TSLA Catalysts Ranking: Q1 2026 Outlook PT 600 USD________________________________________

TSLA: Updated Outlook (Nov-2025)

Here's an updated/revised outlook for TSLA including all the primary

catalyst ranking and analyst ratings and overview of latest developments

this was updated for Q1 2026 with all the viable market data.

________________________________________

🤖 1) Autonomous & Robotaxi Execution — 9.2/10 (↑)

• What changed: Tesla’s invite-only Austin robotaxi pilot kept running through the summer; Tesla also says it launched a Bay Area ride-hailing service using Robotaxi tech (Q3 deck). FSD v14 (Supervised) began rolling out in Oct with broader model upgrades; Tesla claims billions of supervised miles and AI training capacity lifted to ~81k H100-equivalents.

• Offsetting risk: NHTSA opened a fresh probe (Oct-2025) into ~2.9M Teslas over traffic-safety violations when using FSD; investigation cites 58 reports incl. crashes/injuries.

• Why the bump: Real pilots in two metros + visible AI scale-up keep autonomy the center of the bull case—even with elevated regulatory risk.

________________________________________

🌍 2) EV Demand & Geographic Mix — 8.6/10 (↘ )

• What changed: Q3-25 delivered record vehicles and record energy storage deployments, with record revenue and near-record free cash flow. Still, we’re past the U.S. tax-credit pull-forward and China/Europe pricing remains competitive.

• Read-through: Momentum into Q4 looks better than 1H-25, but regional price discipline and mix will matter.

________________________________________

💸 3) U.S. EV Tax Credits & Incentives — 6.0/10 (↘)

• What changed: Federal new/used EV credits ended for vehicles acquired after Sept 30, 2025 under OBBB. Buyers can still qualify if a binding contract + payment was made by 9/30 and the car is placed in service later (“time-of-sale” reporting). This creates a limited after-deadline tail into late ’25/early ’26 but the program has sunset for new acquisitions.

• Implication: Pull-forward demand helped Q3; near-term becomes tougher without the credit.

________________________________________

📉 4) Rates & Credit Conditions — 6.5/10 (↔)

• Rate-cut expectations have eased financing costs M/M, but absolute affordability still binds EV uptake. (Macro-sensitive; no single decisive print.)

________________________________________

🎯 5) Affordable Model / Next-Gen Platform — 8.0/10 (↔)

• Q3 deck emphasized Model 3/Y “Standard” variants to expand entry price points; true next-gen remains staged, with execution risk.

________________________________________

🔋 6) Battery Cost & Margin Levers — 8.3/10 (↑)

• What changed: Q3 total GAAP GM improved vs 1H; energy revenue +44% YoY; free cash flow ~$4.0B. Scale/learning and supply-chain localization called out.

________________________________________

⚡ 7) Energy, AI & Optimus Optionality — 8.7/10 (↑)

• Record storage deployments, Megapack 3 / Megablock unveiled; expanding AI inference/training and a U.S. semi-conductor deal noted. This is the clearest re-rating vector beyond autos.

________________________________________

🛡️ 8) Safety, Regulatory & Governance Risk — 7.5/10 (risk) (↑ risk)

• New NHTSA probe into FSD reporting/behavior escalates headline risk; audit scrutiny persists. Interpret higher score here as more material risk to multiple.

________________________________________

🚩 9) Competition & Global Share — 6.2/10 (↔)

• Competitive intensity in China/EU remains high; Q3 execution improved but pricing power still contested.

________________________________________

🌐 10) Macro & Trade/Policy — 6.5/10 (↑)

• Policy shifts (e.g., OBBB tax-credit sunset; tariff/trade uncertainty) remain a swing factor for cost & demand corridors.

________________________________________

✅ 11) Commodities/Inputs — 5.5/10 (↔)

• Mixed moves across lithium/nickel; no single driver eclipses execution/AI narrative near term.

________________________________________

Updated Catalyst Scorecard (ranked by impact)

1. Autonomous & Robotaxi Execution — 9.2

2. Energy, AI & Optimus Optionality — 8.7

3. EV Demand & Geographic Mix — 8.6

4. Battery Cost & Margin Levers — 8.3

5. Affordable Model / Next-Gen — 8.0

6. U.S. EV Incentives — 6.0

7. Rates & Credit — 6.5

8. Macro/Trade — 6.5

9. Competition/Share — 6.2

10. Safety/Reg/Gov Risk — 7.5 (risk flag)

11. Commodities — 5.5

(Key Q3 facts from Tesla’s deck; probe/tax-credit items from NHTSA/IRS reporting.)

________________________________________

📊 Analyst Rankings & Price Targets

• Street consensus (near-term 12-mo): ~$391 average target; consensus rating: Hold across ~46 firms.

• Bull camp: Wedbush (Dan Ives) $600 PT (reiterated Nov-5; Street-high; thesis = embodied-AI/robotics optionality + robotaxi). Benchmark $475 Buy (post-Q3).

• Cautious/negative: UBS $247 Sell (raised from $215 but still bearish on deliveries/margins).

• Tape-check from Tesla: Q3-25 revenue $28.1B, non-GAAP EPS $0.50, record FCF, record deliveries & storage. (EPS miss vs some expectations; revenue beat.)

________________________________________

🔍 Headlines that moved the needle

• NHTSA opens new FSD probe (scope ~2.9M vehicles).

• FSD v14 (Supervised) broad rollout; AI capacity to ~81k H100-eq; Bay Area robotaxi ride-hailing noted (Q3 deck).

• OBBB EV tax credits sunset 9/30/25; binding-contract/time-of-sale guidance enables limited post-deadline claims.

• Q3 print: record deliveries, record energy storage, record FCF; EPS light vs some models but narrative shifts to AI/energy.

________________________________________

🧭 Technicals: Levels & Structure (weekly focus)

Primary structure: since late-2022, TSLA’s traded inside a contracting wedge, with noteworthy compression into 2H-2025—typical of late-stage accumulation before a decisive break. Momentum divergences are improving on weekly frames even as price consolidates.

________________________________________

Key levels (spot-agnostic):

• Support: $360–$370 (prior breakdown area/weekly shelf); $330–$345 (multi-touch base/pivot); $310–$320 (cycle risk zone).

• Resistance: $405–$420 (range top & supply), $450–$475 (post-robotaxi pop zone / analyst PT cluster), $500 (psych), then $600–$650 (LT measured target band).

• Roadmap Expect one more downside probe into $310–$320 in Q1-2026 to complete the wedge, then trend break and resume bull leg toward $600/$650 over the subsequent cycle (≈ ~100% off the projected low).

• Risk markers: sustained weekly closes < $305 would postpone the “final low” timing and force a re-mark to the 200-week MA cluster; weekly closes > $475 accelerate the upside timing toward the $500/$600 handles.

________________________________________

Cases unchanged framework

• Bull: Robotaxi expands to more metros, regulators settle into a supervised-AV regime, energy/AI scale continues; market re-rates to $475–$600 (Benchmark/Wedbush anchors).

• Base: Solid execution across autos + energy, FCF stays healthy, autonomy rolls out cautiously under oversight; stock tracks Street $350–$400 band.

