Bitcoin(BTC/USD) Daily Chart Analysis For Week of Oct 31, 2025Technical Analysis and Outlook:

The trading session from last week was notably eventful. The Bitcoin market experienced significant volatility, fluctuating between the Mean Resistance level of 116,000 and the critical Mean Support level of 106,500. Currently, the price is actively navigating this range.

Current market analysis indicates a likelihood of a retest toward the Mean Support level at 106,500, with a primary focus on the potential for further downward movement towards the Mean Support level of 101,000. This trajectory may ultimately lead to our key objective of reaching the Outer Coin Dip at 97,000. It is, however, essential to acknowledge the robust rebound potential at these pivotal levels.

Economy

$EUGDPQQ -Europe GDP (Q3/2025)ECONOMICS:EUGDPQQ

Q3/2025 +0.2%

source: EUROSTAT

- The Eurozone economy expanded by 0.2% quarter-on-quarter in Q3 2025,

up from 0.1% in Q2 and slightly above market expectations of 0.1%, according to a flash estimate.

France grew 0.5%, exceeding expectations of 0.2%, driven by a sharp rise in exports, while Spain remained the best performer among the bloc’s largest economies, expanding 0.6% as expected, supported by strong household consumption and fixed investment.

Meanwhile, Germany stagnated due to a decline in exports, and Italy stalled, with the industrial sector contracting and services showing no growth.

On an annual basis, Eurozone GDP rose 1.3%, above expectations of 1.2%.

The better-than-expected figures ease pressure on the ECB to cut interest rates in the near term, supporting the view that the economy remains resilient despite geopolitical tensions and trade policy uncertainty.

$EUINTR -ECB Holds Rate at 2.15% (October/2025)ECONOMICS:EUINTR 2.15%

October/2025

source: European Central Bank

- The ECB kept interest rates unchanged for the 3rd meeting,

reflecting confidence in the eurozone’s economic resilience and continued easing of inflationary pressures.

In her remarks after the meeting, ECB President Lagarde emphasized that the ECB is “in a good place” and remains committed to taking all necessary actions to preserve that stability.

Crypto will boom, BUT...In my view, the cryptocurrency market is poised for a significant multi-year rally.

However, such a rally cannot begin without a major transfer of capital, from weaker holders to large institutional players. This is why I believe we are likely to experience a sharp correction in the coming days or weeks, possibly extending toward the end of the year.

My outlook for this short-term downturn is driven by two key factors:

Persistent uncertainty surrounding the Federal Reserve’s next policy move, particularly whether it will proceed with an interest rate cut in December, and a bearish pattern emerging in the global money supply. After a notable recent decline, this formation suggests further contraction ahead.

The good news is that this potential market shakeout may serve as the final reset before Bitcoin establishes its bottom. Those who withstand the upcoming volatility will likely find themselves well-positioned for the next major bull run.

#bitcoin #crypto #finance #economy #market #analysis

$JPINTR -Japan Interest Rates (October/2025)ECONOMICS:JPINTR

October/2025

source: Bank of Japan

- The Bank of Japan kept its benchmark short-term rate unchanged at 0.5% in October 2025, maintaining borrowing costs at their highest level since 2008 and extending a pause since the last hike in January.

The decision, in line with market expectations, was approved by a 7-2 vote, with board members Naoki Tamura and Hajime Takata again proposing a rise to 0.75%, as they had in September.

The central bank reaffirmed its commitment to continue raising borrowing costs if the economy follows its projections.

The move came hours after the U.S. Federal Reserve delivered its second rate cut of the year.

In its quarterly outlook, the BoJ held core inflation for FY 2025 at 2.7%, expecting it to ease to 1.8% in FY 2026 before rising slightly to 2.0% in FY 2027.

GDP growth for FY 2025 was revised up to 0.7% from 0.6%, supported by a trade deal with Washington and new leadership under Prime Minister Sanae Takaichi, while GDP projections for FY 2026 and 2027 remained at 0.7% and 1%, respectively.

