Bitcoin vs. Gold correlation with lagBTC vs Gold (Lag) + Correlation — multi-timeframe, publication notes

What it does

Plots Gold on the same chart as Bitcoin, with a configurable lead/lag.

Lets you choose how the series is displayed:

Gold shifted forward (+lag on chart) — shows gold ahead of BTC on the time axis (visual offset).

Gold aligned to BTC (gold lag) — standard alignment; gold is lagged for calculation and plotted in place.

BTC 200D Lag (BTC shifted forward) — visualizes BTC shifted forward (like popular “BTC 200D Lag” charts).

Computes Pearson correlations between BTC (no lag) and Gold (with lag) over multiple lookback windows equivalent to:

30d, 60d, 90d, 180d, 365d, 2y (730d), 3y (1095d), 5y (1825d).

Shows a table with the correlation values, automatically scaled to the current timeframe.

Why this is useful

A common macro claim is that BTC tends to follow Gold with a delay (e.g., ~200 trading days). This tool lets you:

Visually advance Gold (or BTC) to see that lead-lag relationship on the chart.

Quantify the relationship with rolling correlations.

Switch timeframes (D/W/M/…): everything automatically stays in sync.

Quick start

Open a BTC chart (any exchange).

Add the indicator.

Set Gold symbol (default TVC:GOLD; alternatives: OANDA:XAUUSD, COMEX:GC1!, etc.).

Choose Lag value and Lag unit (Days/Weeks/Months/Years/Bars).

Pick Visual Mode:

To mirror those “BTC 200D Lag” posts: choose “BTC 200D Lag (BTC shifted forward)” with 200 Days.

To view Gold 200D ahead of BTC: select “Gold shifted forward (+lag on chart)” with 200 Days.

Keep Rebase to 100 ON for an apples-to-apples visual scale. (You can move the study to the left price scale if needed.)

Inputs

Gold symbol: external series to pair with BTC.

Lag value: numeric value.

Lag unit: Days, Weeks, Months (≈30d), Years (≈365d), or direct Bars.

Visual mode:

Gold shifted forward (+lag on chart) → gold is offset to the right by the lag (visual only).

Gold aligned to BTC (gold lag) → standard plot (no visual offset); correlations still use lagged gold.

BTC 200D Lag (BTC shifted forward) → BTC is offset to the right by the lag (visual only).

Rebase to 100 (visual): rescales each series to 100 on its first valid bar for clearer comparison.

Show gold without lag (debug): optional reference line.

Show price tag for gold (lag): toggles the track price label.

Timeframe handling

The study uses the current chart timeframe for both BTC and Gold (timeframe.period).

Lag in time units (Days/Weeks/Months/Years) is internally converted to an integer number of bars of the active timeframe (using timeframe.in_seconds).

Example: on W (weekly), 200 days ≈ 29 bars.

On intraday timeframes, days are converted proportionally.

Correlation math

Correlation = ta.correlation(BTC, Gold_lagged, length_in_bars)

Lookback lengths are the bar-equivalents of 30/60/90/180/365/730/1095/1825 days in the active timeframe.

Important: correlations are computed on prices (not returns). If you prefer returns-based correlation (often more statistically robust), duplicate the script and replace price inputs with change(close) or ta.roc(close, 1).

Reading the table

Window: nominal day label (e.g., 30d, 1y, 5y).

Bars (TF): how many bars that window equals on the current timeframe.

Correlation: Pearson coefficient . Background tint shows intensity and sign.

Tips & caveats

Visual offsets (offset=) move series on screen only; they don’t affect the math. The math always uses BTC (no lag) × Gold (lagged).

With large lags on high timeframes, early bars will be na (normal). Scroll forward / reduce lag.

If your Gold feed doesn’t load, try an alternative symbol that your plan supports.

Rebase to 100 helps visibility when BTC ($100k) and Gold ($2k) share a scale.

Months/Years use 30/365-day approximations. For exact control, use Days or Bars.

Correlations on very short lengths or sparse data can be unstable; consider the longer windows for sturdier signals.

This is a visual/analytical tool, not a trading signal. Always apply independent risk management.

Suggested setups

Replicate “BTC 200D Lag” charts:

Visual Mode: BTC 200D Lag (BTC shifted forward)

Lag: 200 Days

Rebase: ON

Gold leads BTC (Gold ahead):

Visual Mode: Gold shifted forward (+lag on chart)

Lag: 200 Days

Rebase: ON

Compatibility: Pine v6, overlay study.

Best with: BTCUSD (any exchange) + a reliable Gold feed.

Author’s note: Lead-lag relationships are not stable over time; treat correlations as descriptive, not predictive.

Bitcoin (Cryptocurrency)

Adaptive Trend Following Suite [Alpha Extract]A sophisticated multi-filter trend analysis system that combines advanced noise reduction, adaptive moving averages, and intelligent market structure detection to deliver institutional-grade trend following signals. Utilizing cutting-edge mathematical algorithms and dynamic channel adaptation, this indicator provides crystal-clear directional guidance with real-time confidence scoring and market mode classification for professional trading execution.

🔶 Advanced Noise Reduction

Filter Eliminates market noise using sophisticated Gaussian filtering with configurable sigma values and period optimization. The system applies mathematical weight distribution across price data to ensure clean signal generation while preserving critical trend information, automatically adjusting filter strength based on volatility conditions.

advancedNoiseFilter(sourceData, filterLength, sigmaParam) =>

weightSum = 0.0

valueSum = 0.0

centerPoint = (filterLength - 1) / 2

for index = 0 to filterLength - 1

gaussianWeight = math.exp(-0.5 * math.pow((index - centerPoint) / sigmaParam, 2))

weightSum += gaussianWeight

valueSum += sourceData * gaussianWeight

valueSum / weightSum

🔶 Adaptive Moving Average Core Engine

Features revolutionary volatility-responsive averaging that automatically adjusts smoothing parameters based on real-time market conditions. The engine calculates adaptive power factors using logarithmic scaling and bandwidth optimization, ensuring optimal responsiveness during trending markets while maintaining stability during consolidation phases.

// Calculate adaptive parameters

adaptiveLength = (periodLength - 1) / 2

logFactor = math.max(math.log(math.sqrt(adaptiveLength)) / math.log(2) + 2, 0)

powerFactor = math.max(logFactor - 2, 0.5)

relativeVol = avgVolatility != 0 ? volatilityMeasure / avgVolatility : 0

adaptivePower = math.pow(relativeVol, powerFactor)

bandwidthFactor = math.sqrt(adaptiveLength) * logFactor

🔶 Intelligent Market Structure Analysis

Employs fractal dimension calculations to classify market conditions as trending or ranging with mathematical precision. The system analyzes price path complexity using normalized data arrays and geometric path length calculations, providing quantitative market mode identification with configurable threshold sensitivity.

🔶 Multi-Component Momentum Analysis

Integrates RSI and CCI oscillators with advanced Z-score normalization for statistical significance testing. Each momentum component receives independent analysis with customizable periods and significance levels, creating a robust consensus system that filters false signals while maintaining sensitivity to genuine momentum shifts.

// Z-score momentum analysis

rsiAverage = ta.sma(rsiComponent, zAnalysisPeriod)

rsiDeviation = ta.stdev(rsiComponent, zAnalysisPeriod)

rsiZScore = (rsiComponent - rsiAverage) / rsiDeviation

if math.abs(rsiZScore) > zSignificanceLevel

rsiMomentumSignal := rsiComponent > 50 ? 1 : rsiComponent < 50 ? -1 : rsiMomentumSignal

❓How It Works

🔶 Dynamic Channel Configuration

Calculates adaptive channel boundaries using three distinct methodologies: ATR-based volatility, Standard Deviation, and advanced Gaussian Deviation analysis. The system automatically adjusts channel multipliers based on market structure classification, applying tighter channels during trending conditions and wider boundaries during ranging markets for optimal signal accuracy.

dynamicChannelEngine(baselineData, channelLength, methodType) =>

switch methodType

"ATR" => ta.atr(channelLength)

"Standard Deviation" => ta.stdev(baselineData, channelLength)

"Gaussian Deviation" =>

weightArray = array.new_float()

totalWeight = 0.0

for i = 0 to channelLength - 1

gaussWeight = math.exp(-math.pow((i / channelLength) / 2, 2))

weightedVariance += math.pow(deviation, 2) * array.get(weightArray, i)

math.sqrt(weightedVariance / totalWeight)

🔶 Signal Processing Pipeline

Executes a sophisticated 10-step signal generation process including noise filtering, trend reference calculation, structure analysis, momentum component processing, channel boundary determination, trend direction assessment, consensus calculation, confidence scoring, and final signal generation with quality control validation.

