outlook report. The growth forecast for the fiscal year ending March 2026 was slashed to 0.5% from 1.1% in January and inflation is not expected to remain sustainable at 2% until the second half of 2026, a year later than in the January forecast.

The forecast noted that US tariffs would dampen Japan's economy by weighing on global trade and consumer and businesses confidence would be impacted due to the "heightened uncertainties" over the tariffs.

The markets expected a soft US GDP release for Q1 but the 0.3% q/q decline was well below the market estimate of 0.2%. This followed a strong 2.4% gain in the fourth quarter of 2024. The surprise decline was driven by Trump's tariffs, as imports surged ahead of the tariffs taking effect and consumer spending declined.

The weak GDP figure raised the probability of further rate cuts and the markets are looking for up to four rate cuts before the end of the year. The Fed is in a wait-and-see mode, with little chance of a cut in May, but further economic deterioration could force the Fed to cut in June.

GDP

German inflation higher than expected, Euro dipsThe euro is calm on Wednesday. In the North American session, EUR/USD is trading at 1.1334, down 0.45% on the day.

Germany's inflation rate dropped to 2.1% y/y in April, down from 2.2% in March but above the market estimate of 2.0%. This was the lowest level in seven months, largely driven by lower energy prices.

The more significant story was that core CPI, which excludes energy and food and is a more reliable indicator of inflation trends, rose to 2.9% from 2.6%. This will be of concern to policymakers at the European Central Bank, as will the increase in services inflation. The ECB has to balance the new environment of US tariffs and counter-tariffs against the US, which will raise inflation, along with the strong rise in the euro and fiscal stimulus which will boost upward inflationary pressures.

The ECB will be keeping a close look at Friday's eurozone inflation report, which is expected to follow the German numbers. Headline CPI is projected to drop to 2.1% from 2.2%, while the core rate is expected to rise to 2.5% from 2.4%. The central bank would prefer to continue delivering gradual rate cuts in order to boost anemic growth, but this will be contingent on inflation remaining contained.

The markets were braced for soft US numbers but the data was worse than expected. ADP employment change declined to 62 thousand, down from a revised 147 thousand and below the market estimate of 115 thousand.

This was followed by first-estimate GDP for Q1, which declined by 0.3% q/q, down sharply from 2.4% in Q4 and lower than the market estimate of 0.3%. This marked the first quarterly decline in the economy since Q1 2022. The weak GDP reading was driven by a surge in imports ahead of US tariffs taking effect and a drop in consumer spending.

EUR/USD has pushed below support at 1.1362 and is testing support at 1.1338. Below, there is support at 1.1306

There is resistance at 1.1394 and 1.1418

German inflation higher than expected, Euro dipsThe euro is calm on Wednesday. In the North American session, EUR/USD is trading at 1.1334, down 0.45% on the day.

Germany's inflation rate dropped to 2.1% y/y in April, down from 2.2% in March but above the market estimate of 2.0%. This was the lowest level in seven months, largely driven by lower energy prices. The more significant story was that core CPI, which excludes energy and food and is a more reliable indicator of inflation trends, rose to 2.9% from 2.6%. This will be of concern to policymakers at the European Central Bank, as will the increase in services inflation.

The ECB has to balance the new environment of US tariffs and counter-tariffs against the US, which will raise inflation, along with the strong rise in the euro and fiscal stimulus which will boost upward inflationary pressures. The ECB will be keeping a close look at Friday's eurozone inflation report, which is expected to follow the German numbers. Headline CPI is projected to drop to 2.1% from 2.2%, while the core rate is expected to rise to 2.5% from 2.4%.

The central bank would prefer to continue delivering gradual rate cuts in order to boost anemic growth, but this will be contingent on inflation remaining contained.

The markets were braced for soft US numbers but the data was worse than expected. ADP employment change declined to 62 thousand, down from a revised 147 thousand and below the market estimate of 115 thousand.

This was followed by first-estimate GDP for Q1, which declined by 0.3% q/q, down sharply from 2.4% in Q4 and lower than the market estimate of 0.3%. This marked the first quarterly decline in the economy since Q1 2022. The weak GDP reading was driven by a surge in imports ahead of US tariffs taking effect and a drop in consumer spending.

