US 10Y TREASURY: The 4% expected to holdWith the U.S. government shutdown limiting official data, investors are turning to alternative economic indicators to gauge the economy. A University of Michigan survey on Friday showed consumer sentiment fell to 50.3 in November, well below the expected 53.0 and near historic lows. Concerns deepened after Challenger, Gray & Christmas reported October job cuts surged to 153,074, triple September’s figure and the highest for any October since 2003. In the environment of economic data blackout, it is very hard for investors to estimate the state of the US economy.

The 10Y US benchmark yields increased during the week to the level of 4,16% on Wednesday and Thursday, however, pulled back on Friday to the closing level of 4,09%. Softer private-sector job data boosted expectations of a Federal Reserve rate cut in December, which now assigns roughly a 67% probability. Considering a “blindfolded” situation with the U.S. macro data, it could be expected for 10Y Treasury yields to hold around the 4% level also in the week ahead.

Trade ideas

US10Y UNITED STATES 10YEAR TREASURY BOND YIELD. WEEKLY TF US10Y=4.09% weekly close and i see a pull back into confluence where i expect the US10Y to keep rising possibly into 5.0% 2026

FUNDAMENTALS OF US10Y AND US10.

The US 10-Year Treasury note (US10Y) is a debt security issued by the U.S. Department of the Treasury with a maturity of 10 years. It is a key benchmark in global finance and plays a vital role in the U.S. economy and monetary policy changes .

The US10Y yield represents the return investors demand for lending money to the U.S. government for 10 years.

It reflects expectations about economic growth, inflation, and Federal Reserve monetary policy.

When investors expect stronger growth and inflation, yields rise to compensate for higher risk and eroding purchasing power.

Conversely, in economic uncertainty or deflationary scenarios, yields fall as investors seek safe assets.

How US10Y Affects the U.S. Economy

It serves as a baseline for interest rates on mortgages, corporate bonds, and other loans, influencing borrowing costs for consumers and businesses.

Higher US10Y yields can increase borrowing costs, slowing economic growth but controlling inflation.

Lower yields encourage borrowing and investment, boosting economic activity.

It signals market sentiment about future inflation and growth prospects.

Federal Reserve Interest Rate Decisions and US10Y

The Fed’s policy rate influences short-term interest rates directly but also impacts long-term yields via expectations.

If the Fed signals tightening (rate hikes), long-term yields (like US10Y) tend to rise anticipating higher inflation and borrowing costs.

If the Fed signals easing or cuts rates, yields often decline as inflation and growth expectations moderate.

However, long-term yields can diverge if markets believe Fed policy will not control inflation or economic risks emerge.

Difference Between US10Y Yield and Bond Price

Yield is the effective interest rate earned by investors, inversely related to bond price.

When bond prices rise (due to demand), yields fall, and vice versa.

For example, if a 10-year bond’s fixed coupon is $20 annually, and its price drops from $1000 to $900, yield rises because new buyers pay less but still receive $20.

A bond coupon is the fixed annual interest payment that the bond issuer agrees to pay to the bondholder, usually expressed as a percentage of the bond's face (par) value. It represents the regular income investors receive from holding the bond, typically paid semi-annually or annually until the bond matures.

Key Points:

The coupon rate is the percentage of the bond’s face value paid annually as interest.

For example, a bond with a face value of $1,000 and a 6% coupon rate pays $60 per year, often split into two payments of $30 every six months.

The coupon rate is fixed at issuance and does not change, regardless of market price fluctuations of the bond.

This interest payment compensates investors for lending money to the issuer.

Origin of the Term:

Historically, bonds had physical coupons that investors would clip and redeem for interest payments, hence the name “coupon.”

Importance:

The coupon provides a predictable income stream for bondholders.

The coupon rate helps investors compare bonds, but the current yield (coupon payment divided by current bond price) changes as bond prices change in the market.

The inverse relationship between bond yield and bond price exists because a bond’s coupon payment is fixed, so price changes adjust the yield to reflect current market conditions.