• Bear: Delivery softness post-credit-sunset, tougher pricing in China/EU, or adverse NHTSA actions; retest of $300–$330 zone before trend resolution.

________________________________________

What to watch next (60–90 days)

1. NHTSA probe path and any software/recall remedies.

2. Robotaxi geographic expansion cadence and any shift from safety-monitor to remote-assist ops.

3. Energy bookings & Megapack 3/Megablock ramp against utility RFP calendars.

4. Delivery run-rate post-credit sunset and mix of Standard trims.

________________________________________

RACE

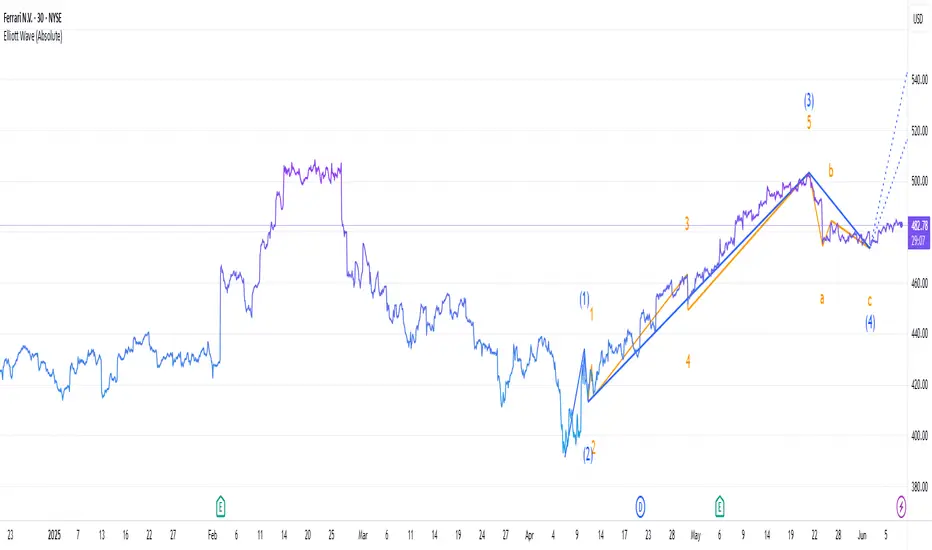

Ferrari RACE Technicals Led Entry With 100% Upside in 2026

RACE is in a measured correction after its July 2025 ATH (~$517). A repeat of prior ~35% corrections (2018/19; 2022) implies a symmetry target near ~$336 (35% off $516), creating a high-quality “buy the pullback” setup for smart investors willing to scale in before fundamentals re-assert. With the current price around ~$400, a full 35% retrace would complete near the low-$330s; prior cycles then delivered outsized recoveries. We view the $330–$360 zone as a strategic accumulation area for 100%+ multi-year upside potential, with a 2026 bull target >$700 assuming backlog support, margin resilience, and successful new product execution. ATH/price data cross-checked from market sources.

________________________________________

Executive Summary

• Thesis: Ferrari remains the purest “luxury-automotive as luxury-goods” equity: scarce supply, sold-out order book into 2026, rising personalization, and a carefully staged electrification roadmap supported by the new Maranello e-building. Even with macro or tariff noise, Ferrari’s brand, pricing power, and capital discipline underpin premium multiples.

• Why now: The stock’s technical correction is doing the valuation work for you. Into weakness, we favor staged entries ahead of 2026 catalysts EV debut & deliveries; new model cadence; ongoing buybacks.

• Key risks we underwrite: macro wealth shocks; execution on first BEV; regulatory/tariff volatility; FX EUR/USD; and luxury demand rotation. Offsetting: backlog visibility, personalization mix, and buybacks.

________________________________________

Ferrari (RACE) Catalyst Scorecard and 2026 Outlook

1) 🏎 New Model Launches & Portfolio — 9/10

Fresh models e.g., Roma Spider, 296 family, 12Cilindri plus track-focused/limited series sustain mix and ASPs. Purosangue remains capacity-constrained by design ≤~20% of shipments, supporting scarcity. Notes: media and management have repeatedly referenced Purosangue caps and order pauses. Rumor watch: the market expects additional halo launches into 2026; specifics beyond official IR should be treated as provisional.

2) 🔌 EV & Hybrid Transition — 9/10

Ferrari’s e-building went live in 2024 to manufacture ICE, hybrid, and the first BEV, enabling in-house e-axles/battery work and flexible capacity. Management reiterated an EV unveiling in October 2025 with sales beginning 2026; external reporting often cites incremental capacity of ~6,000 units management hasn’t fixed a public number. Strategy: electrify without diluting brand character.

3) 💰 Pricing Power & Personalization — 9/10

Personalizations are a structurally expanding, high-margin revenue stream—running ~~20% of revenues by 2025 commentary—while ultra-limited models e.g., Daytona SP3, 499P Modificata add mix tailwinds. Ferrari consistently emphasizes “quality of revenues over volume.”

4) 🌍 Global Demand & Wealth Resilience — 8/10

Order visibility remains exceptional, with management and financial press citing books effectively filled into 2026 even amid tariffs and China softness; U.S./EU/Middle East wealth pools anchor demand. Hybrids already approach half of deliveries, de-risking compliance.

5) 📈 Order Backlog & Supply Discipline — 8/10

Production is deliberately capped; Purosangue constrained to protect exclusivity. Backlog sold-out deep into 2026 reduces cyclicality and protects margins through mix and scarcity.

6) 💵 Shareholder Returns & Capital Allocation — 7.5/10

Ferrari is methodically executing a multi-year €2bn buyback through 2026 alongside dividends, while maintaining heavy R&D and capex for electrification and new platforms. Recent IR updates confirm ongoing tranches.

7) ⚖ Tariffs & Trade — 7/10

The 2025 U.S.–EU deal reduced tariff pressure versus prior peaks, a modest tailwind to margins and pricing optics for EU autos; Ferrari has shown ability to pass costs to clientele.

8) 🏆 Brand & Competitive Moat — 9/10

Ferrari’s moat resembles top luxury houses more than automakers: waiting lists, repeat/collector buyers, F1 halo, and unrivaled pricing power. This underpins luxury-goods-like multiples and high returns. (Multiple third-party and IR references.)

9) ⚔ Competition & Luxury Peers — 6/10

Peers Lamborghini, McLaren, Rimac, etc. lack Ferrari’s breadth/brand equity. Luxury EV entrants pose incremental risk, but Ferrari’s pacing plus customer loyalty mitigate. General industry assessment; monitor EV launches from peers.

10) 📉 Macro & Economic Cycle — 6/10

Ferrari isn’t immune to wealth drawdowns; however, backlog and personalization provide buffers. Management has historically protected price/mix by flexing volumes if needed.

________________________________________

2026 Outlook What Must Go Right

• EV milestone: Successful first-BEV launch & deliveries with waitlists experience parity with hybrids; no brand dilution.

• Mix strength: Purosangue/12Cilindri/hyper/limited series maintain ASPs and margins; personalization share inches higher.

• Financial delivery: Hitting or beating upgraded plan markers into 2026 after Ferrari indicated it is tracking ahead on profitability versus the original 2026 targets.