$EUGDPQQ -Eurozone GDP Growth Rate Beats Forecasts (Q1/2025)ECONOMICS:EUGDPQQ

Q1/2025

source: EUROSTAT

-The Eurozone economy grew by 0.4% in the first quarter of 2025,

accelerating from 0.2% in the previous quarter and exceeding market expectations of 0.2%.

$USGDPQQ -U.S Economy Unexpectedly Contracts in Q1/2025ECONOMICS:USGDPQQ

Q1/2025

source: U.S. Bureau of Economic Analysis

-U.S economy shrank 0.3% in Q1 2025, the first contraction since Q1 2022,

versus 2.4% growth in Q4 and expectations of 0.3% expansion, as rising trade tensions weighed on the economy.

Net exports cut nearly 5 percentage points from GDP as imports jumped over 40%. Consumer spending rose just 1.8%,

the weakest since mid-2023, while federal government outlays fell 5.1%, the most since Q1 2022.

Australian core CPI falls within the RBA target, Aussie shrugsThe Australian dollar has been showing strong movement this week but is calm on Wednesday. In the European session, AUD/USD is trading at 0.6391, up 0.14% on the day.

Australia released the CPI report for the first quarter. The Australian dollar didn't show much reaction, but the data could point to another rate cut from the Reserve Bank of Australia.

Headline CPI remained unchanged at 2.4% y/y, just above the market estimate of 2.3%. The significant news was that RBA Trimmed Mean CPI, the key core inflation indicator, dropped to 2.9% y/y from a revised 3.3% gain in Q4 2024. This is the first time in three years that core CPI is back within the RBA's target band of between 1-3%.

The drop in core inflation is good news for the government, with the national election on Saturday. Australian Treasurer Jim Chalmers jumped on the news, stating that the market expects four or five rate additional rate cuts this year, which would save households with mortgages "hundreds of dollars".

The Reserve Bank is expected to lower rates at its next meeting on May 20, which would mark only the second rate cut this year. After cutting rates in February, the central bank has stayed on the sidelines as US President Trump's tariffs have escalated trade tensions and sent the financial markets on a roller-coaster ride.

In the US, the markets are bracing for some weak data later today. ADP employment is expected to slip to 108 thousand, compared to 155 thousand in the previous release. ADP is not considered a reliable gauge for Friday's nonfarm payrolls, but a weak reading will only increase the anxiety of the nervous markets. US first-estimate GDP for Q1 is expected to slide to just 0.4% q/q, after a 2.4% gain in Q3. If there is a surprise reading from GDP, we could see a strong reaction from the US dollar after the release.

AUD/USD is testing resistance at 0.6403. Above, there is resistance at 0.6431

0.6357 and 0.6329 are the next support levels

DXY Printing a Bullish Triangle??The DXY on the 1 Hr Chart is forming a potential continuation pattern, the Bullish Triangle!

Currently Price is testing the 99.6 - 99.8 Resistance Area and battling with the 200 EMA and 34 EMA Band. The reaction to this conjunction could be pivotal in who overcomes: Buyers or Sellers.

Now during the formation of the potential pattern, Price on the RSI has stayed relatively Above the 50 mark being Bullish Territory suggesting Buyers could win the Bull-Bear battle.

Until Price breaks either the Resistance Area or the Rising Support, we will not have a definitive direction in which USD will strengthen or weaken.

*Wait For The Break*

-If Price breaks the Resistance Area, USD will strength possibly heading to the 100.8 - 101 Area

-If Price breaks the Rising Support, USD will weaken possibly heading to the 98.5 - 98.3 Area

Fundamentally, it is said China and USA are possibly getting closer to potentially ending the Reciprocal Tariff War going on with both sides willing to negotiate.

With the USA being the #1 Consumer of Goods globally, other economies can not afford us to not buy their things so I continue to see the Tariff War more as a Strong-Arm for the USA to be able to negotiate better terms!

USD News:

JOLTS - Tuesday, Apr. 29th

GDP - Wednesday, Apr. 30th

Unemployment Claims / ISM Manu. PMI - Thursday, May 1st

Non-Farm Employment Change / Avg Hourly Earnings / Unemployment Rate - Friday, May 2nd

For all things Currency,

Keep it Current,

With Novi_Fibonacci

British pound keeps rolling as UK GDP shinesThe British pound is up sharply on Friday, extending its rally for a fourth straight day. In the European session, GBP/USD is trading at 1.3088, up 0.94% on the day. The pound has surged 2.9% since Monday.