Summary

Bond Coupon: Fixed interest payment from issuer to bondholder, based on face value.

Coupon Rate: Annual interest rate percentage fixed at issuance.

Investors rely on coupons for regular income until maturity.

The US10Y yield is a key economic indicator signaling growth and inflation expectations and influences borrowing costs across the U.S. economy.

The Fed’s interest rate decisions primarily affect short-term rates but also shape US10Y yields through policy signaling.

The bond price and yield move inversely; falling prices raise yields and vice versa, reflecting changing investor demand and market conditions.

This relationship underpins financial markets and monetary policy transmission globally.

#us10y #us10 #bond

Gold and Silver have a unique relationship with the US10Y.Gold and Silver have a unique relationship with the US10Y since 2011.

Gold+Silver have always had a cool-off period when the US10Y relative touches this range bottom.

Nov US10Y auctions = gold/silver cool-off period.

The bond market MIGHT disagree with rate cuts again.

US 10Y TREASURY: 4% remains in focusThe most important event during the previous week was the FOMC meeting, held on Wednesday, where the Fed decided to cut interest rates by another 25 basis points. Although the market was expecting that another rate cut is coming in December, still, comments from Fed Chair Powell, that such a course of action might not be in the store, set investors to re-positioning. The 10Y US benchmark yields strongly reacted to Powell's comment, bringing yields back toward the 4,1%. The lowest weekly yield levels were at $3,97% prior to the FOMC meeting.

Considering a strong shift in 10Y yields, it could be expected some relaxation in the week ahead. Still, a stronger move should not be expected. As per current charts, there is a higher probability that the 4% level could be tested for one more time. There is a lower probability for a further move toward the upside in the week ahead, but some volatility around the 4,1% might be expected.

Interest rate hikes over10Y bond yeilds broke below the 55W averages for a third time. Rates have now closed below the 55W avg a significant number of days.

I believe we will now see a 20year trend of decreasing int rates again approaching zero

US10YThe market still can't figure out what to make of COVID. Continuing to coin in this 3 year long consolidation phase.

US10Y This break-out can be the next Buy Signal.The U.S. Government Bonds 10YR Yield (US10Y) has been trading within a long-term Triangle pattern and more recently since May 22 2025 it has found itself declining inside a Channel Down.

This Bearish Leg (Channel Down) almost hit the bottom of the Triangle and has been rebounding in the past 10 days. As long as the 1W MA200 (orange trend-line) holds (right now almost at the bottom of the Triangle), the probabilities of a rebound and new Bullish Leg remain strong.

The confirmation for such Bullish Leg will come after the price closes a 1D candle above the 1D MA50 (blue trend-line). If it does, we an expect the price to rise to at least the 0.786 Fibonacci retracement level (Target 4.475%), which has happened all times (3) inside this Triangle after a Bearish Leg bottomed.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

US 10Y TREASURY: Will the Fed cut?Regardless of a relative volatility between levels of 4,02% and 3,94%, the 10Y US Treasury yields managed to sustain the 4% level during the previous week. The markets were mostly focused on US inflation data which were posted on Friday. The figures show that the inflation currently manages to sustain relatively lower levels, although still elevated from Fed's target of 2% y/y. The inflation in September was standing at 0,3% for the month and 3% y/y. Stable inflation and weakening jobs market have increased odds among investors that the Fed will cut interest rates by 25 bps at their meeting on October 29th.

The major event during the week ahead will be the FOMC meeting. Usually, market nervousness increases prior to the meeting, in which sense, such a behaviour could be expected also this time. There is some probability that yields could seek a bit higher levels in the week ahead, somewhere between 4,04% or 4,08%, but generally, the 4% should continue to hold.

US10Y Bonds Signal Bullish Reversal Toward 4.08%US10Y Bonds Signal Bullish Reversal Toward 4.08%

US10Y Government Bonds formed a bullish reversal pattern and is showing signs of bullish momentum. The price is up nearly +1.25% over the past 6 hours.