• Capital returns: Continued cadence on the €2bn buyback; dividend growth within FCF discipline.

________________________________________

Valuation Snapshot

• Quality context: Ferrari’s 2024 print and IR commentary emphasize expanding mix/personalization and ahead-of-plan profitability into 2025/26. Refer to FY24 results + CMD updates.

• Peer framing: Treat RACE as luxury Hermès-like scarcity rather than auto OEM. This justifies premium EV/EBITDA and P/E vs mass OEMs, provided growth/margins hold.

• Multiple work: On pullbacks to the mid-$300s, implied 2026E EV/EBITDA compresses to attractive territory vs luxury comps assuming consensus-style growth/margins investors should plug house estimates.

________________________________________

Scenarios & Targets

• Bull ($700–$750) — Successful BEV introduction, backlog conversion, personalization >20% of sales, steady buybacks, and benign macro.

• Base ($580–$620) — Order book carries revenues; margins hold with disciplined volumes; EV ramps without profit drag.

• Bear ($350–$400) — Wealth shock or EV stumble; cancellations rise, mix weakens; tariff/FX pressure re-rates the multiple. Risk case consistent with technical $330s correction.

________________________________________

Entry & Risk Management Plan

• Where to buy: Scale in $360–$380; add aggressively $330–$360 35% measured-move zone.

• Sizing: For a diversified HNWI book, a core 1.5–3.0% NAV position, with room to add +100–150 bps on capitulation into the $330s.

• Stops/hedges: Soft stop on a decisive weekly break <$320; hedge via short auto-luxury basket or long USD if EUR strength risks translation.

• Time horizon: 18–30 months through 2026 catalysts.

________________________________________

Near-Term Catalyst Timetable rolling 12–18 months

• Oct 2025–1H 2026: First Ferrari BEV unveil → initial deliveries watch order intake, waitlist depth, option take-rate, margin commentary.

• Ongoing 2025–26: Buyback tranches; monitor IR posts for pace/size.

• Quarterlies/Capital Markets updates 2025–26: Mix/personalization trajectory; backlog commentary; Purosangue allocation discipline.

Ferrari (RACE) Catalyst Scorecard AND 2026 OutlookFerrari (RACE) Catalyst Scorecard AND 2026 Outlook

________________________________________

1. 🏎 New Model Launches & Portfolio (9/10)

Ferrari’s 2023–26 lineup is packed with high-end launches. Recent additions include the Roma Spider, SF90 XX, 296 Challenge, and 499P Modificata. Demand for the Purosangue SUV has been overwhelming, with early orders suspended and deliveries backlogged into 2026. Coming next: the 849 Testarossa plug-in hybrid deliveries H2 2025/Q1 2026 and the F80 hybrid hypercar limited series, ~1,200 hp. These models should sustain ASP growth and keep exclusivity intact.

________________________________________

2. 🔌 EV & Hybrid Transition (9/10)

Ferrari is phasing electrification deliberately. After hybrids like the SF90 and 296, Ferrari will unveil its first fully electric car in October 2025 deliveries start 2026. A new “e-building” in Maranello is ready to expand capacity by ~6,000 units annually. Ferrari is building in-house motors and batteries while still pledging to keep V12 ICE alive as long as possible. This balance between heritage and compliance ensures both regulatory cover and customer enthusiasm.

________________________________________

3. 💰 Pricing Power & Personalization (9/10)

Ferrari’s bespoke strategy fuels unmatched pricing power. Recent results showed hundreds of millions in incremental profit from high-priced halo models Daytona SP3, 499P Modificata and personalization demand. Personalization now represents nearly one-fifth of revenues. Carefully managed price hikes on core models, combined with ultra-limited editions, cement Ferrari’s position as the most profitable automaker per unit.

________________________________________

4. 🌍 Global Demand & Wealth Resilience (8/10)

About three-quarters of Ferrari’s sales go to repeat customers, and nearly half to collectors owning multiple Ferraris. The expanding global wealthy class adds to the demand pool. Ferrari’s sales are well balanced across regions; China is only ~10%, limiting exposure to that slowdown. Wealth concentration in the U.S., Europe, and the Middle East provides resilience against macro shocks.

________________________________________

5. 📈 Order Backlog & Supply Discipline (8/10)

Ferrari’s order book is sold out through 2026/early 2027. The company deliberately caps production e.g. Purosangue SUV shipments limited to ~20% of total to preserve scarcity. This ensures pricing discipline and supports margin expansion. With supply tightly managed, Ferrari avoids the discounting and inventory overhangs that plague mass-market automakers.

________________________________________

6. 💵 Shareholder Returns & Capital Allocation (7.5/10)

Ferrari’s capital return story is strong. Annual dividends and share buybacks together exceed €750 million. The €2 billion buyback program through 2026 is ongoing. At the same time, Ferrari invests aggressively in R&D e-building, hybrid/EV systems without margin erosion. The balance between shareholder distributions and future growth spending is a key investor confidence driver.

________________________________________

7. ⚖ U.S./EU Tariffs & Trade (7/10)

A recent U.S.–EU deal cut auto tariffs, enabling Ferrari to avoid planned price hikes in the U.S. and improving margins slightly. Regulatory pressure on emissions is real, but Ferrari’s measured EV roadmap addresses compliance. Trade risks are less critical for Ferrari than for volume automakers, but favorable deals add incremental margin upside.

________________________________________

8. 🏆 Brand & Competitive Moat (9/10)

Ferrari’s brand power is unmatched. It combines scarcity, desirability, and F1 heritage to justify luxury-goods multiples more in line with Hermès than Porsche. The brand enables Ferrari to command unmatched ASPs and maintain margins north of 25%. Ferrari’s intangible moat protects it against both cyclical demand dips and competitive threats.

________________________________________

9. ⚔ Competition & Luxury Peers (6/10)

Direct competitors—Lamborghini, McLaren, Rimac—lack Ferrari’s scale, heritage, and breadth. Luxury EV entrants pose some risk, but Ferrari’s controlled rollout and customer loyalty limit the threat. Peer comparisons place Ferrari firmly alongside high-end luxury brands, not mass-market automakers, underscoring its unique positioning.

________________________________________

10. 📉 Macro & Economic Cycle (6/10)

Ferrari is somewhat insulated but not immune. A sharp global downturn or wealth destruction could dampen orders. However, its backlog, exclusivity, and personalization revenue provide cushions. Even in recessions, Ferrari can slow production and still maintain pricing power.

________________________________________

Catalyst Scorecard

Rank Catalyst Score

1 New Model Launches & Portfolio 9.0

2 EV & Hybrid Strategy 9.0

3 Pricing Power & Personalization 9.0

4 Brand & Competitive Moat 9.0

5 Global Demand & Wealth Trends 8.0

6 Order Book & Supply Discipline 8.0

7 Shareholder Returns 7.5

8 U.S./EU Tariffs & Trade 7.0

9 Competition & Luxury Peers 6.0

10 Macro & Economic Cycle 6.0

________________________________________

Valuation Scenarios

• Bull Case ($700–$750): Successful EV debut, robust demand for new models, strong margins, continued buybacks.