🔶 Confidence Transformation System

Applies sigmoid transformation functions to raw confidence scores, providing 0-1 normalized confidence ratings with configurable threshold controls. The system uses steepness parameters and center point adjustments to fine-tune signal sensitivity while maintaining statistical robustness across different market conditions.

🔶 Enhanced Visual Presentation

Features dynamic color-coded trend lines with adaptive channel fills, enhanced candlestick visualization, and intelligent price-trend relationship mapping. The system provides real-time visual feedback through gradient fills and transparency adjustments that immediately communicate trend strength and direction changes.

🔶 Real-Time Information Dashboard

Displays critical trading metrics including market mode classification (Trending/Ranging), structure complexity values, confidence scores, and current signal status. The dashboard updates in real-time with color-coded indicators and numerical precision for instant market condition assessment.

🔶 Intelligent Alert System

Generates three distinct alert types: Bullish Signal alerts for uptrend confirmations, Bearish Signal alerts for downtrend confirmations, and Mode Change alerts for market structure transitions. Each alert includes detailed messaging and timestamp information for comprehensive trade management integration.

🔶 Performance Optimization

Utilizes efficient array management and conditional processing to maintain smooth operation across all timeframes. The system employs strategic variable caching, optimized loop structures, and intelligent update mechanisms to ensure consistent performance even during high-volatility market conditions.

This indicator delivers institutional-grade trend analysis through sophisticated mathematical modelling and multi-stage signal processing. By combining advanced noise reduction, adaptive averaging, intelligent structure analysis, and robust momentum confirmation with dynamic channel adaptation, it provides traders with unparalleled trend following precision. The comprehensive confidence scoring system and real-time market mode classification make it an essential tool for professional traders seeking consistent, high-probability trend following opportunities with mathematical certainty and visual clarity.

BTC Power Law Valuation BandsBTC Power Law Rainbow

A long-term valuation framework for Bitcoin based on Power Law growth — designed to help identify macro accumulation and distribution zones, aligned with long-term investor behavior.

🔍 What Is a Power Law?

A Power Law is a mathematical relationship where one quantity varies as a power of another. In this model:

Price ≈ a × (Time)^b

It captures the non-linear, exponentially slowing growth of Bitcoin over time. Rather than using linear or cyclical models, this approach aligns with how complex systems, such as networks or monetary adoption curves, often grow — rapidly at first, and then more slowly, but persistently.

🧠 Why Power Law for BTC?

Bitcoin:

Has finite supply and increasing adoption.

Operates as a monetary network , where Metcalfe’s Law and power laws naturally emerge.

Exhibits exponential growth over logarithmic time when viewed on a log-log chart .

This makes it uniquely well-suited for power law modeling.

🌈 How to Use the Valuation Bands

The central white line represents the modeled fair value according to the power law.

Colored bands represent deviations from the model in logarithmic space, acting as macro zones:

🔵 Lower Bands: Deep value / Accumulation zones.

🟡 Mid Bands: Fair value.

🔴 Upper Bands: Euphoria / Risk of macro tops.

📐 Smart Money Concepts (SMC) Alignment

Accumulation: Occurs when price consolidates near lower bands — often aligning with institutional positioning.

Markup: As price re-enters or ascends the bands, we often see breakout behavior and trend expansion.

Distribution: When price extends above upper bands, potential for exit liquidity creation and distribution events.

Reversion: Historically, price mean-reverts toward the model — rarely staying outside the bands for long.

This makes the model useful for:

Cycle timing

Long-term DCA strategy zones

Identifying value dislocations

Filtering short-term noise

⚠️ Disclaimer

This tool is for educational and informational purposes only . It is not financial advice. The power law model is a non-predictive, mathematical framework and does not guarantee future price movements .

Always use additional tools, risk management, and your own judgment before making trading or investment decisions.

Mutanabby_AI | ATR+ | Trend-Following StrategyThis document presents the Mutanabby_AI | ATR+ Pine Script strategy, a systematic approach designed for trend identification and risk-managed position entry in financial markets. The strategy is engineered for long-only positions and integrates volatility-adjusted components to enhance signal robustness and trade management.

Strategic Design and Methodological Basis

The Mutanabby_AI | ATR+ strategy is constructed upon a foundation of established technical analysis principles, with a focus on objective signal generation and realistic trade execution.

Heikin Ashi for Trend Filtering: The core price data is processed via Heikin Ashi (HA) methodology to mitigate transient market noise and accentuate underlying trend direction. The script offers three distinct HA calculation modes, allowing for comparative analysis and validation:

Manual Calculation: Provides a transparent and deterministic computation of HA values.

ticker.heikinashi(): Utilizes TradingView's built-in function, employing confirmed historical bars to prevent repainting artifacts.

Regular Candles: Allows for direct comparison with standard OHLC price action.

This multi-methodological approach to trend smoothing is critical for robust signal generation.

Adaptive ATR Trailing Stop: A key component is the Average True Range (ATR)-based trailing stop. ATR serves as a dynamic measure of market volatility. The strategy incorporates user-defined parameters (

Key Value and ATR Period) to calibrate the sensitivity of this trailing stop, enabling adaptation to varying market volatility regimes. This mechanism is designed to provide a dynamic exit point, preserving capital and locking in gains as a trend progresses.

EMA Crossover for Signal Generation: Entry and exit signals are derived from the interaction between the Heikin Ashi derived price source and an Exponential Moving Average (EMA). A crossover event between these two components is utilized to objectively identify shifts in momentum, signaling potential long entry or exit points.

Rigorous Stop Loss Implementation: A critical feature for risk mitigation, the strategy includes an optional stop loss. This stop loss can be configured as a percentage or fixed point deviation from the entry price. Importantly, stop loss execution is based on real market prices, not the synthetic Heikin Ashi values. This design choice ensures that risk management is grounded in actual market liquidity and price levels, providing a more accurate representation of potential drawdowns during backtesting and live operation.

Backtesting Protocol: The strategy is configured for realistic backtesting, employing fill_orders_on_standard_ohlc=true to simulate order execution at standard OHLC prices. A configurable Date Filter is included to define specific historical periods for performance evaluation.

Data Visualization and Metrics: The script provides on-chart visual overlays for buy/sell signals, the ATR trailing stop, and the stop loss level. An integrated information table displays real-time strategy parameters, current position status, trend direction, and key price levels, facilitating immediate quantitative assessment.

Applicability

The Mutanabby_AI | ATR+ strategy is particularly suited for:

Cryptocurrency Markets: The inherent volatility of assets such as #Bitcoin and #Ethereum makes the ATR-based trailing stop a relevant tool for dynamic risk management.

Systematic Trend Following: Individuals employing systematic methodologies for trend capture will find the objective signal generation and rule-based execution aligned with their approach.

Pine Script Developers and Quants: The transparent code structure and emphasis on realistic backtesting provide a valuable framework for further analysis, modification, and integration into broader quantitative models.

Automated Trading Systems: The clear, deterministic entry and exit conditions facilitate integration into automated trading environments.

Implementation and Evaluation

To evaluate the Mutanabby_AI | ATR+ strategy, apply the script to your chosen chart on TradingView. Adjust the input parameters (Key Value, ATR Period, Heikin Ashi Method, Stop Loss Settings) to observe performance across various asset classes and timeframes. Comprehensive backtesting is recommended to assess the strategy's historical performance characteristics, including profitability, drawdown, and risk-adjusted returns.

I'd love to hear your thoughts, feedback, and any optimizations you discover! Drop a comment below, give it a like if you find it useful, and share your results.

Adaptive MVRV & RSI Strategy V6 (Dynamic Thresholds)Strategy Explanation

This is an advanced Dollar-Cost Averaging (DCA) strategy for Bitcoin that aims to adapt to long-term market cycles and changing volatility. Instead of relying on fixed buy/sell signals, it uses a dynamic, weighted approach based on a combination of on-chain data and classic momentum.

Core Components:

Dual-Indicator Signal: The strategy combines two powerful indicators for a more robust signal:

MVRV Ratio: An on-chain metric to identify when Bitcoin is fundamentally over or undervalued relative to its historical cost basis.

Weekly RSI: A classic momentum indicator to gauge long-term market strength and identify overbought/oversold conditions.