This can be considered a strong momentum considering the economic calendar is empty.

I expect the price to go up to 4.08% at the moment.

The first and strongest target will be found near 4.02%. Once the price moves above the pattern, it should continue to rise higher to the second targets of 4.05% and 4.08%.

You may find more details in the chart!

Thank you and Good Luck!

❤️PS: Please support with a like or comment if you find this analysis useful for your trading day❤️

The Refi Setup: 10-Year Yield Compression📉 10-Year Yield Compression = Refi Setup

The 10Y is coiling inside a descending wedge around 4.00%, signaling upside exhaustion.

A break below 3.90% → 3.66% is the key trigger — that’s the rate-relief zone.

Macro backdrop (credit stress, weak growth, liquidity preference) tilts odds downward.

Yield compression = rate repricing = higher refi probability.

🧭 Key Levels

4.18% → Resistance ceiling

3.90% → Battleground (break = downside momentum)

3.66% → Breakdown confirmation

Measured move projects ~35–40 bps lower toward 3.65% — enough to reprice mortgage spreads .

💡 Refi Mechanics

10Y ↓ → 30Y mortgage rates ↓

4.00% = ~5.8% avg mortgage

3.65% = ~5.35% avg mortgage

Even a 40–50 bps drop can spark a refi wave, as millions cross their break-even line.

Falling yields = faster prepayments → servicers buy Treasuries → more yield compression → positive feedback loop for lower rates.

Stock Market New Highs on CPI? Lotto call option? Tomorrow is the CPI report.

Inflation headline number is expected to be 3.1%.

We will likely see a positive reaction tomorrow which should send the S&P500 to new all time highs.

If we gap up into new all time highs be very careful as this usually gets sold into.

We took a lotto call option on NASDAQ:CRML with members.

This is a pure speculative dead cat bounce play.

US 10Y TREASURY: Treasury market holds the line? Unlike US equities, crypto or gold markets, the US Treasury yields were relatively keeping their grounds during the previous week. Still, some concerns regarding the potential impact of US-China tariffs were at least for now resolved when the US President commented on social networks that they are not sustainable. The US Government is still in official status of “shutdown” so relevant macro data are lacking. At the same time, a new potential banking crisis was emerging in the news, through so-called NDFI (Non-deposit Financial Institutions) companies, raising concerns over potential spill-over effect.

The level of 4,0% has been tested during the week, with some swings around this level. The week started at 4,07%, but the lowest level reached was at 3,93%. However, at Friday's trading session, yields were back to the level of 4,0%, where they are closing the week. There is a lot of uncertainty currently shaping the market sentiment. In this sense, some higher volatility might be possible also during the week ahead. Charts are showing that the path toward the 3,9% is currently open, but only if the level 4,0% does not sustain the buying pressure. Still, what is unclear is what could be the catalyst for the 3,9% level?

US 10Y TREASURY: tariff shock sends yields lowerTreasury yields dropped further as markets reacted to the sudden escalation in U.S.–China trade tensions, after U.S. President’s announcement of a 100 % tariff on Chinese imports. The move deepened fears of economic disruption and amplified uncertainty around trade policy. This came in addition to already increased uncertainty considering that the U.S. Government is already 10 days in the state of “shutdown”. The U.S. benchmark 10Y bond yields dropped from the level of 4,15% down to 4,03%. They are ending the week at 4,05%.

The week ahead will be driven by fundamentals. It is expected that new information will be released by the US Government regarding announced trade tariffs. This will most certainly impose a higher market volatility. As per current charts there are two options for 10Y yields: on one side, some relaxation could bring yields back to levels above the 4,10%, while on the other hand, the level of 4,0% is missing testing.

US10YUS10Y TECHNICAL DETAILS

4.193% A KEY RESISTANCE TO UPSWING

4.088% DEFENDED SUPPORT CURRENTLY

3.996 % LOW RECOVERED AND TESTED TWICE.ANY ATTEMPT ON THIS ZONE WILL BE A TECHNICAL DOWNSLIDE.