• Base Case ($580–$620): Order backlog supports steady revenue growth, modest EV contribution, pricing discipline.

• Bear Case ($350–$400): Macro downturn or execution missteps lead to cancellations and lower margins.

TSLA path to 550/650 USD Breakout Still Pending🔥 What specifically drives TSLA into 550–650

📦 Deliveries + mix surprise

If unit volumes beat whisper numbers and mix favors higher-trim/FSD attach, you get more gross profit per vehicle without needing price hikes. Watch the cadence of regional incentives and shipping vectors; strong NA/EU mix plus improving China utilization is the sweet spot.

🛠️ Margin stabilization → operating leverage

Gross margin base effect + opex discipline = powerful flow-through. Even a 100–150 bps lift in auto GM, coupled with energy GM expanding as Megapack scales, can push operating margin into low-mid teens. That alone recodes the multiple market is willing to pay.

🔋 Energy storage stepping out of auto’s shadow

Megapack/Powerwall growth with multi-GW backlogs turns “side business” into a credible second engine. As deployments and ASP/contract mix normalize, investors begin modeling $10–$15B annualized energy revenue with attractive GM — this is multiple-expanding because it looks more like infrastructure/software-tinted industrials than cyclical autos.

🤖 Autonomy & software monetization bridges

Two things move the needle fast: (1) clear progress toward supervised autonomy at scale (drives FSD attach + ARPU), and (2) licensing (FSD stack, charging/NACS, drive units). Even modestly credible paid-miles/seat-based models (think $50–$150/month vehicles on fleet) transform valuation frameworks.

🦾 Optimus/robotics as a real option, not sci-fi

The market doesn’t need commercial ubiquity — it needs line-of-sight to pilot deployments and unit economics where labor-substitute ROI < 3 years. A few high-credibility pilots (warehousing, simple assembly, logistics cells) can tack on optionality premium that pushes the multiple toward the top of the range.

💹 Options-market reflexivity

Flows matter. Elevated call demand near ATH turns dealers short gamma, forcing delta hedging that lifts spot, which triggers more call buying → a familiar feedback loop. On breakouts, watch open interest skew to short-dated OTM calls, and put-call ratios compressing; these magnify upside in a tight float day.

🌍 Macro & liquidity

If indices hold highs and the rate path doesn’t tighten financial conditions, growth duration gets rewarded. TSLA’s beta + story premium thrives in that regime.

________________________________________

🧠 Outside-the-box accelerants

🛰️ “Software day” packaging

A coordinated showcase that bundles FSD progress, energy software (fleet, VPP), service/insurance data, and Optimus pilots into a single capital-markets narrative could reframe TSLA as a platform. The Street responds to packaging; it compresses time-to-belief.

🤝 Third-party FSD/charging licensing headlines

A single blue-chip OEM announcing software licensing + NACS deep integration reframes the competitive landscape. The equity market pays a software multiple for recurring seats.

🏗️ Capex signaling for next-gen platform without GM hit

Announcing a modular, high-throughput manufacturing scheme (cell to structure, gigacasting tweaks, logistics compression) with proof that unit economics are accretive from ramp can flip skeptics who anchor to past ramp pain.

⚡ Grid-scale contracts + financing innovation

If Tesla pairs utility-scale storage with project-level financing (think repeatable ABS-like channels for Megapack), you de-risk cash conversion cycles and unlock a new investor constituency (infrastructure/green income). That tightens the multiple.

________________________________________

🏎️ Comparative playbook: RACE (Ferrari) & NVDA (NVIDIA)

👑 RACE — the scarcity & brand ROIC lens

Ferrari’s premium multiple rests on scarcity, orderbook visibility, and brand pricing power. TSLA doesn’t have scarcity, but it can borrow the RACE lens via (a) limited-run, ultra-high-margin trims that anchor halo pricing, (b) waitlist-like energy backlogs that create visibility, and (c) bespoke software packages that mimic “personalization” margin. In bull phases, RACE trades as a luxury compounder rather than an automaker; TSLA can earn a slice of that premium when the energy + software story dominates.

🧮 NVDA — the flywheel & supply-constrained S-curve

NVIDIA’s explosive run blended (1) clear demand > supply, (2) pricing power, (3) ecosystem lock-in. TSLA’s battery and compute stacks can echo that dynamic: limited 4680/cell supply + Megapack queues + proprietary autonomy data moat. The moment the market believes TSLA is supply-gated (not demand-gated) in energy/AI, it will award NVDA-like scarcity premia. Add toolchain stickiness (training data, fleet miles, Dojo/AI infra), and you get ecosystem multiples rather than auto multiples.

📊 What the comps teach for TSLA’s 550–650 zone

• RACE lesson: visibility + pricing power boost the quality of earnings → higher P/E durability.

• NVDA lesson: credible scarcity + platform control turbocharge EV/Sales and compress the market’s time-to-future state.

• Translation for TSLA: blend of luxury-like quality (energy contracts + premium trims) and platform scarcity (cells/AI stack) → multiple rerate into our target band.

________________________________________

🧾 Valuation outlook

🧮 Earnings path

• Units up mid-teens % Y/Y; ASP stable to slightly higher on mix; energy + software up strongly.

• Auto GM +100–150 bps; Energy GM expands on scale; opex +SMC disciplined → op margin 12–15%.

• Share count glide modest. Forward EPS ≈ $9–$11.

• Multiple: 50× (conservative growth premium) → $450–$550; 60× (software/autonomy visibility) → $540–$660.

• Why the market pays up: visible recurring high-margin lines (FSD, energy software, services) + AI/robotics optionality.

📈 EV/Sales path

• Forward revenue $130–$150B (auto + energy + software/services).

• Assign blended EV/Sales 6.5–7.5× when energy/software dominate the debate.

• Less net cash → equity value per share in $550–$650.

• Check: At 7× on $140B = $980B EV; equity ≈ $1.0–$1.1T with cash, divided by diluted shares → mid-$500s to $600s. Momentum premium and flow can extend to upper bound.

________________________________________

🧭 Technical roadmap & market-microstructure

🧱 Breakout mechanics

A decisive weekly close above prior ATH with rising volume and a low-volume retest that holds converts resistance to a springboard. Expect a “open-drive → pause → trend” sequence: day 1 impulse, 2–5 sessions of rangebuilding, then trend resumption.

🧲 Volume shelves & AWVAPs

Anchored VWAPs from the last major swing high and the post-washout low often act like magnets. Post-break, the ATH AVWAP becomes first support, then the $500 handle functions as the psychological pivot. Above there, $550/$590/$630 are classical measured-move/Fib projection waypoints; pullbacks should hold prior shelf highs.

🌀 Options & dealer positioning

On a break, short-dated OTM calls populate 1–2% ladders; dealers short gamma chase price up via delta hedging. Expect intraday ramps near strikes (pin-and-pop behavior) and Friday accelerants if sentiment is euphoric. A steepening skew with heavy call open interest is your tell that supply is thin.

________________________________________

🧨 Risks & invalidation

🚫 Failed retest below the breakout shelf (think: a fast round-trip under the $4-handle) downgrades the setup from “trend” to “blow-off.”

🧯 Margin or delivery disappointments (e.g., price-war resumption, regional softness) break the EPS/EV-Sales bridges.