UK GDP higher than expected February with a gain of 0.5% m/m. This followed a revised 0% reading in January and beat the market estimate of 0.1%. This was the fastest pace of growth since March 2024. Services, manufacturing and construction all recorded gains. For the three months to January, GDP expanded 0.6%, above the revised 0.3% gain in January and higher than the market estimate of 0.4%.

The strong GDP data is welcome news amid all the uncertainty created by US President Trump's tariff policy. The UK's largest trading partner is the US and the 10% tariffs on UK products will hurt the UK export sector (Trump has suspended an additional 10% tariff for 90 days).

Bank of England expected to lower rates in May

The turmoil in the financial markets and escalating trade tensions has the Bank of England worried. The markets have priced in a rate cut in May, betting that the BoE will ease policy in order to support the weak economy, even with inflation above the 2% target. The BoE kept rates unchanged in March and meets next on May 8.

The US-China trade war rose up a notch on Friday, as China announced it would raise tariffs on US goods to 125% from 84%. This move was in response to the US lifting tariffs on China by 125% this week, for a total tariff rate at 145%. The trade war will dampen China's economy and Goldman Sachs has lowered its 2025 GDP forecast for China to 4.0% from 4.5%.

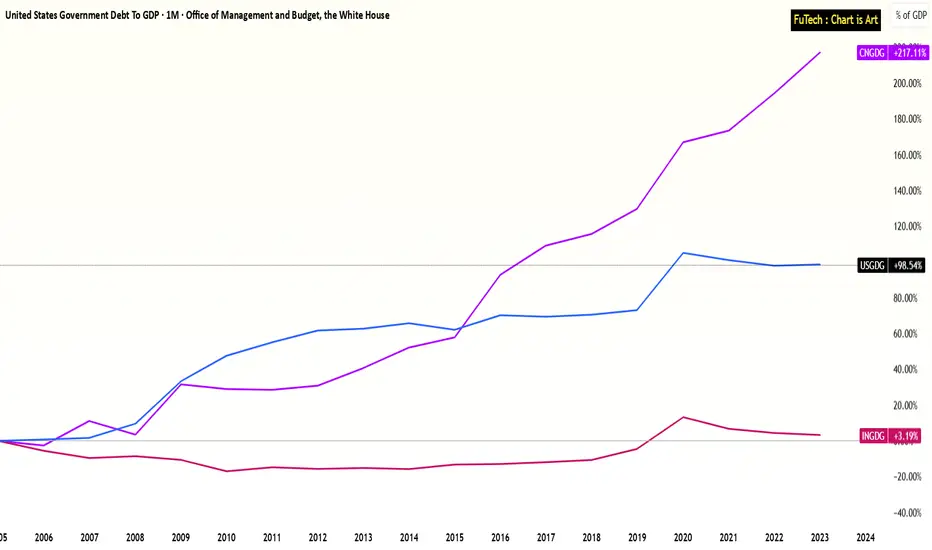

India, USA, China - Government Debt to GDP PerformanceIndia’s Fiscal Discipline Stands Out in a High-Debt Global Economy

Government Debt to GDP Performance Over the Last 20 Years:

China: +217%

USA: +99%

India: +3%

Over the last 2 decades, global economies have increasingly relied on debt to stimulate growth and manage crises.

However, a closer look at long-term Debt-to-GDP trends reveals a stark contrast in fiscal discipline among major economies:

-----------------------------------------------------------------------

India: A Beacon of Fiscal Stability

India has maintained remarkable fiscal discipline, with government debt increasing by just +3% relative to its GDP over the past 20 years.

This demonstrates India’s conservative borrowing strategy, especially notable given the country’s ambitious development goals, infrastructure push, and welfare programs.

This level of restraint positions India well in the face of rising global interest rates and inflation risks.

-----------------------------------------------------------------------

USA: Steady Climb Amid Stimulus Spending

The United States has seen a +99% increase in its debt-to-GDP ratio over the same period, driven by successive rounds of stimulus, defense spending, and entitlement obligations.

While the U.S. enjoys the unique advantage of issuing the world’s reserve currency, the long-term implications of rising debt—especially as interest payments rise—pose potential challenges to fiscal sustainability.