Dynamic, Self-Adjusting Thresholds: The core innovation of this strategy is that it avoids fixed thresholds (e.g., "sell when RSI is 70"). Instead, the buy and sell zones are dynamically calculated based on a long-term (2-year) moving average and standard deviation of each indicator. This allows the strategy to automatically adapt to Bitcoin's decreasing volatility and changing market structure over time.

Weighted DCA (Scaling In & Out): The strategy doesn't just buy or sell a fixed amount. The size of its trades is scaled based on conviction:

Buying: As the MVRV and RSI fall deeper into their "undervalued" zones, the percentage of available cash used for each purchase increases.

Selling: As the indicators rise further into "overvalued" territory, the percentage of the current position sold also increases.

This creates an adaptive system that systematically accumulates during periods of fear and distributes during periods of euphoria, with the intensity of its actions directly tied to the extremity of market conditions.

Pi Cycle Top Indicator - mychaelgoPlots the original Pi Cycle Top moving averages and marks bars where the 111DMA is rising and crosses above the 350DMA×2, often coinciding with Bitcoin cycle peaks. Includes a label with the signal price.

Bitcoin Expectile Model [LuxAlgo]The Bitcoin Expectile Model is a novel approach to forecasting Bitcoin, inspired by the popular Bitcoin Quantile Model by PlanC. By fitting multiple Expectile regressions to the price, we highlight zones of corrections or accumulations throughout the Bitcoin price evolution.

While we strongly recommend using this model with the Bitcoin All Time History Index INDEX:BTCUSD on the 3 days or weekly timeframe using a logarithmic scale, this model can be applied to any asset using the daily timeframe or superior.

Please note that here on TradingView, this model was solely designed to be used on the Bitcoin 1W chart, however, it can be experimented on other assets or timeframes if of interest.

🔶 USAGE

The Bitcoin Expectile Model can be applied similarly to models used for Bitcoin, highlighting lower areas of possible accumulation (support) and higher areas that allow for the anticipation of potential corrections (resistance).

By default, this model fits 7 individual Expectiles Log-Log Regressions to the price, each with their respective expectile ( tau ) values (here multiplied by 100 for the user's convenience). Higher tau values will return a fit closer to the higher highs made by the price of the asset, while lower ones will return fits closer to the lower prices observed over time.

Each zone is color-coded and has a specific interpretation. The green zone is a buy zone for long-term investing, purple is an anomaly zone for market bottoms that over-extend, while red is considered the distribution zone.

The fits can be extrapolated, helping to chart a course for the possible evolution of Bitcoin prices. Users can select the end of the forecast as a date using the "Forecast End" setting.

While the model is made for Bitcoin using a log scale, other assets showing a tendency to have a trend evolving in a single direction can be used. See the chart above on QQQ weekly using a linear scale as an example.

The Start Date can also allow fitting the model more locally, rather than over a large range of prices. This can be useful to identify potential shorter-term support/resistance areas.

🔶 DETAILS

🔹 On Quantile and Expectile Regressions

Quantile and Expectile regressions are similar; both return extremities that can be used to locate and predict prices where tops/bottoms could be more likely to occur.

The main difference lies in what we are trying to minimize, which, for Quantile regression, is commonly known as Quantile loss (or pinball loss), and for Expectile regression, simply Expectile loss.

You may refer to external material to go more in-depth about these loss functions; however, while they are similar and involve weighting specific prices more than others relative to our parameter tau, Quantile regression involves minimizing a weighted mean absolute error, while Expectile regression minimizes a weighted squared error.

The squared error here allows us to compute Expectile regression more easily compared to Quantile regression, using Iteratively reweighted least squares. For Quantile regression, a more elaborate method is needed.

In terms of comparison, Quantile regression is more robust, and easier to interpret, with quantiles being related to specific probabilities involving the underlying cumulative distribution function of the dataset; on the other expectiles are harder to interpret.

🔹 Trimming & Alterations

It is common to observe certain models ignoring very early Bitcoin price ranges. By default, we start our fit at the date 2010-07-16 to align with existing models.

By default, the model uses the number of time units (days, weeks...etc) elapsed since the beginning of history + 1 (to avoid NaN with log) as independent variable, however the Bitcoin All Time History Index INDEX:BTCUSD do not include the genesis block, as such users can correct for this by enabling the "Correct for Genesis block" setting, which will add the amount of missed bars from the Genesis block to the start oh the chart history.

🔶 SETTINGS

Start Date: Starting interval of the dataset used for the fit.

Correct for genesis block: When enabled, offset the X axis by the number of bars between the Bitcoin genesis block time and the chart starting time.

🔹 Expectiles

Toggle: Enable fit for the specified expectile. Disabling one fit will make the script faster to compute.

Expectile: Expectile (tau) value multiplied by 100 used for the fit. Higher values will produce fits that are located near price tops.

🔹 Forecast

Forecast End: Time at which the forecast stops.

🔹 Model Fit

Iterations Number: Number of iterations performed during the reweighted least squares process, with lower values leading to less accurate fits, while higher values will take more time to compute.

Mutanabby_AI | Algo Pro Strategy# Mutanabby_AI | Algo Pro Strategy: Advanced Candlestick Pattern Trading System

## Strategy Overview

The Mutanabby_AI Algo Pro Strategy represents a systematic approach to automated trading based on advanced candlestick pattern recognition and multi-layered technical filtering. This strategy transforms traditional engulfing pattern analysis into a comprehensive trading system with sophisticated risk management and flexible position sizing capabilities.

The strategy operates on a long-only basis, entering positions when bullish engulfing patterns meet specific technical criteria and exiting when bearish engulfing patterns indicate potential trend reversals. The system incorporates multiple confirmation layers to enhance signal reliability while providing comprehensive customization options for different trading approaches and risk management preferences.

## Core Algorithm Architecture

The strategy foundation relies on bullish and bearish engulfing candlestick pattern recognition enhanced through technical analysis filtering mechanisms. Entry signals require simultaneous satisfaction of four distinct criteria: confirmed bullish engulfing pattern formation, candle stability analysis indicating decisive price action, RSI momentum confirmation below specified thresholds, and price decline verification over adjustable lookback periods.

The candle stability index measures the ratio between candlestick body size and total range including wicks, ensuring only well-formed patterns with clear directional conviction generate trading signals. This filtering mechanism eliminates indecisive market conditions where pattern reliability diminishes significantly.

RSI integration provides momentum confirmation by requiring oversold conditions before entry signal generation, ensuring alignment between pattern formation and underlying momentum characteristics. The RSI threshold remains fully adjustable to accommodate different market conditions and volatility environments.

Price decline verification examines whether current prices have decreased over a specified period, confirming that bullish engulfing patterns occur after meaningful downward movement rather than during sideways consolidation phases. This requirement enhances the probability of successful reversal pattern completion.

## Advanced Position Management System

The strategy incorporates dual position sizing methodologies to accommodate different account sizes and risk management approaches. Percentage-based position sizing calculates trade quantities as equity percentages, enabling consistent risk exposure across varying account balances and market conditions. This approach proves particularly valuable for systematic trading approaches and portfolio management applications.

Fixed quantity sizing provides precise control over trade sizes independent of account equity fluctuations, offering predictable position management for specific trading strategies or when implementing precise risk allocation models. The system enables seamless switching between sizing methods through simple configuration adjustments.

Position quantity calculations integrate seamlessly with TradingView's strategy testing framework, ensuring accurate backtesting results and realistic performance evaluation across different market conditions and time periods. The implementation maintains consistency between historical testing and live trading applications.

## Comprehensive Risk Management Framework

The strategy features dual stop loss methodologies addressing different risk management philosophies and market analysis approaches. Entry price-based stop losses calculate stop levels as fixed percentages below entry prices, providing predictable risk exposure and consistent risk-reward ratio maintenance across all trades.

The percentage-based stop loss system enables precise risk control by limiting maximum loss per trade to predetermined levels regardless of market volatility or entry timing. This approach proves essential for systematic trading strategies requiring consistent risk parameters and capital preservation during adverse market conditions.

Lowest low-based stop losses identify recent price support levels by analyzing minimum prices over adjustable lookback periods, placing stops below these technical levels with additional buffer percentages. This methodology aligns stop placement with market structure rather than arbitrary percentage calculations, potentially improving stop loss effectiveness during normal market fluctuations.