🌪️ Macro shock (rates spike, liquidity drains) compresses long-duration multiples first; TSLA is high beta.

🔁 Flow reversal — if call-heavy positioning unwinds, gamma flips to a headwind and accelerates downside.

________________________________________

💼 Trading & portfolio expressions for HNWI

🎯 Core + satellite

Hold a core equity position to capture trend, add a satellite of calls for convexity. If chasing, consider call spreads (e.g., 1–3 month $500/$600 or $520/$650) to tame IV.

🛡️ Risk-managed parity

Pair equity with a protective put slightly OTM or finance it with a put spread. Alternatively, collars (write covered calls above $650 to fund downside puts) if you’re guarding a large legacy stake.

⚙️ Momentum follow-through

Use stop-ins above key levels for systematic adds, and stop-outs below retest lows to avoid round-trips. Size reduces into $590–$630 where target confluence lives; recycle risk into pullbacks.

💵 Liquidity & slippage

Scale entries around liquid times (open/closing auctions). For size, work algos to avoid prints into obvious strikes where dealers can lean.

________________________________________

🧾 Monitoring checklist

🔭 Delivery run-rate signals (regional registration proxies, shipping cadence).

🏭 Margin tells (bill of materials trends, promotions cadence, energy deployment updates).

🧠 Autonomy milestones (software releases, safety metrics, attach/ARPU hints).

🔌 Licensing/partnership beats (NACS depth, FSD/AI stack interest).

📊 Options dashboard (short-dated call OI ladders; put-call ratio shifts; gamma positioning).

🌡️ Macro regime (rates, liquidity, risk appetite).

________________________________________

✅ Bottom line

🏁 The 550–650 tape is not a fairy tale — it’s a stacked-catalyst + rerate setup where energy/software/autonomy rise in the narrative mix, margins stabilize, and options-market reflexivity does the rest. Execute the breakout playbook, respect invalidation lines, and use convex expressions to lean into upside while protecting capital.

esla (TSLA) — Breakout Playbook

🎯 Core Thesis

• Insider conviction: Musk’s ~$1B buy.

• Risk-on macro: equities at highs, liquidity supportive.

• Options reflexivity: call-heavy flows can fuel upside.

• ATH breakout (~$480–$490) = gateway to price discovery.

________________________________________

🚀 Upside Drivers to $550–$650

• Deliveries & Mix: Surprise beat + higher trim/FSD attach.

• Margins: GM stabilization + energy scaling → op margin 12–15%.

• Energy: $10–15B rev potential with infra-like multiples.

• Autonomy/Software: FSD attach, ARPU, licensing.

• Optimus/Robotics: Pilot deployments → ROI < 3 yrs adds optionality.

• Licensing Headlines: OEMs adopting NACS/FSD stack.

• Capital Markets Narrative: Packaged “software + energy + robotics” story reframes Tesla as a platform.

________________________________________

🏎️ Comparative Bull Run Lens

• Ferrari (RACE): Scarcity, orderbook, luxury multiples.

• NVIDIA (NVDA): Scarcity + ecosystem flywheel → EV/Sales premium.

• Tesla Parallel: Blend of luxury quality (energy backlogs, halo trims) + AI scarcity (cells, fleet data, Dojo).

________________________________________

📊 Valuation Bridges

• EPS Path: $9–$11 EPS × 50–60× = $450–$660.

• EV/Sales Path: $130–150B revenue × 6.5–7.5× = $550–$650.

________________________________________

📈 Technical Roadmap

• Breakout > $490 → retest holds → next legs:

o $550 / $590 / $630 / stretch $650–$690.

• Watch anchored VWAPs; ATH shelf flips to support.

• Options chase accelerates above round strikes.

Is Ferrari's stock still bullish?Is Ferrari's stock still bullish?

Technical Outlook

Elliot Wave theory suggests a cautious bullish stance. The present correction seems to be a temporary setback, likely driven by guidance and tariff fears, but sets the stage for a potential rally to $520-$540 if support is not broken. However, risks of a deeper correction (i.e., to $420-$440) persist if pressures from the outside intensify.

The stock is currently trading above all three of its major EMA levels — daily, weekly, and monthly — that is a good technical signal. The rising daily EMA at 479.98 suggests that short-run momentum remains healthy. The weekly EMA at 461.77 provides medium-term support, while the monthly EMA at 421.08 supports the longer-term trend solidly.

Positive Sentiment Factors

Ferrari reported robust Q1 2025 results, with net revenues of €1.79 billion (up 13% YoY), an operating profit of €542 million (up 22.7%), and a net profit of €412 million (up 17%). Adjusted earnings per share were €2.30, surpassing analyst expectations of €2.28. This shows Ferrari’s strong pricing power and demand for personalized vehicles.

Analyst Sentiment: Optimism remains for Ferrari among some analysts. UBS raised its price target to $560 from $520, maintaining a Buy rating, with the new Ferrari Elettrica a major catalyst, the company said. Bernstein and RBC Capital maintained Outperform ratings on the stock at $575 and €500, respectively. Barclays upgraded Ferrari to Overweight, calling it a "safe haven" in a shaky European automotive environment.

Brand Strength and Strategic Positioning: Ferrari’s luxury brand and high demand for models like the Roma Spider, 296 GTS, SF90 XX, and Purosangue bolster its market position.

Neutral Sentiment Factors

Market and Industry Context: The broader market has been volatile due to trade developments and tariff relief rallies. Ferrari’s stock has been influenced by these macroeconomic factors, but its luxury positioning makes it less sensitive than mass-market automakers.

Formula 1 Performance: Ferrari’s underwhelming Formula 1 season, with McLaren significantly outscoring Ferrari in points poses some concern among investors. While this does not directly impact stock performance, it may indirectly affect brand sentiment among enthusiasts.

Negative Sentiment Factors

Tariff Concerns: Ferrari shares have been sensitive to Trump's U.S. tariff policies. A tariff increase would add up to $50,000 to the price of an average Ferrari, potentially cutting sales volumes in the U.S., which accounts for 28.8% of net sales. JPMorgan warned that tariff impacts might be "worse" for Ferrari, lowering the price target to $460 from $525

Conclusion

Ferrari stock has a bullish but cautious bias, supported by solid fundamentals, favorable technical momentum, and positive analyst sentiment on upcoming product releases such as the Ferrari Elettrica. Macro risks, however, including U.S. trade policy and market volatility, are still major overhangs.

TSLA New ATH incoming? Overview of primary catalysts.After trading between $346 and $365 intraday on May 27, Tesla shares closed at $362.89—up modestly despite broader market headwinds and lingering investor skepticism.

Here’s a detailed breakdown of the primary catalysts shaping Tesla’s stock price (ranked 0–10):

1. Electric Vehicle Demand Growth

Strength: 9/10

Global EV adoption remains the single largest driver of Tesla’s top line. Despite slowing sales in Europe and China, overall EV penetration continues to surge as consumers shift away from internal-combustion engines.

2. Launch of Affordable Model (Entry-Level EV)

Strength: 8.5/10

Elon Musk has reiterated plans to unveil a sub-$25,000 EV in early 2025, targeting the mass market. Investors cheered a recent reaffirmation of focus on core products over peripheral projects.