-----------------------------------------------------------------------

China: Debt-Fueled Expansion

China’s debt-to-GDP has surged +217% over the past two decades, reflecting its aggressive infrastructure-led growth model and significant off-balance-sheet local government borrowing.

While this has powered China's rapid urbanization and industrial growth, the mounting debt burden raises questions about long-term efficiency, default risks in the shadow banking sector, and the need for deleveraging.

-----------------------------------------------------------------------

🔍 Key Insights:

1) India’s 3% debt growth over 20 years highlights an underleveraged economy, offering headroom for targeted fiscal expansion if needed.

2) In a world where debt sustainability is becoming a key investment theme, India stands out as a relatively safer macro environment.

3) This fiscal prudence complements India’s improving trade metrics and strengthens its position in global economic leadership.

-----------------------------------------------------------------------

📈 Conclusion:

As the global economy grapples with inflation, rising interest rates, and debt concerns, India’s modest rise in government debt is a key macro strength.

While China and the USA have seen significant increases in their debt burdens, India’s fiscal balance provides confidence to both investors and policymakers for future growth cycles.

This makes India an attractive long-term investment destination in a world of rising uncertainty.

GBP/USD shrugs as UK GDP unexpectedly declineshe British pound has edged lower against the US dollar on Friday. GBP/USD is trading at 1.2928 in the European session, down 0.13% on the day.

The UK economy barely registered any growth in the second half of 2024, rising 0.1% in the third quarter and flatlining in the third quarter. The New Year hasn't seen any improvement, as GDP contracted 0.1% m/m in January, after a 0.4% gain in December and missing the market estimate of 0.1%. The surprise contraction was driven by declines in the production and manufacturing sectors. The economy expanded 0.2% in the three months to January, up from 0.1% in the three months to December but shy of the market estimate of 0.3%.

The weak GDP report won't make things any easier for Finance Minister Rachel Reeves, who will announce the Treasury's "Spring Statement" on March 26. Reeves is expected to outline plans for higher taxes and spending cuts. The tax hikes on British businesses are expected to weigh on investment, hiring and growth.

The Bank of England meets on March 20 and is widely expected to maintain rates at 4.5%. The BoE trimmed rates by a quarter-point in February. Inflation rose sharply in January to 3.0% y/y, up from 2.5% in December. The rise in inflation and weak GDP has raised concerns about stagflation, which is characterized by persistent inflation and weak growth.

Another headache for BoE policymakers is US President Donald Trump's tariff policy. The UK had hoped to avoid the tariffs, but this week the US slapped 25% tariffs on all steel and aluminum imports, including on UK products. That could hurt UK growth and boost inflation.

GBP/USD tested resistance at 1.2949 earlier. Above, there is resistance at 1.2978

1.2923 and 1.2894 are the next support levels

Can France’s Economy Defy Gravity?The CAC 40, France’s flagship stock index, showcases the nation’s economic strength, driven by global giants like LVMH and TotalEnergies. With their vast international presence, these multinational corporations provide the index with notable resilience, allowing it to endure domestic challenges. However, this apparent stability masks a deeper, more intricate reality. Beneath the surface, the French economy grapples with significant structural issues that could undermine its long-term success, making the CAC 40’s performance both a symbol of hope and a point of vulnerability.

France confronts multiple internal pressures that threaten its economic stability. An aging population, with a median age of 40—among the highest in developed nations—shrinks the workforce, increasing the burden of healthcare and pension costs. Public debt, projected to hit 112% of GDP by 2027, restricts fiscal flexibility, while political instability, such as a recent government collapse, hampers essential reforms. Compounding these issues is the challenge of immigration. France’s immigrant population, particularly from Africa and the Middle East, faces difficulties integrating into a rigid labor market shaped by strict regulations and strong unions. This struggle limits the nation’s ability to leverage immigrant labor to offset workforce shortages while straining social unity, adding further complexity to France’s economic challenges.

Looking forward, France’s economic future hangs in the balance. The CAC 40’s resilience offers a buffer, but lasting prosperity depends on tackling these entrenched problems—demographic decline, fiscal constraints, political gridlock, and the effective integration of immigrants. To maintain its global standing, France must pursue bold reforms and innovative solutions, a daunting task requiring determination and foresight. As the nation strives to reconcile its rich traditions with the demands of a modern economy, a critical question looms: can France overcome these obstacles to secure a thriving future? The outcome will resonate well beyond its borders, offering lessons for a watching world.