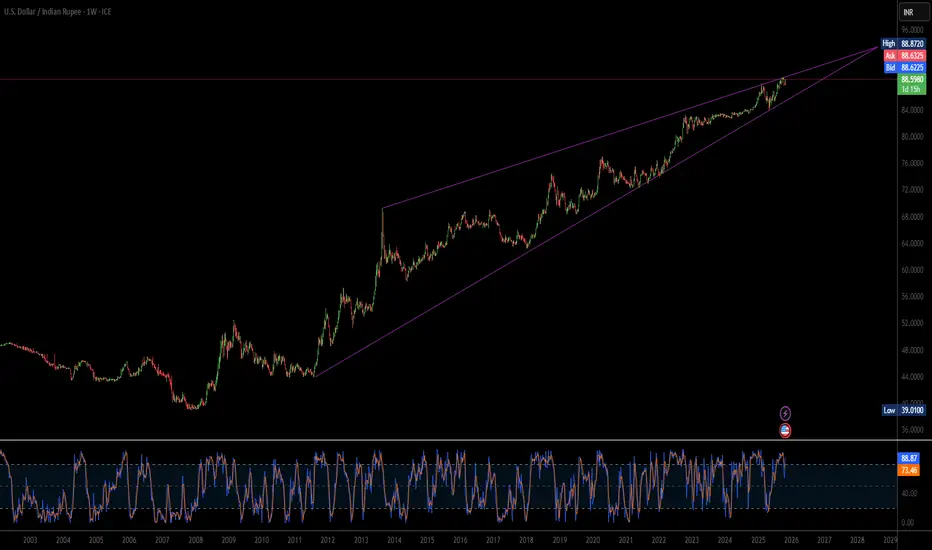

Why Is The Rupee Falling When The Dollar Is Weak?The Indian Rupee (INR) is exhibiting a pronounced, sustained weakness against the US Dollar (USD), pushing the USD/INR pair toward the 88.60 level, even as the global US Dollar Index (DXY) shows signs of softness. This resilience in the USD/INR confirms that domestic and structural headwinds—rather than external dollar strength—are primarily responsible for the Rupee's depreciation. A deep analysis across strategic, economic, and technological domains reveals that geopolitical delays and cautious monetary policy abroad are significantly outweighing any temporary relief from global dollar flows.

The central source of this structural weakness stems from two major factors: geopolitical uncertainty and macroeconomic policy divergence. The persistent delay in finalizing a comprehensive trade agreement between the US and India fuels Foreign Institutional Investor (FII) anxiety, leading to hesitant capital inflows. While FIIs showed a brief surge in buying, overall conviction remains low without a clear trade resolution. Concurrently, the US Federal Reserve's commitment to a "higher-for-longer" interest rate floor, despite a recent cut, strengthens the relative appeal of the USD. This policy stance attracts global capital to US assets, thereby limiting liquidity and increasing the cost of holding the INR.

Furthermore, India’s technological landscape adds to the structural demand for the USD. Low domestic Research & Development (R&D) investment and a heavy reliance on foreign patents mean the nation must spend more USD to import essential high-tech equipment and intellectual property. This technological deficit creates a persistent, structural requirement for foreign currency, putting continuous pressure on the Rupee. From a technical analysis perspective, the USD/INR pair's decisive hold above the 20-day Exponential Moving Average (EMA) confirms the market's bullish bias, suggesting the current trend is robust and targeting the all-time high of 89.12.

In essence, the Rupee's struggle is a complex interplay of internal and external structural factors. Until a major trade deal is confirmed, capital inflows become more decisive, or India's technological import needs stabilize, the market will continue to favor the USD. Traders must recognize that the technical path of least resistance for the USD/INR is upward, driven by these fundamental geopolitical and economic asymmetries rather than temporary movements in the global dollar index.