3. Battery Cost Reductions & Margin Expansion

Strength: 8/10

Tesla’s relentless drive to lower battery pack costs underpins both profitability and price competitiveness. Q4 cost of goods sold dipped below $35,000 per vehicle, even as margins softened amid mixed volumes.

4. Autonomy & Robotaxi Progress

Strength: 7.5/10

Commercial robotaxi trials are slated to begin in Austin in June 2025, with a dedicated Cybercab in development. While regulatory and safety hurdles loom, the promise of recurring software subscription revenue could be transformative.

5. Competition from Other EV Manufacturers

Strength: 7/10

Legacy automakers and startups alike are ramping up EV offerings. Tesla’s U.S. market share has declined in recent years, highlighting intensifying pressure in key regions.

6. U.S.–China Trade Policies & Tariffs

Strength: 6.5/10

Fluctuating tariffs on Chinese EV imports have led to order suspensions and forecasting challenges. Trade-policy uncertainty remains a wild card given Tesla’s global supply chain.

7. Regulatory Incentives & Subsidies

Strength: 6/10

U.S. federal tax credits under the Inflation Reduction Act and similar programs in Europe and China support EV demand—and Tesla’s eligibility criteria will influence its market growth.

8. Commodity Price Volatility (Lithium, Nickel, Cobalt)

Strength: 5.5/10

Raw material cost swings can erode margins. While long-term supply agreements help, spot shortages or price spikes remain risks.

9. Fed “Higher for Longer” Interest Rate Environment

Strength: 5/10

Elevated real yields reduce the appeal of high-growth names like Tesla. A sustained hawkish stance from the Fed could continue to cap valuations, similar to how it weighs on non-yielding assets.

10. Corporate Governance & Elon Musk’s Public Profile

Strength: 4/10

Musk’s high-profile engagements and occasional controversies can politicize the brand, prompting sentiment-driven stock swings.

Catalyst Strength Rankings (May 2025)

🔸 EV demand growth: 9

🔸 Affordable Model launch: 8.5

🔸 Battery cost & margins: 8

🔸 Autonomy/robotaxi progress: 7.5

🔸 Competition: 7

🔸 Trade & tariffs: 6.5

🔸 Regulatory incentives: 6

🔸 Commodity costs: 5.5

🔸 Fed rates: 5

🔸 Musk profile: 4

Analyst Forecasts for 2025

| Analyst / Consensus | 12-Month Price Target | Rating |

| --------------------------- | --------------------- | ------------ |

| High | \$470.00 | – |

| Median | \$306.00 | Hold/Neutral |

| Low | \$115.00 | – |

| Average (Consensus) | \$306.29 | Hold |

| Dan Ives (Wedbush) | \$315 | Outperform |

| Adam Jonas (Morgan Stanley) | \$430 | Overweight |

* Consensus sees a range of \$115–\$470 with an average near \$306.

* Dan Ives trimmed his target from \$550 to \$315, citing tariff risks and political headwinds.

* Adam Jonas remains bullish with a \$430 target, viewing Tesla as an “embodied AI compounder” despite near-term brand challenges.

Where to Next for Tesla?

* Current price: \~\$362.89

* Key support levels: \$350 and \$340

* Next technical floor: \$330

* Upside triggers: Stronger-than-expected delivery volumes, breakthrough in full-self-driving (FSD) reliability, or renewed cost cuts.

Tesla’s stock remains a balance between long-term disruptive potential and short-term execution risks. While EV adoption and autonomous ambitions underpin a compelling growth narrative, margin compression, competitive pressures, and macro uncertainties will dictate volatility in the months ahead.

RACE (Ferrari) LONG SET UPEntry 1 $450.00

Entry 2 $440.00

Stop loss $430.00

Take profit 1- $460

(Close 33%)

Take profit 2- $480.00

(Close 66%)

Take profit 3-$500.00

(Close 100%)

RACE (Ferrari) – Quality has its PriceMIL:RACE has a technically interesting setup that also fits well with the weekly setup that I presented a few weeks ago.

The current consolidation has once again reached the lower zone and should find support from here one more time. Recently, a significant bounce was achieved from here several times. In addition, Ferrari is moving at the daily SMA 200 line and has bounced upwards from this (as well as from the horizontal support). In the 4h chart we see a nice RSI divergence as well as a breakout from a falling wedge. Both bullish signals.

Fundamentally, Ferrari is not cheap, but quality has its price. The backlog extends years into the future, the pre-order lists are full to bursting, the line-up presented is technically flawless and in demand and the cash flow is immense. In addition, the company is still family-owned (which secures the share price) and the current F1 season with Hamilton and Leclerc as the team should also be interesting.

We are initially targeting the area around EUR 438 and then the previous ATH at EUR 457. This results in an ROI of 10%. Should the daily closing price fall below EUR 400, the trade would be disqualified and closed.

Target zones

438 EUR

457 EUR

Support Zones

400 EUR

75% gains TSLA Best Level to BUY/HOLD🔸Hello traders, today let's review 12hour price chart for TSLA.

Recently we gapped up on higher volume, we got two liquidity

gaps below market overall this indicates strength, having said

that there is heavy fresh overhead supply zone so expecting pullback.

🔸Fresh supply zones at 400/375/305 usd will provide liquidit for

a potential pullback in TSLA. fresh demand zones located below market

at 230/235 usd and 190 usd. most likely limited downside below fresh

liqudity at 230/235 usd.

🔸Recommended strategy bulls: expecting measured move pullback

once we trigger fresh supply zone near 300/305 usd, bulls should

wait for the pullback to trigger fredh demand/liquidity zone at/near

230/235 USD. BUY/HOLD after pullback TP1 375 USD TP2 400 USD.

75% gains potential for patient traders. good luck!

🎁Please hit the like button and

🎁Leave a comment to support our team!

RISK DISCLAIMER:

Trading Futures , Forex, CFDs and Stocks involves a risk of loss.

Please consider carefully if such trading is appropriate for you.

Past performance is not indicative of future results.

Always limit your leverage and use tight stop loss.

Best Level to BUY/HOLD TSLA 100% upside TP 500/550 USD🔸Hello traders, today let's review 8hour chart for TSLA. Entering re-accumulation stage now, expecting range bound trading during next few weeks as we enter pullback/correction. We are closing in on heavy overhead resistace / limited upside currently.

🔸The speculative chart pattern is bullish C*H in progress, expect more range locked price action for a few weeks as we re-accumulate and get ready to clear the overhead resistances. Measured move price projectiong for the C*H structure is 500/550 USD, 100%+ upside from the recommended BUY ZONE.

🔸Recommended strategy bulls: wait for TSLA to re-accumulate in the sliding bull flag formation into the liquidity zone and get ready to BUY/HOLD low near 220 USD, target based on measured move projection is 550 USD. good luck traders!

🎁Please hit the like button and

🎁Leave a comment to support our team!

RISK DISCLAIMER:

Trading Futures , Forex, CFDs and Stocks involves a risk of loss.

Please consider carefully if such trading is appropriate for you.

Past performance is not indicative of future results.

Always limit your leverage and use tight stop loss.