The lookback period adjustment enables optimization for different timeframes and market characteristics, with shorter periods providing tighter stops for active trading and longer periods offering broader stops suitable for position trading approaches. Buffer percentage additions ensure stops remain below obvious support levels where other market participants might place similar orders.

## Visual Customization and Interface Design

The strategy provides comprehensive visual customization through eight predefined color schemes designed for different chart backgrounds and personal preferences. Color scheme options include Classic bright green and red combinations, Ocean themes featuring blue and orange contrasts, Sunset combinations using gold and crimson, and Neon schemes providing high visibility through bright color selections.

Professional color schemes such as Forest, Royal, and Fire themes offer sophisticated alternatives suitable for business presentations and professional trading environments. The Custom color scheme enables precise color selection through individual color picker controls, maintaining maximum flexibility for specific visual requirements.

Label styling options accommodate different chart analysis preferences through text bubble, triangle, and arrow display formats. Size adjustments range from tiny through huge settings, ensuring appropriate visual scaling across different screen resolutions and chart configurations. Text color customization maintains readability across various chart themes and background selections.

## Signal Quality Enhancement Features

The strategy incorporates signal filtering mechanisms designed to eliminate repetitive signal generation during choppy market conditions. The disable repeating signals option prevents consecutive identical signals until opposing conditions occur, reducing overtrading during consolidation phases and improving overall signal quality.

Signal confirmation requirements ensure all technical criteria align before trade execution, reducing false signal occurrence while maintaining reasonable trading frequency for active strategies. The multi-layered approach balances signal quality against opportunity frequency through adjustable parameter optimization.

Entry and exit visualization provides clear trade identification through customizable labels positioned at relevant price levels. Stop loss visualization displays active risk levels through colored line plots, ensuring complete transparency regarding current risk management parameters during live trading operations.

## Implementation Guidelines and Optimization

The strategy performs effectively across multiple timeframes with optimal results typically occurring on intermediate timeframes ranging from fifteen minutes through four hours. Higher timeframes provide more reliable pattern formation and reduced false signal occurrence, while lower timeframes increase trading frequency at the expense of some signal reliability.

Parameter optimization should focus on RSI threshold adjustments based on market volatility characteristics and candlestick pattern timeframe analysis. Higher RSI thresholds generate fewer but potentially higher quality signals, while lower thresholds increase signal frequency with corresponding reliability considerations.

Stop loss method selection depends on trading style preferences and market analysis philosophy. Entry price-based stops suit systematic approaches requiring consistent risk parameters, while lowest low-based stops align with technical analysis methodologies emphasizing market structure recognition.

## Performance Considerations and Risk Disclosure

The strategy operates exclusively on long positions, making it unsuitable for bear market conditions or extended downtrend periods. Users should consider market environment analysis and broader trend assessment before implementing the strategy during adverse market conditions.

Candlestick pattern reliability varies significantly across different market conditions, with higher reliability typically occurring during trending markets compared to ranging or volatile conditions. Strategy performance may deteriorate during periods of reduced pattern effectiveness or increased market noise.

Risk management through stop loss implementation remains essential for capital preservation during adverse market movements. The strategy does not guarantee profitable outcomes and requires proper position sizing and risk management to prevent significant capital loss during unfavorable trading periods.

## Technical Specifications

The strategy utilizes standard TradingView Pine Script functions ensuring compatibility across all supported instruments and timeframes. Default configuration employs 14-period RSI calculations, adjustable candle stability thresholds, and customizable price decline verification periods optimized for general market conditions.

Initial capital settings default to $10,000 with percentage-based equity allocation, though users can adjust these parameters based on account size and risk tolerance requirements. The strategy maintains detailed trade logs and performance metrics through TradingView's integrated backtesting framework.

Alert integration enables real-time notification of entry and exit signals, stop loss executions, and other significant trading events. The comprehensive alert system supports automated trading applications and manual trade management approaches through detailed signal information provision.

## Conclusion

The Mutanabby_AI Algo Pro Strategy provides a systematic framework for candlestick pattern trading with comprehensive risk management and position sizing flexibility. The strategy's strength lies in its multi-layered confirmation approach and sophisticated customization options, enabling adaptation to various trading styles and market conditions.

Successful implementation requires understanding of candlestick pattern analysis principles and appropriate parameter optimization for specific market characteristics. The strategy serves traders seeking automated execution of proven technical analysis techniques while maintaining comprehensive control over risk management and position sizing methodologies.

Mutanabby_AI __ OSC+ST+SQZMOMMutanabby_AI OSC+ST+SQZMOM: Multi-Component Trading Analysis Tool

Overview

The Mutanabby_AI OSC+ST+SQZMOM indicator combines three proven technical analysis components into a unified trading system, providing comprehensive market analysis through integrated oscillator signals, trend identification, and volatility assessment.

Core Components

Wave Trend Oscillator (OSC): Identifies overbought and oversold market conditions using exponential moving average calculations. Key threshold levels include overbought zones at 60 and 53, with oversold areas marked at -60 and -53. Crossover signals between the two oscillator lines generate entry opportunities, displayed as colored circles on the chart for easy identification.

Supertrend Indicator (ST): Determines overall market direction using Average True Range calculations with a 2.5 factor and 10-period ATR configuration. Green lines indicate confirmed uptrends while red lines signal downtrend conditions. The indicator automatically adapts to market volatility changes, providing reliable trend identification across different market environments.

Squeeze Momentum (SQZMOM): Compares Bollinger Bands with Keltner Channels to identify consolidation periods and potential breakout scenarios. Black squares indicate squeeze conditions representing low volatility periods, green triangles signal confirmed upward breakouts, and red triangles mark downward breakout confirmations.

Signal Generation Logic

Long Entry Conditions:

Green triangles from Squeeze Momentum component

Supertrend line transitioning to green

Bullish crossovers in Wave Trend Oscillator from oversold territory

Short Entry Conditions:

Red triangles from Squeeze Momentum component

Supertrend line transitioning to red

Bearish crossovers in Wave Trend Oscillator from overbought territory

Automated Risk Management

The indicator incorporates comprehensive risk management through ATR-based calculations. Stop losses are automatically positioned at 3x ATR distance from entry points, while three progressive take profit targets are established at 1x, 2x, and 3x ATR multiples respectively. All risk management levels are clearly displayed on the chart using colored lines and informative labels.

When trend direction changes, the system automatically clears previous risk levels and generates new calculations, ensuring all risk parameters remain current and relevant to existing market conditions.

Alert and Notification System

Comprehensive alert framework includes trend change notifications with complete trade setup details, squeeze release alerts for breakout opportunity identification, and trend weakness warnings for active position management. Alert messages contain specific trading pair information, timeframe specifications, and all relevant entry and exit level data.

Implementation Guidelines

Timeframe Selection: Higher timeframes including 4-hour and daily charts provide the most reliable signals for position trading strategies. One-hour charts demonstrate good performance for day trading applications, while 15-30 minute timeframes enable scalping approaches with enhanced risk management requirements.

Risk Management Integration: Limit individual trade risk to 1-2% of total capital using the automatically calculated stop loss levels for precise position sizing. Implement systematic profit-taking at each target level while adjusting stop loss positions to protect accumulated gains.

Market Volatility Adaptation: The indicator's ATR-based calculations automatically adjust to changing market volatility conditions. During high volatility periods, risk management levels appropriately widen, while low volatility conditions result in tighter risk parameters.

Optimization Techniques

Combine indicator signals with fundamental support and resistance level analysis for enhanced signal validation. Monitor volume patterns to confirm breakout strength, particularly when Squeeze Momentum signals develop. Maintain awareness of scheduled economic events that may influence market behavior independent of technical indicator signals.

The multi-component design provides internal signal confirmation through multiple alignment requirements, significantly reducing false signal occurrence while maintaining reasonable trade frequency for active trading strategies.

Technical Specifications

The Wave Trend Oscillator utilizes customizable channel length (default 10) and average length (default 21) parameters for optimal market sensitivity. Supertrend calculations employ ATR period of 10 with factor multiplier of 2.5 for balanced signal quality. Squeeze Momentum analysis uses Bollinger Band length of 20 periods with 2.0 multiplication factor, combined with Keltner Channel length of 20 periods and 1.5 multiplication factor.

Conclusion

The Mutanabby_AI OSC+ST+SQZMOM indicator provides a systematic approach to technical market analysis through the integration of proven oscillator, trend, and momentum components. Success requires thorough understanding of each element's functionality and disciplined implementation of proper risk management principles.