$USINTR -Fed Delivers Rate Cut (October/2025)ECONOMICS:USINTR

October/2025

source: Federal Reserve

- The Federal Reserve lowered the federal funds rate by 25 bps to a target range of 3.75%–4.00% at its October 2025 meeting, in line with market expectations.

The move followed a similar cut in September,

bringing borrowing costs to their lowest level since 2022.

Policymakers cited increasing downside risks to employment in recent months while inflation has moved up since earlier in the year and remains somewhat elevated.

The Fed said it will continue to monitor the implications of incoming information for the economic outlook and would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of its goals.

In addition, the central bank decided to conclude the reduction of its aggregate securities holdings on December 1.

US vs China: should we be worried?Another ''Buy the rumor''? What EVERY trader should have in mind amid US-China Trade talks:

1. Beijing balks at enforcement or verification terms

China could reject U.S.‑demanded mechanisms for monitoring compliance, such as agricultural purchase tracking or fentanyl control checkpoints.

Past talks collapsed over the same issue, the U.S. insisting on verification, China citing sovereignty .

If Beijing signals “framework only, no enforcement,” Washington may treat it as stalling and re‑activate the 155 % tariff threat for Nov 1 .

2. Rare‑earth or tech export retaliation

China still holds leverage through critical‑mineral exports. If it re‑tightens rare‑earth or semiconductor‑material shipments, Washington could impose new export controls on Chinese tech, reigniting escalation.

That “supply‑chain weaponization” was what caused the early‑October market sell‑off and would likely repeat—hurting metals, EV, and chip stocks first.

3. Unexpected Trump pivot under political pressure

Analysts warn that Trump tends to shift abruptly when domestic optics change.

A new social‑media statement accusing Beijing of backsliding could nullify the deal narrative overnight .

Morgan Stanley’s Mike Wilson noted that any such reversal could trigger a 10–15 % equity correction due to “positioning unwind and tariff risk repricing” .

4. National‑security or Taiwan language slips

The framework explicitly avoids defense issues, but if Trump or Xi reference Taiwan or South China Sea policy during press remarks, it could politicize the summit and freeze trade clauses .

5. Market complacency and over‑positioning

Even with a signed “mini‑deal,” markets may have already priced it in.

JPMorgan research warns that a “buy‑the‑rumor, sell‑the‑news” reaction is likely if investors had pre‑emptively rotated into cyclicals .

Thin liquidity plus leveraged optimism could amplify any disappointment.

Bottom line:

Unless both leaders explicitly confirm a tariff suspension and avoid new geopolitical flashpoints, markets remain only one headline away from reversal. The biggest red flags to watch this week are (1) a stalled verification clause, (2) talk of renewed tech or rare‑earth restrictions, or (3) Trump implying that tariffs will still “go forward pending review.” Any of these could instantly shift sentiment from optimism to a fresh wave of selling.

#trade #correction #economy #finance #us #china #tariff #bitcoin #crypto #stocks #equities #trading

S&P 500 Daily Chart Analysis For Week of Oct 24, 2025Technical Analysis and Outlook:

The most recent trading session exhibited significant volatility in the S&P 500 Index, marked by pronounced price fluctuations between the Mean Resistance at 6671 and the Key Resistance at 6753. This range served as a crucial threshold for market participants, prompting a series of rapid buying and selling that influenced the index's overall wild movement. Ultimately, this price action culminated in a breakout above the completed Outer Index Rally at 6768.

At present, the index is situated at the newly established Key Resistance level of 6800, which lies just below the historical high of 6807. This positioning indicates the potential for further upward momentum, as the prevailing trend suggests a well-structured Active Inner Rebound extension toward the Next Outer Index Rally target of 7110.

Conversely, it is imperative to acknowledge the possibility of a sustained, steady-to-lower pullback from the Key Resistance level of 6800 to Mean Support 6740 for the Secondary Primary Up-Trend to continue on its path.

Bitcoin(BTC/USD) Daily Chart Analysis For Week of Oct 24, 2025Technical Analysis and Outlook:

In last week's trading session, the Bitcoin market experienced wild gyrations between Mean Support 106500 and the critical Mean Resistance level of 113500, as the price is currently actively fluctuating between the two.