Can NVDA hit 200 USD in Q1 2025?🔸Time to update the NVDA trade setup, previously was expecting

a correction in this market, based on fundamentals we are definitely

overextended, however NVDA so far is trading purely based on momentum

ignoring the fundumentals. It's the star stock of the 2024 stock market.

🔸Previous strong uptrend, we broke above key psychological S/R at 100 usd. Right now we got a compression setup, expecting limited upside / pullback heading into US elections, having said that probably any downside beyond 115/120 usd is very limited. current floor set at 100/110 USD.

🔸Compressing into wedge formation, most likely we will break out

to the upside following a shallow pullback in November 2024.

Also November/December is a very strong seasonal period for US stock

market, so it's really hard to recommend short selling NVDA.

🔸Recommended strategy bulls: expecting pullback near 114/118 USD

in November going into elections, limited downside beyond 110 USD.

BUY/HOLD near 114/118 TP bulls is 200 USD, which is almost 75% upside.

Most likely we will reach target somewhere in Q1 2025, probably January.

🎁Please hit the like button and

🎁Leave a comment to support our team!

RISK DISCLAIMER:

Trading Futures , Forex, CFDs and Stocks involves a risk of loss.

Please consider carefully if such trading is appropriate for you.

Past performance is not indicative of future results.

Always limit your leverage and use tight stop loss.

RACE (Ferrari N.V.) BUY TF M15 TP = 479.50On the M15 chart the trend started on Oct.3. (linear regression channel).

There is a high probability of profit taking. Possible take profit level is 479.50

This level, which I have outlined above, is certainly not a “finish” level. But it is the level that has the “highest percentage of hits on target.”

Using a trailing stop is also a good idea!

Please leave your feedback, your opinion. I am very interested in it. Thank you!

Good luck!

Regards, WeBelievelnTrading

TSLA Best Level to BUY/HOLD 30% gains ABCD fractal🔸Hello traders, today let's review 4hour price chart for TSLA.

Recently we gapped down back into trading range, based on previous

update I still maintain neutral outlook until we complete the

re-accumulation structure, details see idea below.

🔸Having said that I'm expecting a decent 30% bounce in TSLA based

on the ABCD price fractal. ABCD fractal from 2023 projected into

the current market structure, point D expected near 188 usd timewise

most likely December/January. This will be a good reload for the bulls.

🔸Recommended strategy bulls: Bulls wait for pullback to complete

near 188 / point D and BUY/hold for a 30% bounce play. Exit/TP at 250 USD.

good luck traders!

🎁Please hit the like button and

🎁Leave a comment to support our team!

RISK DISCLAIMER:

Trading Futures , Forex, CFDs and Stocks involves a risk of loss.

Please consider carefully if such trading is appropriate for you.

Past performance is not indicative of future results.

Always limit your leverage and use tight stop loss.

Can a Prancing Horse Outrun an Electric Future?In the ever-evolving landscape of luxury automobiles, Ferrari stands as a beacon of innovation and exclusivity. The recent upgrade from J.P. Morgan, elevating Ferrari's status from "Neutral" to "Overweight," underscores the company's resilience and strategic prowess in navigating complex market dynamics. This vote of confidence, coupled with a substantial increase in the price target to $525, reflects Ferrari's unique position in the luxury sector and its ability to maintain growth even in the face of global economic challenges.

At the heart of Ferrari's success lies a paradoxical strategy that defies conventional wisdom: deliberately producing fewer cars than the market demands. This approach, rooted in the vision of founder Enzo Ferrari, has cultivated an environment of perpetual desire and scarcity. With a staggering backlog of 24 to 30 months, Ferrari has not only engineered exceptional vehicles but has also orchestrated an "underappreciated cultural evolution" within the company. This disciplined approach to growth, combined with the power to command premium prices, provides unparalleled visibility into future earnings and sets Ferrari apart from its luxury peers.

As the automotive industry races towards electrification, Ferrari is poised to redefine the boundaries of performance and sustainability. The company's foray into the electric vehicle market, promising an "incredible driving experience" that remains true to the Ferrari ethos, demonstrates its commitment to innovation while preserving its core values. However, this journey is not without obstacles. Ferrari must navigate challenges such as an ongoing investigation into its chairman and the conclusion of a key partnership with Santander. Yet, with strong financial performance, positive investor sentiment, and a clear strategic vision, Ferrari appears well-equipped to maintain its pole position in the luxury automotive market, promising a future as thrilling and exclusive as its storied past.

Ferrari Reported an Increase in Core Earnings Stock Down 0.61%Ferrari reported a 13% increase in core earnings in the first quarter of 2021, but its shares fell as the luxury sports car maker failed to excite investors. The Italian company said its quarterly results were boosted by pricing power, the mix of product sales, and a greater contribution from personalized vehicles. It also cited rising deliveries of its 2 million euro ($2.2 million) limited-series Daytona SP3 model. CEO Benedetto Vigna said Ferrari ( NYSE:RACE ) had produced double-digit growth for both revenue and profits despite stable car deliveries.

The company's adjusted earnings before interest, tax, depreciation and amortization (EBITDA) reached 605 million euros in January-March, in line with analyst expectations. However, shipment fell by seven units to 3,560, dragged by a 20% drop in the China, Hong Kong, and Taiwan region. Ferrari confirmed its forecast for full-year adjusted EBITDA to increase to at least 2.45 billion euros in 2024.

The company's net revenues of Euro 1,585 million, up 10.9% versus the prior year, with total shipments of 3,560 units $1flat versus Q1 2023. Adjusted EBIT(1) of Euro 442 million, up 14.8% versus the prior year, with adjusted EBIT(1) margin of 27.9%. Adjusted net profit of Euro 352 million and adjusted diluted EPS(1) at Euro 1.95 were up 12.7% versus the prior year, with adjusted EBITDA(1) margin of 38.2%.

The product portfolio in the quarter included nine internal combustion engine (ICE) models and four hybrid engine models, which represented 54% and 46% of total shipments, respectively. Revenues from Cars and spare parts were Euro 1,382 million, up 11.4% or 13.5% at constant currency(1). Sponsorship, commercial, and brand revenues reached Euro 145 million, up 11.6% or 12.0% at constant currency(1) attributable to new sponsorships, partially offset by lower Formula 1 ranking in 2023 vs. 2022. Other revenues were flat, with higher revenues from financial services activities offset by the decreased contribution from the Maserati contract which expired in 2023.

Currency had a negative net impact of Euro 26 million, mostly related to the Chinese Yuan, Japanese Yen, and US Dollar. Q1 2024 Adjusted EBITDA reached Euro 605 million, up 12.7% versus the prior year and with an Adjusted EBITDA(1) margin of 38.2%. Industrial free cash flow for the quarter was strong at Euro 321 million, driven by the increased Adjusted EBITDA, partially offset by capital expenditures of Euro 195 million and the increase in working capital, provisions, and other of Euro 71 million. As of March 31, 2024, the company was in a Net Industrial Cash position of Euro 38 million for the first time, compared to Net Industrial Debt of Euro 99 million as of December 31, 2023, also reflecting share repurchases of Euro 136 million.