The US 10-year Treasury yield is approximately 4.125%

This yield represents the return investors expect for lending to the US government for 10 years and is a key benchmark influencing financial markets.

Dollar Index (DXY)

The DXY measures the value of the US dollar relative to a basket of major currencies , reflecting the dollar's strength amid global economic conditions such as interest rate differentials and geopolitical factors.

Relationship Between US10Y and DXY

The US10Y yield strongly influences the DXY because higher yields attract foreign capital, boosting demand for the dollar and strengthening the index.

When yields rise, the DXY usually follows upward due to investor demand for higher-yielding dollar assets.

Conversely, yields falling can weaken the dollar, reducing the DXY.

The relationship between bond yield and bond price is fundamental in bond investing and is characterized by an inverse correlation:

Key Concepts

Bond Price: The amount investors are willing to pay for a bond in the market. This can be above or below the bond’s face/par value.

Bond Yield: The return an investor expects to earn if the bond is held until maturity, expressed as a percentage. Several types include coupon rate, current yield, and yield to maturity (YTM).

Relationship Between Bond Yield and Bond Price

Inverse Relationship: When bond prices go up, bond yields go down; when bond prices fall, bond yields rise. This is because the fixed coupon payment represents a smaller or larger percentage of the bond’s market price depending on price changes.

Why? If interest rates in the market rise, new bonds offer higher yields. Existing bonds with lower coupons become less attractive, so their prices drop to increase their yield to competitiveness. Conversely, if market interest rates fall, existing bonds with higher coupons become more valuable, driving prices up and yields down.

Basic Formula Explanation

Current Yield = Annual Coupon Payment / Current Bond Price

Example:

A bond with a $1,000 face value and $50 annual coupon pays a 5% coupon rate.

If the bond price drops to $900, the current yield = $50 / $900 ≈ 5.56% (yield rises)

If the bond price rises to $1,100, the current yield = $50 / $1,100 ≈ 4.55% (yield falls)

More Accurate Measure: Yield to Maturity (YTM)

YTM accounts for the total return, including coupon payments and the gain or loss if the bond is held to maturity.

It reflects the discount rate that equates the present value of a bond’s cash flows (coupons + principal repayment) to its current market price.

Summary

Change Direction Effect on Bond Price and Yield

Interest Rates Rise Bond prices fall, bond yields rise

Interest Rates Fall Bond prices rise, bond yields fall

Bond Price Increases Bond yield decreases

Bond Price Decreases Bond yield increases

Bond investors must understand this inverse dynamic to manage portfolio risks and returns effectively.

NOTE ;IF YOU ARE A GOLD TRADER FOCUS ON DXY AND US10Y PRICE ACTION

#US10Y #BONDS #DXY #DOLLAR

US 10Y TREASURY: Shutdown fuels rate-cut speculationThe US Treasury bond market was focused on the US government “shutdown” during the previous week, estimating the implication which this shutdown could have on the macro segment on the US economy. The 10-year Treasury yield rose slightly to 4.154%, but reverted back as of the end of the week toward the 4,08%. Yields are closing the week at 4,119%.

The shutdown, which began on October 1, resulted from a failure by lawmakers to agree on a temporary spending bill. This impasse has led to the suspension of most government economic data releases, including the September jobs report, heightening uncertainty in the markets. Investors are particularly concerned about the potential impact on the Federal Reserve's upcoming policy decisions, as the lack of updated labor market data may influence the central bank's approach to interest rates.

Despite these challenges, markets are closely monitoring the situation, with expectations that the Federal Reserve may consider easing monetary policy if the shutdown persists and economic indicators weaken. The evolving political landscape and its effects on fiscal policy continue to be key factors influencing investor sentiment and Treasury yields.

US10Y & DXY downward trend continues. US10Y 4% triggers DXY 96.TVC:US10Y has been in a downward trend despite of US Fed holding the rates stable. In this blog space I have been following the downward sloping channel since Jan 2025. Since our May 2 prediction of a 4% in %US10Y we are very much on that glide path to lower low.