Practice with demo trading accounts before live implementation to develop familiarity with signal interpretation and trade management procedures. The indicator's systematic approach effectively reduces emotional decision-making while providing clear, objective guidelines for trade entry, management, and exit strategies across various market conditions.

On-Chain Signals [LuxAlgo]The On-Chain Signals indicator uses fundamental blockchain metrics to provide traders with an objective technical view of their favorite cryptocurrencies.

It uses IntoTheBlock datasets integrated within TradingView to generate four key signals: Net Network Growth, In the Money, Concentration, and Large Transactions.

Together, these four signals provide traders with an overall directional bias of the market. All of the data can be visualized as a gauge, table, historical plot, or average.

🔶 USAGE

The main goal of this tool is to provide an overall directional bias based on four blockchain signals, each with three possible biases: bearish, neutral, or bullish. The thresholds for each signal bias can be adjusted on the settings panel.

These signals are based on IntoTheBlock's On-Chain Signals.

Net network growth: Change in the total number of addresses over the last seven periods; i.e., how many new addresses are being created.

In the Money: Change in the seven-period moving average of the total supply in the money. This shows how many addresses are profitable.

Concentration: Change in the aggregate addresses of whales and investors from the previous period. These are addresses holding at least 0.1% of the supply. This shows how many addresses are in the hands of a few.

Large Transactions: Changes in the number of transactions over $100,000. This metric tracks convergence or divergence from the 21- and 30-day EMAs and indicates the momentum of large transactions.

All of these signals together form the blockchain's overall directional bias.

Bearish: The number of bearish individual signals is greater than the number of bullish individual signals.

Neutral: The number of bearish individual signals is equal to the number of bullish individual signals.

Bullish: The number of bullish individual signals is greater than the number of bearish individual signals.

If the overall directional bias is bullish, we can expect the price of the observed cryptocurrency to increase. If the bias is bearish, we can expect the price to decrease. If the signal is neutral, the price may be more likely to stay the same.

Traders should be aware of two things. First, the signals provide optimal results when the chart is set to the daily timeframe. Second, the tool uses IntoTheBlock data, which is available on TradingView. Therefore, some cryptocurrencies may not be available.

🔹 Display Mode

Traders have three different display modes at their disposal. These modes can be easily selected from the settings panel. The gauge is set by default.

🔹 Gauge

The gauge will appear in the center of the visible space. Traders can adjust its size using the Scale parameter in the Settings panel. They can also give it a curved effect.

The number of bars displayed directly affects the gauge's resolution: More bars result in better resolution.

The chart above shows the effect that different scale configurations have on the gauge.

🔹 Historical Data

The chart above shows the historical data for each of the four signals.

Traders can use this mode to adjust the thresholds for each signal on the settings panel to fit the behavior of each cryptocurrency. They can also analyze how each metric impacts price behavior over time.

🔹 Average

This display mode provides an easy way to see the overall bias of past prices in order to analyze price behavior in relation to the underlying blockchain's directional bias.

The average is calculated by taking the values of the overall bias as -1 for bearish, 0 for neutral, and +1 for bullish, and then applying a triangular moving average over 20 periods by default. Simple and exponential moving averages are available, and traders can select the period length from the settings panel.

🔶 DETAILS

The four signals are based on IntoTheBlock's On-Chain Signals. We gather the data, manipulate it, and build the signals depending on each threshold.

Net network growth

float netNetworkGrowthData = customData('_TOTALADDRESSES')

float netNetworkGrowth = 100*(netNetworkGrowthData /netNetworkGrowthData - 1)

In the Money

float inTheMoneyData = customData('_INOUTMONEYIN')

float averageBalance = customData('_AVGBALANCE')

float inTheMoneyBalance = inTheMoneyData*averageBalance

float sma = ta.sma(inTheMoneyBalance,7)

float inTheMoney = ta.roc(sma,1)

Concentration

float whalesData = customData('_WHALESPERCENTAGE')

float inverstorsData = customData('_INVESTORSPERCENTAGE')

float bigHands = whalesData+inverstorsData

float concentration = ta.change(bigHands )*100

Large Transactions

float largeTransacionsData = customData('_LARGETXCOUNT')

float largeTX21 = ta.ema(largeTransacionsData,21)

float largeTX30 = ta.ema(largeTransacionsData,30)

float largeTransacions = ((largeTX21 - largeTX30)/largeTX30)*100

🔶 SETTINGS

Display mode: Select between gauge, historical data and average.

Average: Select a smoothing method and length period.

🔹 Thresholds

Net Network Growth : Bullish and bearish thresholds for this signal.

In The Money : Bullish and bearish thresholds for this signal.

Concentration : Bullish and bearish thresholds for this signal.

Transactions : Bullish and bearish thresholds for this signal.

🔹 Dashboard

Dashboard : Enable/disable dashboard display

Position : Select dashboard location

Size : Select dashboard size

🔹 Gauge

Scale : Select the size of the gauge

Curved : Enable/disable curved mode

Select Gauge colors for bearish, neutral and bullish bias

🔹 Style

Net Network Growth : Enable/disable historical plot and choose color

In The Money : Enable/disable historical plot and choose color

Concentration : Enable/disable historical plot and choose color

Large Transacions : Enable/disable historical plot and choose color

Sat Stacking Strategies Simulation (SSSS)Sat Stacking Strategies Simulation (SSSS)

This indicator simulates and compares different Bitcoin stacking strategies over time, allowing you to visualize performance, cost basis, and stacking behavior directly on your chart.

Core Features:

Three Stacking Strategies

• Trend-Based – Stack only when price is above/below a long-term SMA.

• Stack the Dip – Buy during sharp pullbacks or oversold conditions.

• Price Zone – Stack only in “cheap”, “fair”, or “expensive” zones based on a simulated Short-Term Holder (STH) cost basis.

Always Stack Benchmark

Compare your chosen strategy against a simple “Always Stack” approach for a real-world DCA reference.

Performance Metrics Table

Track:

• Total Fiat Added

• Total BTC Accumulated

• Current Value

• Average Cost per BTC

• PnL %

• CAGR

• Sharpe Ratio & Stdev

• Stack Events & Time Underwater

Advanced Options

• Simulate cash-secured puts on unused fiat.

• Simulate covered calls on BTC holdings.

• Roll over unused stacking amounts for future buys.

This tool is designed for Bitcoiners, stackers, and DCA enthusiasts who want to backtest and visualize their stacking plan—whether you keep it simple or go full quant.

Sometimes the best alpha is just showing up every week with your wallet open… and occasionally wearing a helmet. 🪖💰

Trend Strength Index [Alpha Extract]The Trend Strength Index leverages Volume Weighted Moving Average (VWMA) and Average True Range (ATR) to quantify trend intensity in cryptocurrency markets, particularly Bitcoin. The combination of VWMA and ATR is particularly powerful because VWMA provides a more accurate representation of the market's true average price by weighting periods of higher trading volume more heavily—capturing genuine momentum driven by increased participation rather than treating all price action equally, which is crucial in volatile assets like Bitcoin where volume spikes often signal institutional interest or market shifts.

Meanwhile, ATR normalizes this measurement for volatility, ensuring that trend strength readings remain comparable across different market conditions; without ATR's adjustment, raw price deviations from the mean could appear artificially inflated during high-volatility periods (like during news events or liquidations) or understated in low-volatility sideways markets, leading to misleading signals. Together, they create a volatility-adjusted, volume-sensitive metric that reliably distinguishes between meaningful trend developments and noise.

This indicator measures the normalized distance between price and its volume-weighted mean, providing a clear visualization of trend strength while accounting for market volatility. It helps traders identify periods of strong directional movement versus consolidation, with color-coded gradients for intuitive interpretation.