Japan's GDP revised downwards, yen swingsThe Japanese yen is showing movement in both directions today. In the North American session, USD/JPY is trading at 147.37, down 0.03% on the day.

Japan's GDP expanded 2.2% y/y in the fourth quarter of 2024, lower than the initial estimate of 2.8%. The revision was expected to stay largely unchanged but was pushed lower due to a decrease in inventories and consumption.

The GDP downward revision follows other soft data which points to weakness in Japan's economy. Household spending slumped 4.5% m/m in January. This was a sharp reversal from the 2.3% gain in December and missed the estimate of -1.9%. Annualized, household spending rose 0.8%, below the 2.7% in December and the market estimate of 3.6%. On Monday, the wage growth report indicated that real wages declined by 1.8% in January, after two months of growth.

How will the Bank of Japan react to the string of weak data? The annual wage negotiations are close to the end and the BoJ has urged companies and workers to reach a deal that significantly raises wages. This would boost growth and consumption and help keep inflation sustainable at the BoJ's 2% target.

The unions are asking for an average wage hike of 6%, up from 5.85% last year and the highest in more than 20 years. Last year's wage agreement led to the BoJ raising rates for the first time since 2007 and this year's wage deal could pave the way for another rate hike. The BoJ holds its next meeting on Mar. 19, five days after the wage settlement will be announced. The BoJ isn't expected to make a move next week but investors are circling April or May as potential rate-hike meetings.

There is resistance at 147.30 and 147.97

146.59 and 145.92 are the next support levels

$USGDPQQ -United States GDP (Q4/2024)ECONOMICS:USGDPQQ 2.3%

Q4/2024

source: U.S. Bureau of Economic Analysis

- The US economy expanded an annualized 2.3% in Q4 2024, the slowest growth in three quarters, down from 3.1% in Q3 and in line with the advance estimate.

Personal consumption remained the main driver of growth, increasing 4.2%, the most since Q1 2023, in line with the advance estimate.

Spending rose for both goods (6.1%) and services (3.3%).

Also, exports fell slightly less (-0.5% vs -0.8%) and imports declined slightly more than initially anticipated (-1.2% vs -0.8%), leaving the contribution from net trade positive at 0.12 pp.

Government expenditure also rose more (2.9% vs 2.5%).

Private inventories cut 0.81 pp from the growth, less than 0.93 pp.

On the other hand, fixed investment contracted more (-1.4% vs -0.6%), due to equipment (-9% vs -7.8%) and as investment in intellectual property products failed to rise (0% vs 2.6%).

Residential investment however, rose more than initially anticipated (5.4% vs 5.3%).

Considering full 2024, the economy advanced 2.8%.

Swiss franc dips as Swiss GDP declinesThe Swiss franc is down for a second straight trading day. In the European session, USD/CHF is trading at 0.8980, up 0.38% on the day.

The Swiss economy slowed to 0.2% q/q in the fourth quarter of 2024, down from 0.4% in Q3 and in line with expectations. This was the weakest expansion since Q2 2023. Construction weakened in the fourth quarter but manufacturing and exports rebounded from the previous quarter. Annualized, GDP rose 1.5%, down from 1.9% in Q3, the softest expansion in three quarters.

The weak GDP data supports the case for the Swiss National Bank to lower interest rates. The central bank is in the midst of an easing cycle and showed its aggressive side in December when it chopped rates by 50 basis points, bringing the cash rate to 0.50%.

The SNB only meets on a quarterly basis, magnifying the importance of each meeting. The next meeting is on March 20 and the markets have priced in a 25-bps cut at close to 100%. There are two key factors that Bank policymakers will be looking ahead of a rate decision - inflation levels and the exchange rate. Inflation has fallen by 0.1% for four consecutive months and is putting pressure on the SNB to continue lowering rates. The next inflation report is on March 5 and another soft report would cement a rate cut at next month's meeting. The SNB also uses monetary policy to ensure that the Swiss franc is not too strong, which would hurt the export sector.

The US releases second-estimate GDP for the fourth quarter of 2024 later today. The initial estimate came in at 2.3%, down from 3.2% in the third quarter. The US economy remains strong and inflation has been largely contained. The Federal Reserve is expected to cut rates this year only once or twice, unless the economic data does not evolve as expected.