TVC:US10Y making new lows. 4% upcoming. 3.5% target low. for TVC:US10Y by RabishankarBiswal — TradingView

And then we add TVC:DXY into the mix which is also making lower lows and lower highs. I had a near term target of 96 on TVC:DXY and 90 by year end. This seems unreasonable now. I must change my outlook, when the charts change.

As we see, whenever TVC:DXY touches the lower bound of the downward slopping channel it tends to rebound to the mid-point of the channel. If it does so, then we might see a 100 on TVC:DXY Before we plunge down to 96 or lower.

Hence, I revise my prediction to be bullish on TVC:DXY , but that will have no impact on TVC:US10Y which is headed lower due to Fed cutting cycle and probably higher TVC:DXY dampening inflation.

Verdict: Revise our prediction: Short term bullish on OPOFINANCE:DXY. Long term bearish. Key levels: TVC:DXY to 100 first then 96. US10Y remains bearish with 4% by Dec 2025.

Bond Market Whiplash: September Ends with Yields Under PressureSeptember was a month of sharp swings for U.S. Treasuries. The 10-year yield started strong near 4.4% but lost momentum as political gridlock and growing bets on Fed rate cuts fuelled a flight to safety. Traders shifted from fearing inflation to bracing for slower growth and a possible government shutdown, sending yields drifting lower into month’s end.

What began as a hawkish month ended with markets pricing in caution — and the bond market once again reminding everyone that fear moves faster than policy.

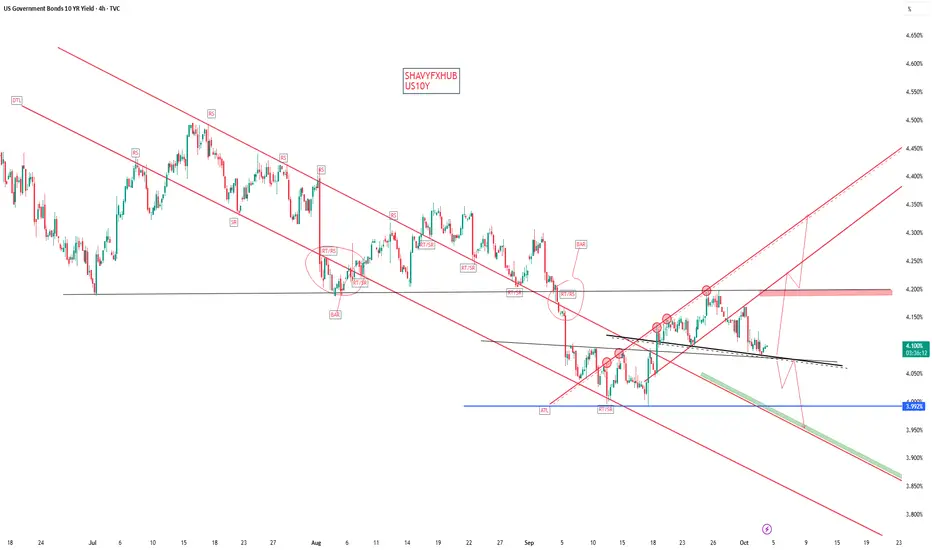

US10Y UNITED STATES 10 YEAR TREASURY YIELD.THE US10Y defended 3.992% demand floor and its expected that 4.196% be broken ,amides government shut down market could be in caution mode.

GIVING BITCOIN AND GOLD A BUY RUN.

#US10Y #DOLLAR

10 Yr Bonds When most see a government shutdown as panic,

I see it as strategy.

Cutting unnecessary spending = stronger funding base.

This can pull 10-yr bonds toward 3%, giving investors steady confidence.

Panic for some.

Opportunity for others.

Freight Power and Economic Growth1. The Concept of Freight Power

Freight power can be conceptualized through multiple dimensions:

Transport Infrastructure Capacity: The total capacity of road, rail, air, and port networks to move goods. High-capacity networks enable faster and larger volume movement.