Ferrari Races Higher, Bulls Eye $550 After Key Resistance BreakBuckle up, Ferrari (RACE) fans! The Italian Stallion is back in the driver's seat, and I am bullish after a crucial resistance level was shattered.

Ferrari stock surged past $370 resistance, a key technical hurdle that has capped the stock's potential for some time. This breakout suggests a bullish trend could be taking hold, with some expert analysts eyeing a potential surge to $550 in the coming months.

Ferrari Sets New Record Highs On Earnings

Ferrari (NYSE: NYSE:RACE ), the iconic luxury sports car manufacturer, is making headlines once again as its stock ( NYSE:RACE ) catapults to all-time highs, fueled by impressive Q4 earnings and the potential signing of Formula 1 legend Lewis Hamilton. The renowned racing driver, a seven-time World Drivers' Championship winner, could be donning the iconic red suit for Ferrari in the 2025 season, signaling a significant shift in the F1 landscape.

Earnings Triumph:

Ferrari ( NYSE:RACE ) reported Q4 adjusted earnings of 1.62 euros per share, exceeding forecasts with a 33% year-over-year increase. Net revenues for the quarter surged by 11% to 1.52 billion euros, surpassing FactSet analysts' expectations. The company delivered 1,493 cars to the EMEA market, while deliveries to the Americas rose by 6%. Despite a 25% drop in deliveries to China, Hong Kong, and Taiwan, Ferrari's ( NYSE:RACE ) overall performance paints a robust picture.

Full-year shipments rose by 3% to 13,663 vehicles, although China deliveries experienced a 4% decline. Notably, cars and spare parts revenue jumped by 12% to 1.29 billion euros for the quarter, showcasing the brand's enduring appeal and solid financial performance.

Strategic Guidance:

Ferrari ( NYSE:RACE ) provided optimistic guidance for 2024, expecting earnings to increase nearly 9% to 7.5 euros per share or more, with revenue projected to grow by about 7% to 6.4 billion euros or greater. Analysts at FactSet anticipate adjusted earnings of 7.53 euros per share on 6.45 billion euros in revenue, aligning with Ferrari's ( NYSE:RACE ) bullish outlook.

Lewis Hamilton's Potential Move:

In a surprising turn of events, reports suggest that Lewis Hamilton, a stalwart with Mercedes, might be on the verge of joining Ferrari ( NYSE:RACE ) for the 2025 season. The seven-time World Champion, who currently holds the record for the most Grand Prix victories at 103 wins, could form a formidable alliance with Ferrari's rising star, Charles Leclerc.

Hamilton's potential move adds an extra layer of excitement to the F1 narrative, as the partnership aims to challenge Red Bull's Max Verstappen, the current driver behind F1's dominance. If the speculated move materializes, it could mark a historic moment in the world of motorsports, bringing together one of the greatest drivers with one of the most iconic teams in the sport's history.

Market Reaction:

Investors responded swiftly to the positive earnings report and the Hamilton news, propelling Ferrari ( NYSE:RACE ) stock to a 12% surge to all-time highs. The move has positioned NYSE:RACE stock into a buy zone. The stock's strong ascent has also propelled it above its 50-day moving average, signaling continued market enthusiasm.

Conclusion:

Ferrari's ( NYSE:RACE ) record-breaking performance, both on the financial front and the potential addition of Lewis Hamilton to its roster, underscores the brand's enduring appeal and strategic vision for F1 dominance. As the luxury carmaker revs up for the future, investors and racing enthusiasts alike are eagerly anticipating the unfolding chapters in Ferrari's ( NYSE:RACE ) storied history. The convergence of financial success and high-profile partnerships positions Ferrari as a driving force in both the automotive and motorsports industries.

#RACE What recession? Ferrari racing away!i0.wp.com

Stock has broken out of this broadening pattern to reach new all-time highs with a measured target of at least $360.00 after beating expectations and and raising guidance.

Ferrari Stock Is on Track to Hit All-Time Highs — WSJ

Nov 3, 202321:31 GMT+2

RACE

+1.78%

By Hardika Singh

The company that makes some of the hottest cars in the world has a hot stock.

Ferrari shares recently rose 2.4% to $331 Friday, on course to set at a record high, after the Italian sports-car maker on Thursday reported earnings (www.wsj.com) that exceeded expectations.

The company raised its full-year guidance after profit jumped 45% and revenue grew 24% in the third quarter from a year ago, thanks to a better sales mix and higher demand for vehicle customization.

Ferrari shares are up 54% this year.

Quick update on CB rat raceAs you citizens can see we've found a mistake in our earlier analysis, we are apoligising for this. We think that during summer of 1998 Russian Federation stepped into fx trading big time and move cycles towards bigger and longer planning. So as you have guessed this is a game of sharade about who is planning longer and who is taking gaps. Thank you and see you later, have a good working week guests.

$RACE short term trading planI've included a weekly trade plan for RACE (Ferrari) with points to watch at the weekly close, need a close below yellow and green supports right now, this week should give a strong signal.

Once that happens we have to capture a 12% swing to low as that's a strong support area, where we will be looking for re entry short or long depending on the general market and index positioning.

Ferrari begins accepting crypto currency as means of paymentThis is huge for Ferrari and we are expecting a surge in price for the RACE Ferrari stock

Race Ferrari:Hitting the Brakes on a Volatile Day

Race Ferrari (NYSE) presents an enticing opportunity for investors looking to go long in the luxury automotive sector. Ferrari, known for its iconic brand and high-performance vehicles, has demonstrated resilience amid economic uncertainties.

One compelling reason to consider a long position is Ferrari's strong brand loyalty and demand for its premium cars, which has shown no signs of waning. Additionally, as the global economy recovers, luxury car sales tend to rebound strongly.

With a track record of steady growth and a commitment to sustainability, Ferrari is well-poised for future success. Its expansion into electric vehicles and continued focus on innovation ensures it remains at the forefront of the automotive industry.

Furthermore, technical analysis reveals positive signals, including moving averages and relative strength index (RSI), supporting a bullish outlook.

While no investment is without risks, Ferrari's unique market position and promising future prospects make it an attractive choice for those considering a long-term investment strategy in the automotive industry.

RACE 4d best level to buy/hold 100% gains 🔸Hello traders, today let's review4 daily price chart for RACE/Ferrari. Measured move

pullback in progress right now, however overall strong chart indicates further upside possible.

🔸Strong sequence of higher lows and higher highs and new higher lows

new higher low expected near 210/215 usd. currently pullback in progress so it's recommended

to wait until pullback is over before reloading. buy/hold setup for patient traders only.

🔸Recommended strategy bulls: expecting pullback based on measured move projection

set to extend further down towards 210/215 usd. Bulls should focus on buying low later

after the pullback is complete later in Q4 2023/Q1 2024. reload bulls near 210/215usd.

Based on measured move projection new high expected at 500 usd. 100% upside in this trade.

🎁Please hit the like button and

🎁Leave a comment to support our team!

RISK DISCLAIMER:

Trading Futures , Forex, CFDs and Stocks involves a risk of loss.

Please consider carefully if such trading is appropriate for you.

Past performance is not indicative of future results.

Always limit your leverage and use tight stop loss.