🔶 CALCULATION

The indicator processes price data through these analytical stages:

Volume Weighted Moving Average: Computes a smoothed average weighted by trading volume

Volatility Normalization: Uses ATR to account for market volatility

Distance Measurement: Calculates absolute deviation between current price and VWMA

Strength Normalization: Divides price deviation by ATR for a volatility-adjusted metric

Formula:

VWMA = Volume-Weighted Moving Average of Close over specified length

ATR = Average True Range over specified length

Price Distance = |Close - VWMA|

Trend Strength = Price Distance / ATR

🔶 DETAILS Visual Features:

VWMA Line: Blue line overlay on the price chart representing the volume-weighted mean

Trend Strength Area: Histogram-style area plot with dynamic color gradient (red for weak trends, transitioning through orange and yellow to green for strong trends)

Threshold Line: Horizontal red line at the customizable Trend Enter level

Background Highlight: Subtle green background when trend strength exceeds the enter threshold for strong trend visualization

Alert System: Triggers notifications for strong trend detection

Interpretation:

0-Weak (Red): Minimal trend strength, potential consolidation or ranging market

Mid-Range (Orange/Yellow): Building momentum, watch for breakout potential

At/Above Enter Threshold (Green): Strong trend conditions, potential for continued directional moves

Threshold Crossing: Trend strength crossing above the enter level signals increasing conviction in the current direction

Color Transitions: Gradual shifts from warm (red/orange) to cool (green) tones indicate strengthening trends

🔶 EXAMPLES

Strong Trend Entry: When trend strength crosses above the enter threshold (e.g., 1.2), it identifies the onset of a powerful move where price deviates significantly from the mean.

Example: During a rally, trend strength rising from yellow (around 1.0) to green (1.2+) often precedes sustained upward momentum, providing entry opportunities for trend followers.

Consolidation Detection: Low trend strength values in red shades (below 0.5) highlight periods of low volatility and mean reversion potential.

Example: After a sharp sell-off, persistent red values signal a likely sideways phase, allowing traders to avoid whipsaws and wait for orange/yellow transitions as a precursor to recovery.

Volatility-Adjusted Pullbacks: In volatile markets, the ATR component ensures trend strength remains accurate; a dip back to yellow from green during minor corrections can indicate healthy pullbacks within a strong trend.

Example: Trend strength briefly falling to yellow levels (e.g., 0.8-1.1) after hitting green provides profit-taking signals without invalidating the overall bullish bias if the VWMA holds as support.

Threshold Alert Integration: The alert condition combines strength value with the enter threshold for timely notifications.

Example: Receiving a "Strong Trend Detected" alert when the area plot turns green helps confirm Bitcoin's breakout from consolidation, aligning with increased volume for higher-probability trades.

🔶 SETTINGS

Customization Options:

Lengths: VWMA length (default 14), ATR length (default 14)

Thresholds: Trend enter (default 1.2, step 0.1), trend exit (default 1.15, for potential future signal enhancements)

Visuals: Automatic color scaling with red at 0, transitioning to green at/above enter threshold

Alert Conditions: Strong trend detection (when strength > enter)

The Trend Strength Index equips traders with a robust, easy-to-interpret tool for gauging trend intensity in volatile markets like Bitcoin. By normalizing price deviations against volatility, it delivers reliable signals for identifying high-momentum opportunities while the gradient coloring and alerts facilitate quick assessments in both trending and choppy conditions.

DAX Inducere Simplă v1.3 – Confirmare InducereDAX Inducere Simplă v1.3 – Confirmare Inducere ,signals before fvg mss and displacement

Market to NAV Premium Arbitrage Alpha IndicatorBitcoin treasury companies such as Microstrategy are known for trading at significant premiums. but how big exactly is the premium? And how can we measure it in real time?

I developed this quantitative tool to identify statistical mispricings between market capitalization and net asset value (NAV), specifically designed for arbitrage strategies and alpha generation in Bitcoin-holding companies, such as MicroStrategy or Sharplink Gaming, or SPACs used primarily to hold cryptocurrencies, Bitcoin ETFs, and other NAV-based instruments. It can probably also be used in certain spin-offs.

KEY FEATURES:

✅ Real-time Premium/Discount Calculation

• Automatically retrieves market cap data from TradingView

• Calculates precise NAV based on underlying asset holdings (for example Bitcoin)

• Formula: (Market Cap - NAV) / NAV × 100

✅ Statistical Analysis

• Historical percentile rankings (customizable lookback period)

• Standard deviation bands (2σ) for extreme value detection (close to these values might be seen as interesting points to short or go long)

• Smoothing period to reduce noise

✅ Multi-Source Market Cap Detection

• You can add the ticker of the NAV asset, but if necessary, you can also put it manually. Priority system: TradingView data → Calculated → Manual override

✅ Advanced NAV Modeling

• Basic NAV: Asset holdings + cash.

• Adjusted NAV: Includes software business value, debt, preferred shares. If the company has a lot of this kind of intrinsic value, put it in the "cash" field

• Support for any underlying asset (BTC, ETH, etc.)

TRADING APPLICATIONS:

🎯 Pairs Trading Signals

• Long/Short opportunities when premium reaches statistical extremes

• Mean reversion strategies based on historical ranges

• Risk-adjusted position sizing using percentile ranks

🎯 Arbitrage Detection

• Identifies when market pricing significantly deviates from fair value

• Quantifies the magnitude of mispricing for profit potential

• Historical context for timing entry/exit points

CONFIGURATION OPTIONS:

• Underlying Asset: Any symbol (default: COINBASE:BTCUSD) NEEDS MANUAL INPUT

• Asset Quantity: Precise holdings amount (for example, how much BTC does the company currently hold). NEEDS MANUAL INPUT

• Cash Holdings: Additional liquid assets. NEEDS MANUAL INPUT

• Market Cap Mode: Auto-detect, calculated, or manual

• Advanced Adjustments: Business value, debt, preferred shares

• Display Settings: Lookback period, smoothing, custom colors

IT CAN BE USED BY:

• Quantitative traders focused on statistical arbitrage

• Institutional investors monitoring NAV-based instruments

• Bitcoin ETF and MSTR traders seeking alpha generation

• Risk managers tracking premium/discount exposures

• Academic researchers studying market efficiency (as you can see, markets are not efficient 😉)

Ultimate Market Structure [Alpha Extract]Ultimate Market Structure

A comprehensive market structure analysis tool that combines advanced swing point detection, imbalance zone identification, and intelligent break analysis to identify high-probability trading opportunities.Utilizing a sophisticated trend scoring system, this indicator classifies market conditions and provides clear signals for structure breaks, directional changes, and fair value gap detection with institutional-grade precision.

🔶 Advanced Swing Point Detection

Identifies pivot highs and lows using configurable lookback periods with optional close-based analysis for cleaner signals. The system automatically labels swing points as Higher Highs (HH), Lower Highs (LH), Higher Lows (HL), and Lower Lows (LL) while providing advanced classifications including "rising_high", "falling_high", "rising_low", "falling_low", "peak_high", and "valley_low" for nuanced market analysis.

swingHighPrice = useClosesForStructure ? ta.pivothigh(close, swingLength, swingLength) : ta.pivothigh(high, swingLength, swingLength)

swingLowPrice = useClosesForStructure ? ta.pivotlow(close, swingLength, swingLength) : ta.pivotlow(low, swingLength, swingLength)

classification = classifyStructurePoint(structureHighPrice, upperStructure, true)

significance = calculateSignificance(structureHighPrice, upperStructure, true)

🔶 Significance Scoring System

Each structure point receives a significance level on a 1-5 scale based on its distance from previous points, helping prioritize the most important levels. This intelligent scoring system ensures traders focus on the most meaningful structure breaks while filtering out minor noise.

🔶 Comprehensive Trend Analysis

Calculates momentum, strength, direction, and confidence levels using volatility-normalized price changes and multi-timeframe correlation. The system provides real-time trend state tracking with bullish (+1), bearish (-1), or neutral (0) direction assessment and 0-100 confidence scoring.

// Calculate trend momentum using rate of change and volatility

calculateTrendMomentum(lookback) =>

priceChange = (close - close ) / close * 100

avgVolatility = ta.atr(lookback) / close * 100

momentum = priceChange / (avgVolatility + 0.0001)

momentum

// Calculate trend strength using multiple timeframe correlation

calculateTrendStrength(shortPeriod, longPeriod) =>

shortMA = ta.sma(close, shortPeriod)

longMA = ta.sma(close, longPeriod)

separation = math.abs(shortMA - longMA) / longMA * 100

strength = separation * slopeAlignment

❓How It Works

🔶 Imbalance Zone Detection

Identifies Fair Value Gaps (FVGs) between consecutive candles where price gaps create unfilled areas. These zones are displayed as semi-transparent boxes with optional center line mitigation tracking, highlighting potential support and resistance levels where institutional players often react.