Logistics Efficiency: Includes time taken to move goods, reliability of delivery, customs efficiency, and the technology used for inventory and transport management.

Modal Diversity: The ability to move goods via multiple transport modes (road, rail, waterways, air) improves resilience and reduces bottlenecks.

Regulatory and Policy Environment: Policies that ease transport, reduce tariffs, and promote trade corridors enhance freight power.

Integration with Global Supply Chains: Freight power grows exponentially when a nation’s logistics system is connected to international trade networks.

Essentially, freight power reflects both the quantity and quality of freight movement and its ability to sustain continuous economic activity.

2. Freight Power as a Driver of Economic Growth

Freight power and economic growth are interdependent. Several mechanisms explain this relationship:

2.1 Reducing Transaction Costs

Efficient freight systems lower the cost of moving goods. This reduction in transaction costs allows businesses to expand markets, improve profitability, and attract investment. Lower transportation costs also reduce the final price of goods, increasing consumer purchasing power.

2.2 Enabling Industrial Expansion

Industrial growth depends on the timely movement of raw materials to factories and finished products to markets. Countries with strong freight power can support large-scale industrial hubs and complex manufacturing supply chains. For instance, China’s industrial growth is closely linked to its investment in railways, ports, and highways.

2.3 Promoting Trade Competitiveness

Freight power enhances a country’s ability to participate in international trade. Efficient ports and shipping corridors allow exporters to access global markets rapidly, reducing lead times and enhancing competitiveness. Economies with poor logistics infrastructure often suffer from delayed shipments, higher costs, and reduced trade volumes.

2.4 Stimulating Employment and Regional Development

Freight and logistics systems create direct employment in transport, warehousing, and infrastructure sectors. They also stimulate regional development by connecting remote areas to urban markets. Industrial zones near ports, rail hubs, or highways tend to grow faster due to easier access to inputs and markets.

2.5 Supporting Agricultural Growth

For agrarian economies, freight power is critical for moving perishable goods efficiently. Refrigerated transport, efficient rural roads, and cold storage systems reduce post-harvest losses and enhance farmers’ incomes.

3. Freight Power and Macroeconomic Indicators

The impact of freight power on economic growth can be traced through several macroeconomic indicators:

3.1 Gross Domestic Product (GDP)

Transport and logistics are part of the services sector, contributing directly to GDP. More importantly, freight efficiency indirectly boosts GDP by facilitating industrial output and trade expansion.

3.2 Trade Balance

Improved freight systems lower export costs and enhance the competitiveness of domestic products abroad. Efficient freight corridors can transform landlocked economies by providing faster access to ports, improving their trade balance.

3.3 Inflation and Price Stability

Efficient freight reduces distribution costs, which can dampen inflationary pressures. Conversely, logistics bottlenecks increase the cost of goods, contributing to price volatility.

3.4 Foreign Direct Investment (FDI)

Investors prefer locations with robust logistics infrastructure. Countries with strong freight power attract FDI in manufacturing, warehousing, and trade sectors, stimulating employment and technology transfer.

4. Modes of Freight and Their Economic Impact

Freight power depends on the efficient integration of multiple modes of transport:

4.1 Road Freight

Road networks provide door-to-door connectivity, critical for domestic trade. Well-maintained highways reduce travel time, fuel consumption, and vehicle maintenance costs, supporting small and medium enterprises (SMEs) and regional markets.

4.2 Rail Freight

Railways are ideal for bulk cargo like coal, minerals, and grains. Rail freight is more cost-efficient over long distances and supports industrial clusters. Countries like India and China have leveraged rail freight to boost heavy industries.

4.3 Maritime Freight

Seaports are the backbone of international trade. Containerization and port efficiency directly influence export-import volumes. Countries with strategic ports can become trade hubs, boosting employment and foreign exchange earnings.