Current market analysis indicates an initial recovery towards the Mean Resistance level of 113500, with the potential for further upward movement to the Mean Resistance level of 116000. However, it is crucial to acknowledge the possibility of a reversal at these resistance levels, which could extend to continue the Progressive In Force Retracement trend.

$USIRYY -U.S Inflation Rate (September/2025)ECONOMICS:USIRYY 3%

September/2025

source: U.S. Bureau of Labor Statistics

- The US annual inflation rate rose to 3.0% in September from 2.9% in August, slightly below market expectations of 3.1%.

It was the highest rate since January, mainly due to a jump in energy prices. Meanwhile, core inflation eased to 3.0% from 3.1%, while monthly headline and core CPI increased 0.3% and 0.2%, respectively.

$JPIRYY -Japan CPI (September/2025)ECONOMICS:JPIRYY

September/2025

source: Ministry of Internal Affairs & Communications

- Japan’s annual inflation rate rose to 2.9% in September 2025 from August’s 10-month low of 2.7%.

The increase was driven by the first rise in electricity prices in three months (3.2% vs -7.2%) and a rebound in gas costs (1.6% vs -2.7%), after the expiry of temporary government measures launched to offset summer heat.

Price growth also persisted across most categories, including housing (1.0% vs 1.1%), clothing (2.5% vs 2.9%), transport (3.0% vs 3.0%), household items (1.0% vs 2.0%), healthcare (1.2% vs 1.3%), recreation (2.0% vs 2.3%), communications (6.7% vs 7.0%), and miscellaneous goods (0.7% vs 1.3%), while education costs fell further (-5.6% vs -5.6%).

On the food side, prices increased 6.7% yoy, easing from a 7.2% rise in August and marking the softest gain in four months, largely due to the smallest rise in rice prices in a year (49.2%) amid Tokyo’s continued efforts to contain staple food costs.

Core inflation came in at 2.9%, matching consensus and rising from the prior 2.7%.

$CNGDPYY - China GDP (Q3/2025)ECONOMICS:CNGDPYY

Q3/2025

source: National Bureau of Statistics of China

- China’s economy expanded 4.8% year-on-year in Q3 2025, down from 5.2% in Q2,

marking its slowest pace since Q3 2024.

While in line with market expectations,

the GDP growth has lost momentum after a strong start to the year, pressured by U.S. trade tensions, a prolonged property slump, and soft consumer demand.

September data showed retail sales in China rose at their slowest pace in a year despite ongoing consumer subsidy programs, while the jobless rate edged down but remained near August’s six-month high.

Industrial output, however, grew at its fastest pace in three months ahead of Golden Week.

On the trade front, exports and imports beat forecasts as firms pushed into new markets and domestic demand was boosted by holiday spending.

China’s statistics bureau cautioned that risks and external headwinds persist, with the recovery’s foundation still fragile.

Still, it said that 5.2% growth in the first nine months lays a “solid foundation” for meeting a full-year target of around 5%.

S&P 500 Daily Chart Analysis For Week of Oct 17, 2025Technical Analysis and Outlook:

Last week's trading session was marked by significant volatility in the S&P 500 Index, which experienced pronounced price fluctuations following its descent to our established Mean Support level of 6550. This level served as a critical point for market participants, triggering a series of rapid buying and selling activities that contributed to the index's overall gyrations.

At present, the index is positioned just below the newly established Mean Resistance level of 6671, which indicates the potential for further upward momentum, as this trend suggests a Well-built extension to the subsequent Mean Support level of 6550.

Contrariwise, it is essential to acknowledge and be aware of the emergence of the unexpected market drop to the Mean Support 6550, 6485, 6371, and the Key Support level of 6240. Additionally, it's crucial to take note of the Auxiliary Inner Rebounds occurring at these critical points.