// Detect Fair Value Gaps

detectPriceImbalance() =>

currentHigh = high

currentLow = low

refHigh = high

refLow = low

if currentOpen > currentClose

if currentHigh - refLow < 0

upperBound = currentClose - (currentClose - refLow)

lowerBound = currentClose - (currentClose - currentHigh)

centerPoint = (upperBound + lowerBound) / 2

newZone = ImbalanceZone.new(

zoneBox = box.new(bar_index, upperBound, rightEdge, lowerBound,

bgcolor=bullishImbalanceColor, border_color=hiddenColor)

)

🔶 Structure Break Analysis

Determines Break of Structure (BOS) for trend continuation and Directional Change (DC) for trend reversals with advanced classification as "continuation", "reversal", or "neutral". The system compares pre-trend and post-trend states for each break, providing comprehensive trend change momentum analysis.

🔶 Intelligent Zone Management

Features partial mitigation tracking when price enters but doesn't fully fill zones, with automatic zone boundary adjustment during partial fills. Smart array management keeps only recent structure points for optimal performance while preventing duplicate signals from the same level.

🔶 Liquidity Zone Detection

Automatically identifies potential liquidity zones at key structure points for institutional trading analysis. The system tracks broken structure points and provides adaptive zone extension with configurable time-based limits for imbalance areas.

🔶 Visual Structure Mapping

Provides clear visual indicators including swing labels with color-coded significance levels, dashed lines connecting break points with BOS/DC labels, and break signals for continuation and reversal patterns. The adaptive zones feature smart management with automatic mitigation tracking.

🔶 Market Structure Interpretation

HH/HL patterns indicate bullish market structure with trend continuation likelihood, while LH/LL patterns signal bearish structure with downtrend continuation expected. BOS signals represent structure breaks in trend direction for continuation opportunities, while DC signals warn of potential reversals.

🔶 Performance Optimization

Automatic cleanup of old structure points (keeps last 8 points), recent break tracking (keeps last 5 break events), and efficient array management ensure smooth performance across all timeframes and market conditions.

Why Choose Ultimate Market Structure ?

This indicator provides traders with institutional-grade market structure analysis, combining multiple analytical approaches into one comprehensive tool. By identifying key structure levels, imbalance zones, and break patterns with advanced significance scoring, it helps traders understand market dynamics and position themselves for high-probability trade setups in alignment with smart money concepts. The sophisticated trend scoring system and intelligent zone management make it an essential tool for any serious trader looking to decode market structure with precision and confidence.

Wavelet-Trend ML Integration [Alpha Extract]Alpha-Extract Volatility Quality Indicator

The Alpha-Extract Volatility Quality (AVQ) Indicator provides traders with deep insights into market volatility by measuring the directional strength of price movements. This sophisticated momentum-based tool helps identify overbought and oversold conditions, offering actionable buy and sell signals based on volatility trends and standard deviation bands.

🔶 CALCULATION

The indicator processes volatility quality data through a series of analytical steps:

Bar Range Calculation: Measures true range (TR) to capture price volatility.

Directional Weighting: Applies directional bias (positive for bullish candles, negative for bearish) to the true range.

VQI Computation: Uses an exponential moving average (EMA) of weighted volatility to derive the Volatility Quality Index (VQI).

Smoothing: Applies an additional EMA to smooth the VQI for clearer signals.

Normalization: Optionally normalizes VQI to a -100/+100 scale based on historical highs and lows.

Standard Deviation Bands: Calculates three upper and lower bands using standard deviation multipliers for volatility thresholds.

Signal Generation: Produces overbought/oversold signals when VQI reaches extreme levels (±200 in normalized mode).

Formula:

Bar Range = True Range (TR)

Weighted Volatility = Bar Range × (Close > Open ? 1 : Close < Open ? -1 : 0)

VQI Raw = EMA(Weighted Volatility, VQI Length)

VQI Smoothed = EMA(VQI Raw, Smoothing Length)

VQI Normalized = ((VQI Smoothed - Lowest VQI) / (Highest VQI - Lowest VQI) - 0.5) × 200

Upper Band N = VQI Smoothed + (StdDev(VQI Smoothed, VQI Length) × Multiplier N)

Lower Band N = VQI Smoothed - (StdDev(VQI Smoothed, VQI Length) × Multiplier N)

🔶 DETAILS

Visual Features:

VQI Plot: Displays VQI as a line or histogram (lime for positive, red for negative).

Standard Deviation Bands: Plots three upper and lower bands (teal for upper, grayscale for lower) to indicate volatility thresholds.

Reference Levels: Horizontal lines at 0 (neutral), +100, and -100 (in normalized mode) for context.

Zone Highlighting: Overbought (⋎ above bars) and oversold (⋏ below bars) signals for extreme VQI levels (±200 in normalized mode).

Candle Coloring: Optional candle overlay colored by VQI direction (lime for positive, red for negative).

Interpretation:

VQI ≥ 200 (Normalized): Overbought condition, strong sell signal.

VQI 100–200: High volatility, potential selling opportunity.

VQI 0–100: Neutral bullish momentum.

VQI 0 to -100: Neutral bearish momentum.

VQI -100 to -200: High volatility, strong bearish momentum.

VQI ≤ -200 (Normalized): Oversold condition, strong buy signal.

🔶 EXAMPLES

Overbought Signal Detection: When VQI exceeds 200 (normalized), the indicator flags potential market tops with a red ⋎ symbol.

Example: During strong uptrends, VQI reaching 200 has historically preceded corrections, allowing traders to secure profits.

Oversold Signal Detection: When VQI falls below -200 (normalized), a lime ⋏ symbol highlights potential buying opportunities.

Example: In bearish markets, VQI dropping below -200 has marked reversal points for profitable long entries.

Volatility Trend Tracking: The VQI plot and bands help traders visualize shifts in market momentum.

Example: A rising VQI crossing above zero with widening bands indicates strengthening bullish momentum, guiding traders to hold or enter long positions.

Dynamic Support/Resistance: Standard deviation bands act as dynamic volatility thresholds during price movements.

Example: Price reversals often occur near the third standard deviation bands, providing reliable entry/exit points during volatile periods.

🔶 SETTINGS

Customization Options:

VQI Length: Adjust the EMA period for VQI calculation (default: 14, range: 1–50).

Smoothing Length: Set the EMA period for smoothing (default: 5, range: 1–50).

Standard Deviation Multipliers: Customize multipliers for bands (defaults: 1.0, 2.0, 3.0).

Normalization: Toggle normalization to -100/+100 scale and adjust lookback period (default: 200, min: 50).

Display Style: Switch between line or histogram plot for VQI.

Candle Overlay: Enable/disable VQI-colored candles (lime for positive, red for negative).

The Alpha-Extract Volatility Quality Indicator empowers traders with a robust tool to navigate market volatility. By combining directional price range analysis with smoothed volatility metrics, it identifies overbought and oversold conditions, offering clear buy and sell signals. The customizable standard deviation bands and optional normalization provide precise context for market conditions, enabling traders to make informed decisions across various market cycles.

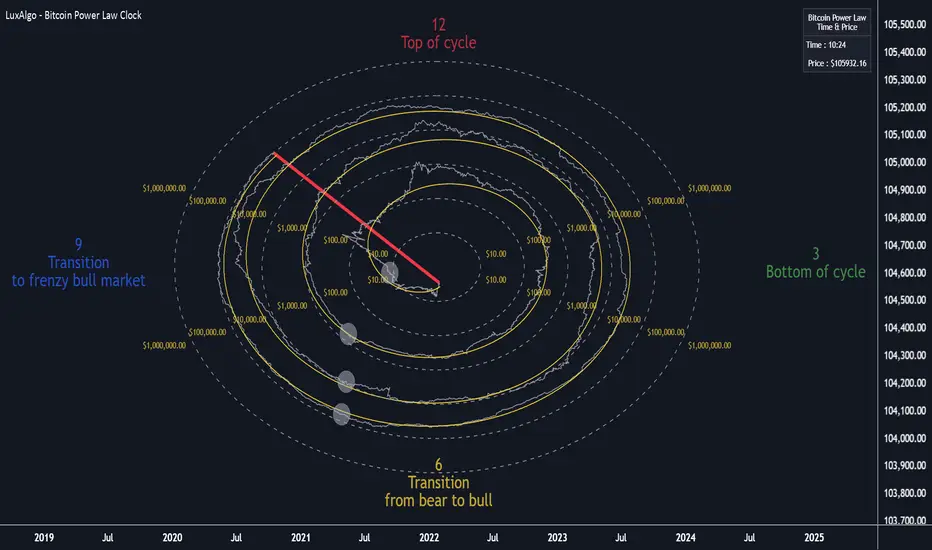

Bitcoin Power Law Clock [LuxAlgo]The Bitcoin Power Law Clock is a unique representation of Bitcoin prices proposed by famous Bitcoin analyst and modeler Giovanni Santostasi.