4.4 Air Freight

Air freight is crucial for high-value, perishable, or time-sensitive goods. Though costly, it facilitates global integration for sectors like electronics, pharmaceuticals, and fashion.

4.5 Intermodal Freight

The combination of road, rail, and sea freight enhances efficiency and flexibility. Logistics parks, container depots, and technology-driven freight management systems increase economic output.

5. Case Studies: Freight Power and Economic Growth

5.1 China

China’s Belt and Road Initiative and domestic investment in high-speed rail, highways, and ports have dramatically increased freight power. This infrastructure surge has enabled China to dominate global manufacturing and exports, leading to sustained GDP growth over decades.

5.2 India

India’s freight corridors, like the Dedicated Freight Corridor (DFC), aim to decongest road networks and enhance rail freight efficiency. Improved freight power can stimulate industrial clusters, reduce logistics costs (currently among the highest globally), and promote regional development.

5.3 European Union

The EU’s integrated transport networks, including cross-border highways, rail corridors, and ports, support intra-European trade. Freight power facilitates the free movement of goods, enhancing GDP and employment across member states.

6. Challenges in Freight Power Development

Despite its importance, many economies face challenges in enhancing freight power:

Infrastructure Bottlenecks: Aging ports, congested highways, and limited rail networks constrain growth.

High Logistics Costs: Developing countries often incur 10–20% of GDP in logistics costs compared to 5–10% in developed nations.

Regulatory Hurdles: Complex customs procedures, inefficient permits, and cross-border restrictions impede freight movement.

Technological Gaps: Lack of digital tracking, automated warehouses, and intelligent transport systems reduce efficiency.

Environmental Concerns: Freight transport contributes significantly to carbon emissions. Sustainable solutions are essential for long-term economic and environmental balance.

7. Policy Recommendations

To maximize the contribution of freight power to economic growth, governments and private actors should consider:

Infrastructure Investment: Expand highways, railways, ports, and logistics parks. Public-private partnerships can accelerate this.

Technology Integration: Implement smart logistics systems, GPS tracking, automated warehouses, and AI-based transport management.

Regulatory Reforms: Simplify customs procedures, reduce bottlenecks, and harmonize cross-border regulations.

Sustainability Focus: Promote green transport, electric vehicles, and carbon-efficient shipping practices.

Skill Development: Train personnel in modern logistics management to increase efficiency.

Regional Integration: Develop freight corridors that connect industrial zones, ports, and urban centers.

8. Future Trends

The future of freight power and economic growth is shaped by:

Digital Freight Platforms: AI-driven platforms will optimize routes, reduce fuel consumption, and increase reliability.

Autonomous Transport: Self-driving trucks, drones, and automated port operations will reduce human dependency and improve speed.

Green Logistics: Pressure to decarbonize will drive innovations in alternative fuels and eco-friendly supply chains.

Global Supply Chain Integration: Countries that integrate freight networks with global supply chains will attract more trade and investment.

Conclusion

Freight power is a cornerstone of economic growth. Efficient, diversified, and technologically advanced freight systems reduce costs, enhance trade competitiveness, stimulate industrial and agricultural output, and foster regional development. Countries that strategically invest in freight infrastructure, integrate logistics with global markets, and adopt sustainable practices can achieve faster, more inclusive, and resilient economic growth.

The link between freight power and economic growth is not linear—it is dynamic and multifaceted. While infrastructure alone is insufficient, its combination with policy support, technology, and global integration determines the true economic potential of freight power.

US Shutdown... How Can This Impact Yields?A U.S. shutdown doesn’t just freeze Washington — it shakes Wall Street. Investors rush into Treasuries for safety, pulling long-term yields down, while missing data and fiscal fears can push short-term yields up. The curve bends under politics, not just economics, turning every extra day of gridlock into fresh market uncertainty.

The 10-year U.S. Treasury yield recently fell ~4.3 basis points to about 4.145 % amid safe-haven demand ahead of a possible shutdown.

The curve has shown signs of steepening: longer maturities have been under more pressure (yields up) relative to short maturities.