USD/CHF is testing resistance at 0.8992. Above, there is resistance at 0.9018

0.8969 and 0.8943 are providing support

UK GDP beats forecast, gives sterling a liftThe British pound has edged higher on Thursday. GBP/USD is trading at 1.2460, up 0.15% on the day.

The UK economy ended 2024 on a high note, as GDP rose 0.4% m/m in December. This was the fastest pace of growth in nine months and blew past the market estimate of 01.%. The surprise gain was driven by increases in services and manufacturing activity. Annually, the economy expanded 1.5% in December, its best showing since Oct. 2022. This followed a revised 1.1% gain in November and beat the market estimate of 1%.

The surprise to the upside in GDP is welcome news but is tempered by the fact that much of the growth may have been due to government spending, as business investment decreased in the fourth quarter and consumer spending was flat. GDP quarterly growth was only 0.1%, an indication that the UK economy is still weak.

Fed Chair Jerome Powell testified before the House Financial Services Committee on Wednesday, just after the release of January's hot inflation report. Headline and core CPI were both higher than expected, with headline inflation accelerating for a fourth consecutive month. Powell told lawmakers that the Fed had made "great progress" on inflation, but acknowledged there was more work to do. Powell said that the Fed doesn't "get excited about one or two bad readings" but there are concerns that inflation could be moving in the wrong direction, away from the Fed's 2% target.

The Fed's battle with inflation has also become more complicated with President Donald Trump's promise to impose tariffs on US trading partners. Trump has called on the Fed to lower interest rates, raising fears that he is trying to dictate monetary policy to the Fed, which is suppose to act independent of political considerations.

GBP/USD tested resistance at 1.2493 earlier. Above, there is support at 1.2541

1.2435 and 1.2387 are the next support levels

GBP/USD dips on hot US inflation reportThe British pound is lower on Wednesday. GBP/USD is trading at 1.2400, down 0.37% on the day.

The January inflation report was hotter than expected, giving the US dollar a boost against the major currencies today. Headline CPI rose 3% y/y, above the December gain of 2.9% which was also the market estimate. Monthly, CPI rose 0.5%, up from 0.4% in December and above the market estimate of 0.3%. It was the highest monthly inflation rate since August 2023.

The core rate, which excludes food and energy, rose 3.3% from 3.2%, above the market estimate of 3.2%. Monthly core CPI accelerated to 0.4% from 0.2%, above the market estimate of 0.3%.

The inflation report didn't change expectations about the March meeting, with the Fed virtually certain to hold rates. However, expectations for a cut in May have dropped to just 9%, compared to 21% a day ago. The economy is performing well and the Fed will be reluctant to lower rates again until it sees inflation moving lower.

Fed Chair Powell repeated a familiar message in testimony before a Senate Banking committee on Tuesday, saying that the Fed "does not need to be in a hurry" to adjust policy. Powell said that rate policy remains restrictive but the Fed would be careful not to lower rates too quickly or too slowly. Powell deflected a question about Trump's tariffs and US trade policy but acknowledged that tariffs could lift inflation and complicate the Fed's ability to lower rates.

The UK releases GDP on Thursday, with little change expected from the sputtering UK economy. Annually, GDP is projected to remain unchanged at 1%, while the GDP 3-month average to December is expected to decline by 0.1%, compared to a flat reading in the previous release. The economy contracted in the third quarter and may show a small gain in Q4 thanks to increased government spending.

GBP/USD tested support at 1.2411 earlier. Below, there is support at 1.2368

1.2491 and 1.2534 are the next resistance lines

$CNGDPYY -China 2024 GDP Meets Official Target ECONOMICS:CNGDPYY

Q4/2024

- The Chinese economy expanded by 5.4% yoy in Q4 2024, topping estimates of 5.0% and accelerating from a 4.6% rise in Q3.

It was the strongest annual growth rate in 1-1/2 years, boosted by a series of stimulus measures introduced since September to boost recovery and regain confidence.

For full year, the GDP grew by 5.0%, aligning with Beijing's target of around 5% but falling short of a 5.2% rise in 2023.

GBP/USD slips after soft UK retail salesThe British pound is lower on Friday. In the European session, GBP/USD is currently trading at 1.2201, down 0.27% on the day. The pound can't find its footing and is down 2.5% in January and a massive 8.8% since October 1.