EUR/USD Daily Chart Analysis For Week of Oct 17, 2025Technical Analysis and Outlook:

Last week, we had an interesting trading session! The Euro demonstrated a considerable increase after reaching our crucial Mean Support level at 1.155. Nevertheless, this significant upward reversal fell marginally short of the Mean Resistance at 1.174, leading to a subsequent decline in the currency.

Current market indicators suggest that this Active Inner Rebound movement is unlikely to be sustainable. Ongoing market sentiment consistently reflects a retracement toward the Outer Currency Dip, designated at 1.145. Should this downward trend persist, it may extend further to the Key Support level of 1.140.

Conversely, it is essential to acknowledge and be aware of the emergence of an Auxiliary Inner Rebound following the Outer Currency Dip at 1.145, in conjunction with the Key Support level of 1.140.

Bitcoin(BTC/USD) Daily Chart Analysis For Week of Oct 17, 2025Technical Analysis and Outlook:

In the most recent trading session, the Bitcoin market experienced a significant decline, falling below critical support levels of 108000 and 105700, as the price is currently actively fluctuating between these two points.

The current market analysis indicates an initial potential rebound towards the Mean Resistance level of 109500, with further extension possibilities up to the Mean Resistance level of 115500. It is essential to recognize and be aware that an Auxiliary Inner Rebound occurrence following the Outer Coin Dip, marked as a 97000, in conjunction with the Mean Support level of 99000. This scenario is particularly significant at the Progressive In-Force retracement extension, identified as the Key Support level of 94000.

$CNIRYY -China CPI (September/2025)ECONOMICS:CNIRYY

September/2025

source: National Bureau of Statistics of China

- China’s consumer prices dropped 0.3% yoy in September 2025,

steeper than market estimates of a 0.1% decline but slightly less than

a 0.4% fall in the previous month.

Food prices declined further (-4.4% vs -4.3% in August), recording the strongest contraction since January 2024, amid broad-based falls across categories, with pork prices down further due to abundant supply ahead of the Golden Week holidays,

lower production costs, and weak demand.

In contrast, non-food inflation quickened (0.7% vs 0.5%), supported by ongoing consumer trade-in schemes to bolster consumer demand, with more increases in housing (0.1% vs 0.1%), clothing (1.7% vs 1.8%), healthcare (1.1% vs 0.9%), and education (0.8% vs 1.0%).

Meanwhile, transport costs fell at a slower pace (-2.0% vs -2.4%).

Core inflation, which excludes food and energy, rose 1.0% yoy, the highest in 19 months, after August's 0.9% gain.

On a monthly basis, the CPI inched up 0.1%, missing forecasts of 0.2% after remaining flat in August.

Global Markets Turn Defensive as Trump’s Tariff Threats Shake CoGlobal Markets Turn Defensive as Trump’s Tariff Threats Shake Confidence.

U.S. President Donald Trump has announced he is considering a “massive increase” in tariffs on imports from China, signalling a possible escalation in the long-running trade dispute between the world’s two largest economies.

In response, Beijing has vowed to impose countermeasures should Washington proceed with the proposed 100% tariffs, defending its recent export rules while warning that such moves would further raise tensions.

A high-level meeting between President Trump and Chinese leader Xi Jinping — expected on the sidelines of the APEC leaders’ meeting in South Korea later this month — now appears uncertain, with Washington’s recent rhetoric jeopardising the diplomatic groundwork for the summit.

Markets are already reacting. Investors have been shifting capital toward safe-haven assets, with gold and silver among the biggest beneficiaries of the risk-off move. Gold notably pushed past the $4,000-per-ounce mark amid the turmoil, underscoring strong demand for protection against trade-driven volatility.

According to World-Signals analysis, with gold prices holding above $4,000 per ounce, any correction toward $3,950–$3,975 is likely to trigger fresh buying interest.

As geopolitical strategy increasingly intersects with resource control — from oil to rare earth elements — the global economic balance may be entering a new phase of heightened volatility. Traders and portfolio managers should watch tariff announcements, export-control actions on critical inputs (including rare earths), and developments around planned diplomatic meetings for signs of market direction.