It displays a clock-like figure with the Bitcoin price and average lines as spirals, as well as the 12, 3, 6, and 9 hour marks as key points in the cycle.

🔶 USAGE

Giovanni Santostasi, Ph.D., is the creator and discoverer of the Bitcoin Power Law Theory. He is passionate about Bitcoin and has 12 years of experience analyzing it and creating price models.

As we can see in the above chart, the tool is super intuitive. It displays a clock-like figure with the current Bitcoin price at 10:20 on a 12-hour scale.

This tool only works on the 1D INDEX:BTCUSD chart. The ticker and timeframe must be exact to ensure proper functionality.

According to the Bitcoin Power Law Theory, the key cycle points are marked at the extremes of the clock: 12, 3, 6, and 9 hours. According to the theory, the current Bitcoin prices are in a frenzied bull market on their way to the top of the cycle.

🔹 Enable/Disable Elements

All of the elements on the clock can be disabled. If you disable them all, only an empty space will remain.

The different charts above show various combinations. Traders can customize the tool to their needs.

🔹 Auto scale

The clock has an auto-scale feature that is enabled by default. Traders can adjust the size of the clock by disabling this feature and setting the size in the settings panel.

The image above shows different configurations of this feature.

🔶 SETTINGS

🔹 Price

Price: Enable/disable price spiral, select color, and enable/disable curved mode

Average: Enable/disable average spiral, select color, and enable/disable curved mode

🔹 Style

Auto scale: Enable/disable automatic scaling or set manual fixed scaling for the spirals

Lines width: Width of each spiral line

Text Size: Select text size for date tags and price scales

Prices: Enable/disable price scales on the x-axis

Handle: Enable/disable clock handle

Halvings: Enable/disable Halvings

Hours: Enable/disable hours and key cycle points

🔹 Time & Price Dashboard

Show Time & Price: Enable/disable time & price dashboard

Location: Dashboard location

Size: Dashboard size

Bitcoin Power Law [LuxAlgo]The Bitcoin Power Law tool is a representation of Bitcoin prices first proposed by Giovanni Santostasi, Ph.D. It plots BTCUSD daily closes on a log10-log10 scale, and fits a linear regression channel to the data.

This channel helps traders visualise when the price is historically in a zone prone to tops or located within a discounted zone subject to future growth.

🔶 USAGE

Giovanni Santostasi, Ph.D. originated the Bitcoin Power-Law Theory; this implementation places it directly on a TradingView chart. The white line shows the daily closing price, while the cyan line is the best-fit regression.

A channel is constructed from the linear fit root mean squared error (RMSE), we can observe how price has repeatedly oscillated between each channel areas through every bull-bear cycle.

Excursions into the upper channel area can be followed by price surges and finishing on a top, whereas price touching the lower channel area coincides with a cycle low.

Users can change the channel areas multipliers, helping capture moves more precisely depending on the intended usage.

This tool only works on the daily BTCUSD chart. Ticker and timeframe must match exactly for the calculations to remain valid.

🔹 Linear Scale

Users can toggle on a linear scale for the time axis, in order to obtain a higher resolution of the price, (this will affect the linear regression channel fit, making it look poorer).

🔶 DETAILS

One of the advantages of the Power Law Theory proposed by Giovanni Santostasi is its ability to explain multiple behaviors of Bitcoin. We describe some key points below.

🔹 Power-Law Overview

A power law has the form y = A·xⁿ , and Bitcoin’s key variables follow this pattern across many orders of magnitude. Empirically, price rises roughly with t⁶, hash-rate with t¹² and the number of active addresses with t³.

When we plot these on log-log axes they appear as straight lines, revealing a scale-invariant system whose behaviour repeats proportionally as it grows.

🔹 Feedback-Loop Dynamics

Growth begins with new users, whose presence pushes the price higher via a Metcalfe-style square-law. A richer price pool funds more mining hardware; the Difficulty Adjustment immediately raises the hash-rate requirement, keeping profit margins razor-thin.

A higher hash rate secures the network, which in turn attracts the next wave of users. Because risk and Difficulty act as braking forces, user adoption advances as a power of three in time rather than an unchecked S-curve. This circular causality repeats without end, producing the familiar boom-and-bust cadence around the long-term power-law channel.

🔹 Scale Invariance & Predictions

Scale invariance means that enlarging the timeline in log-log space leaves the trajectory unchanged.

The same geometric proportions that described the first dollar of value can therefore extend to a projected million-dollar bitcoin, provided no catastrophic break occurs. Institutional ETF inflows supply fresh capital but do not bend the underlying slope; only a persistent deviation from the line would falsify the current model.

🔹 Implications

The theory assigns scarcity no direct role; iterative feedback and the Difficulty Adjustment are sufficient to govern Bitcoin’s expansion. Long-term valuation should focus on position within the power-law channel, while bubbles—sharp departures above trend that later revert—are expected punctuations of an otherwise steady climb.

Beyond about 2040, disruptive technological shifts could alter the parameters, but for the next order of magnitude the present slope remains the simplest, most robust guide.

Bitcoin behaves less like a traditional asset and more like a self-organising digital organism whose value, security, and adoption co-evolve according to immutable power-law rules.

🔶 SETTINGS

🔹 General

Start Calculation: Determine the start date used by the calculation, with any prior prices being ignored. (default - 15 Jul 2010)

Use Linear Scale for X-Axis: Convert the horizontal axis from log(time) to linear calendar time

🔹 Linear Regression

Show Regression Line: Enable/disable the central power-law trend line

Regression Line Color: Choose the colour of the regression line

Mult 1: Toggle line & fill, set multiplier (default +1), pick line colour and area fill colour

Mult 2: Toggle line & fill, set multiplier (default +0.5), pick line colour and area fill colour

Mult 3: Toggle line & fill, set multiplier (default -0.5), pick line colour and area fill colour

Mult 4: Toggle line & fill, set multiplier (default -1), pick line colour and area fill colour

🔹 Style

Price Line Color: Select the colour of the BTC price plot

Auto Color: Automatically choose the best contrast colour for the price line

Price Line Width: Set the thickness of the price line (1 – 5 px)

Show Halvings: Enable/disable dotted vertical lines at each Bitcoin halving

Halvings Color: Choose the colour of the halving lines

CHN BUY SELL with EMA 200Overview

This indicator combines RSI 7 momentum signals with EMA 200 trend filtering to generate high-probability BUY and SELL entry points. It uses colored candles to highlight key market conditions and displays clear trading signals with built-in cooldown periods to prevent signal spam.

Key Features

Colored Candles: Visual momentum indicators based on RSI 7 levels

Trend Filtering: EMA 200 confirms overall market direction

Signal Cooldown: Prevents over-trading with adjustable waiting periods

Clean Interface: Simple BUY/SELL labels without clutter

How It Works

Candle Coloring System

Yellow Candles: Appear when RSI 7 ≥ 70 (overbought momentum)

Purple Candles: Appear when RSI 7 ≤ 30 (oversold momentum)

Normal Candles: All other market conditions

Trading Signals

BUY Signal: Triggered when closing price > EMA 200 AND yellow candle appears

SELL Signal: Triggered when closing price < EMA 200 AND purple candle appears

Signal Cooldown

After a BUY or SELL signal appears, the same signal type is suppressed for a specified number of candles (default: 5) to prevent excessive signals in ranging markets.

Settings

RSI 7 Length: Period for RSI calculation (default: 7)

RSI 7 Overbought: Threshold for yellow candles (default: 70)

RSI 7 Oversold: Threshold for purple candles (default: 30)

EMA Length: Period for trend filter (default: 200)

Signal Cooldown: Candles to wait between same signal type (default: 5)

How to Use

Apply the indicator to your chart

Look for yellow or purple colored candles

For LONG entries: Wait for yellow candle above EMA 200, then enter BUY when signal appears

For SHORT entries: Wait for purple candle below EMA 200, then enter SELL when signal appears

Use appropriate risk management and position sizing

Best Practices

Works best on timeframes M15 and higher

Suitable for Forex, Gold, Crypto, and Stock markets

Consider market volatility when setting stop-loss and take-profit levels

Use in conjunction with proper risk management strategies

Technical Details