UK retail sales ended the week on a disappointing note. December retail sales declined 0.3% m/m, down from a downwardly revised 0.1% gain in November and shy of the forecast of 0.4%. Quarterly, retail sales fell 0.8% in the fourth quarter.

The weak retail data indicates that the UK consumer held tight on the purse strings during the crucial Christmas season. Consumers remain cautious over inflation worries and expectations that interest rates will stay high. Consumer spending is a key engine of economic growth, and the decrease is retail sales has raised fears of stagflation, a toxic mix of high inflation and low growth which will further hurt businesses and households. The UK economy posted negligible growth of just 0.1% in November, after back-to-back months of no growth.

Finance Minister Rachel Reeves could not have been pleased with the soft GDP and retail sales numbers. Reeves delivered a "tax and spend" budget in October 2024 and has admitted that she needs the economy to show stronger growth in order to increase tax revenue and carry out her spending plans. If the weak economy does not turn around soon, Reeves could find herself on the hot seat.

In the US, retail sales gained 0.4% m/m in December after an upwardly revised gain of 0.8% in November and below the forecast of 0.6%. Annually, retail sales rose 3.9%, below a downwardly revised 4.1% gain in November and above the forecast of 4.0%. The numbers show that consumer spending remains solid and the Federal Reserve isn't under pressure to lower interest rates anytime soon.

GBP/USD is testing support at 1.2225. Below, there is support at 1.2188

1.2274 and 1.2311 are the next resistance lines

UK GDP less than expected, pound edges lowerThe British pound has edged lower on Thursday. In the European session, GBP/USD is currently trading at 1.2205, down 0.22%.

The UK economy climbed out of negative growth for the first time in three months but not by much. After GDP contracted by 0.1% in September and October, November saw a small gain of 0.1%, missing the market estimate of 0.2%. In the three months to November, GDP showed no growth.

The small uptick in growth in November was welcome news for the government but the economic outlook is not very bright. The recent "tax and spend" budget will see tax increases take effect in April, including a rise in employer National Insurance contributions. This will hurt the business sector and many firms will cut back on spending and investment, which in turn will dampen economic growth. Inflation remains high and combined with low growth, stagflation is a real danger.

Another headache for the government is Donald Trump, who has promised to slap tariffs on US trading partners. The UK is heavily reliant on its export sector and a trade war with the US would be devastating for the fragile UK economy. As well, Trump's protectionist trade polices could lead to higher inflation which could derail much of the progress made to contain inflation. This week's soft UK inflation and GDP reports have raised expectations that the Bank of England will lower interest rates at the next meeting on Feb. 6.

In the US, December's inflation release presented a mixed picture, as headline CPI rose for a third straight month, while core CPI eased slightly. Expectations for a rate cut rose in the aftermath of the inflation report, sending the US dollar lower against many of the majors.

GBP/USD tested resistance at 1.2242 earlier. Above, there is resistance at 1.2310

1.2176 and 1.2108 are the next support levels

Euro stabilizes as Spain posts strong job dataThe euro has stabilized on Friday. In the European session, EUR/USD is currently trading at 1.0296, up 0.3% on the day. The euro fell as much as 1.2% a day earlier and fell below the 1.03 line for the first time since Nov. 2022.

The eurozone economy wasn't exactly on fire in 2024. The Ukraine-Russia war led to increases in gas and oil prices, millions of war refugees have strained the economy and many eurozone countries have boosted their defense budget as relations with Moscow have chilled. In addition, global demand has been weak and the incoming Trump administration could spell tariffs and even a trade war.

Germany, which for decades was the locomotive of Europe, hasn't recovered since the corona pandemic. Competition from China has hurt the key automotive industry and the government coalition has collapsed, resulting in political instability. France and Italy, the second and third largest economies in the eurozone, are also struggling.

The bright light is this gloomy picture has been Spain, the fourth-largest economy in the eurozone. "Sunny Spain" isn't just a catchy phrase for winter-weary tourists, but also reflects a resilient economy. According to the European Commission, Spain's economy is expected to have expanded by an impressive 3% in 2024. In contrast, Germany's GDP is projected to have contrasted by -0.1%.

Spain's manufacturing and services sectors are expanding, in contrast to the eurozone's three largest economies which are showing contraction. The labor market remains solid and the number of unemployed fell by 25.3 thousand in December, the lowest figure since December 2007.