S&P 500 Daily Chart Analysis For Week of Oct 10, 2025Technical Analysis and Outlook:

During the previous week's trading session, the S&P 500 Index experienced a notable decline in price activity after reaching the Key Resistance level of 6750 and the Outer Index Rally at 6946.

At present, the index is positioned just above the newly established Mean Support level of 6550, which indicates the potential for further downward momentum. This trend could extend to subsequent Mean Support levels of 6485, 6371, and the Key Support level at 6240.

It is imperative to recognize that the index may exhibit a strong rebound following its price contact at the Mean Support level of 6550. Furthermore, there exists the possibility of an upward extension that could reach the Key Resistance target of 6753.

EUR/USD Daily Chart Analysis For Week of Oct 10, 2025Technical Analysis and Outlook:

During the trading session of the previous week, the Euro exhibited considerable volatility, initially declining to approximately the Mean Support level of 1.153 before experiencing a substantial upward reversal. Current market indicators suggest that this bullish trend may persist, with particular emphasis on the Mean Resistance level identified at 1.165, which could lead to an ascent toward the secondary Mean Resistance at 1.174.

Conversely, recent price movements may indicate a reversal, leading to a decline toward the Mean Support level of 1.156, which could complete the Outer Currency Dip at 1.145. Should this downward trajectory continue, it may extend further to the Key Support level of 1.140.

Bitcoin(BTC/USD) Daily Chart Analysis For Week of Oct 10, 2025Technical Analysis and Outlook:

During the most recent trading session, the Bitcoin market experienced a notable decline, falling below significant support levels of 120000, 117500, and 114000, respectively. Current market analysis indicates an initial potential retracement toward the Mean Support level of 108000, with further extension possibilities to the Mean Support level of 105700 and the Key Support level of 100000. It is crucial to acknowledge that intermediary rebounds may occur at these defined levels, particularly at the Mean Resistance level of 113000.

Friday - the day the market shows its true faceEveryone loves chasing moves early in the week - Monday, Tuesday, news, data drops. But if you look closer, the most honest market signals usually appear on Fridays. By that time, the fight between buyers and sellers is settled, and the price reveals who really has control.

When big funds and banks are confident about direction, they don’t rush to close positions before the weekend. The market often ends the week at its highs - and Monday continues the same move. But if selling pressure picks up late on Friday, it’s usually a warning sign: traders are nervous and prefer not to hold risk over the weekend.

Friday’s close isn’t just another candle - it’s the verdict for the entire week. A close near the top of the range means demand is strong; near the bottom means fear and profit-taking are taking over.

Retail traders often close everything before the weekend to “stay safe.” But smart money uses those thin Friday hours to shake out weak hands and grab liquidity. That’s why the real moves often begin right after those late-week impulses.

What to keep an eye on:

1. Watch where the price closes within the weekly range - it sets the tone for Monday.

2. Check volume during the last trading hours - it tells you who’s really in control.

3. A strong Friday move with no news? Often that’s the setup for next week’s trend.

Friday’s action is rarely random. It’s the final scene before the next act of the market drama.

$USGRES - U.S Gold Reserves (October/2025)ECONOMICS:USGRES

October/2025

source: World Gold Council

-The U.S Treasury's Gold Reserves ECONOMICS:USGRES have surpassed 1$ Trillion Dollars in

Value for the first time in History;

more than 90 times what's stated on the Government's Balance Sheet.

United States now holds 2.4 Times more Gold than Germany,

the second largest Gold holder in the World.

Not even the 2020 Pandemic Crisis, 2008 Financial Crisis or Dot.Com Bubble saw

TVC:GOLD post a 40% Annual Gain.

As The U.S Dollar TVC:DXY continues to lose Purchasing Power,

Safe Heaven assets like TVC:GOLD , TVC:SILVER and CRYPTOCAP:BTC continue their

Uptrend Resumption .