The European Central Bank entered an easing phase in June and has lowered rates at the past three straight meetings. The central bank is keeping an eye on inflation but is expected to continue lowering rates in order to boost the weak economy. The ECB meets next on January 30.

EUR/USD is testing resistance at 1.0289. Above, there is resistance at 1.0353

There is support at 1.0203 and 1.0139

$USGDPQQ -U.S GDP (Q3/2024)ECONOMICS:USGDPQQ

(Q3/2024)

source: U.S. Bureau of Economic Analysis

- The US economy expanded an annualized 3.1% in Q3, higher than 2.8% in the 2nd estimate and above 3% in Q2.

The update primarily reflected upward revisions to exports and consumer spending that were partly offset by a downward revision to private inventory investment.

Imports, which are a subtraction in the calculation of GDP, were revised up.

Pound higher as Services PMI rises, job report nextThe British pound has moved higher on Monday, after declining 1% last week. In the European session, GBP/USD is trading at 1.2747, up 0.30% on the day.

The UK Services PMI rose to 51.4 in December, up from 50.8 in November, which was a 13-month low. This beat the market estimate of 51.0, but points to weak business activity as demand for UK exports has been weak and confidence among services providers remains subdued.

UK manufacturing is mired in a depression, and the PMI fell to 47.3 in December, down from 48.0 in November and shy of the market estimate of 48.2. This marked the lowest level in eleven months, as production and new orders showed an accelerated decrease.

The weak PMI data followed Friday's GDP report, which showed a 0.1% decline for a second straight month in October. This missed the market estimate of 0.1%. GDP rose just 0.1% in the three months to October.

The UK releases employment and wage growth numbers on Tuesday. The economy is projected to have lost 12 thousand jobs in the three months to October, after a sparking 200 thousand gain in the previous report. Wages including bonuses is expected to climb to 5% from 4.8%.

The Bank of England meets on Thursday and is expected to hold the cash rate at 4.75% after cutting rates by 25 basis points in November. The economy could use another rate cut but inflation remains a risk to upside, with CPI climbing in October to 2.3% from 1.7%. The BoE will be keeping a close eye on wage growth, which has been a driver of inflation.

The US releases PMIs later today. Manufacturing remained in contraction territory in November at an upwardly revised 49.7 and there is optimism that the new Trump administration's protectionist stance could benefit US manufacturers.

The services sector is in good shape and improved in November to 56.1, up from 55.0 in October. The uncertainty ahead of the US election is over and lower interest rates have contributed to stronger expansion in services.

GBP/USD is testing resistance at 1.2638. The next resistance line is 1.2668

1.2592 and 1.2562 are the next support levels

Euro rally ends, Eurozone GDP expected to accelerateThe euro is steady on Friday after jumping 0.7% a day earlier. In the European session, EUR/USD is trading at 1.0581, down 0.06% at the time of writing.

The eurozone wraps up the week with the GDP and job growth reports and the market is expecting an improvement. Third-quarter GDP is expected to improve to 0.4% q/q from o.2% in the second quarter. Job growth if forecast to tick upwards to 0.2% q/q, up from 0.1% in Q2.

In France, the political chaos continues. A no-confidence vote passed this week and has left the country without a functioning government. Prime Minister Michel Barnier resigned on Thursday after just three months in office. President Emmanuel Macron said he will name a new prime minister shortly but the political crisis could push up French interest rates and the country's large debt.

Germany, once the powerful locomotive of the eurozone, has faltered badly and has hampered growth in the eurozone. This week's German manufacturing data was dismal. The Manufacturing PMI remains mired in contraction and was unchanged at 43.0 in November. Factory orders for October declined by 1.5% after a 7.2% gain a month earlier. On Friday, industrial production fell 1% in October, after a 2% decline in September and shy of the market estimate of 1.2%.

The German Services PMI slipped into contraction in November and there is political instability, as the coalition German government collapsed in November. A snap election has been scheduled for Feb. 23, 2025.

The US wraps up the week with the nonfarm payroll report. With inflation largely contained, the employment growth is once again a key release can move the US dollar. The November report is expected to rise to a respectable 200 thousand, after a weak gain of 12 thousand in October, which was driven downwards by hurricanes and work stoppages at Boeing.

EUR/USD faces resistance at 1.0615 and 1.0644

1.0562 and 1.0533 are providing support