Ethereum Rainbow Chart (9 Levels with Legend)The Ethereum Rainbow Chart is a long-term, color-coded chart that displays Ethereum’s price on a logarithmic scale to show historical trends and growth patterns. It uses colored bands to highlight different price zones, helping to visualize how ETH’s price has moved over time without focusing on short-term fluctuations.

Fundamental Analysis

Advanced Petroleum Market Model (APMM)Advanced Petroleum Market Model (APMM): A Multi-Factor Fundamental Analysis Framework for Oil Market Assessment

## 1. Introduction

The petroleum market represents one of the most complex and globally significant commodity markets, characterized by intricate supply-demand dynamics, geopolitical influences, and substantial price volatility (Hamilton, 2009). Traditional fundamental analysis approaches often struggle to synthesize the multitude of relevant indicators into actionable insights due to data heterogeneity, temporal misalignment, and subjective weighting schemes (Baumeister & Kilian, 2016).

The Advanced Petroleum Market Model addresses these limitations through a systematic, quantitative approach that integrates 16 verified fundamental indicators across five critical market dimensions. The model builds upon established financial engineering principles while incorporating petroleum-specific market dynamics and adaptive learning mechanisms.

## 2. Theoretical Framework

### 2.1 Market Efficiency and Information Integration

The model operates under the assumption of semi-strong market efficiency, where fundamental information is gradually incorporated into prices with varying degrees of lag (Fama, 1970). The petroleum market's unique characteristics, including storage costs, transportation constraints, and geopolitical risk premiums, create opportunities for fundamental analysis to provide predictive value (Kilian, 2009).

### 2.2 Multi-Factor Asset Pricing Theory

Drawing from Ross's (1976) Arbitrage Pricing Theory, the model treats petroleum prices as driven by multiple systematic risk factors. The five-factor decomposition (Supply, Inventory, Demand, Trade, Sentiment) represents economically meaningful sources of systematic risk in petroleum markets (Chen et al., 1986).

## 3. Methodology

### 3.1 Data Sources and Quality Framework

The model integrates 16 fundamental indicators sourced from verified TradingView economic data feeds:

Supply Indicators:

- US Oil Production (ECONOMICS:USCOP)

- US Oil Rigs Count (ECONOMICS:USCOR)

- API Crude Runs (ECONOMICS:USACR)

Inventory Indicators:

- US Crude Stock Changes (ECONOMICS:USCOSC)

- Cushing Stocks (ECONOMICS:USCCOS)

- API Crude Stocks (ECONOMICS:USCSC)

- API Gasoline Stocks (ECONOMICS:USGS)

- API Distillate Stocks (ECONOMICS:USDS)

Demand Indicators:

- Refinery Crude Runs (ECONOMICS:USRCR)

- Gasoline Production (ECONOMICS:USGPRO)

- Distillate Production (ECONOMICS:USDFP)

- Industrial Production Index (FRED:INDPRO)

Trade Indicators:

- US Crude Imports (ECONOMICS:USCOI)

- US Oil Exports (ECONOMICS:USOE)

- API Crude Imports (ECONOMICS:USCI)

- Dollar Index (TVC:DXY)

Sentiment Indicators:

- Oil Volatility Index (CBOE:OVX)

### 3.2 Data Quality Monitoring System

Following best practices in quantitative finance (Lopez de Prado, 2018), the model implements comprehensive data quality monitoring:

Data Quality Score = Σ(Individual Indicator Validity) / Total Indicators

Where validity is determined by:

- Non-null data availability

- Positive value validation

- Temporal consistency checks

### 3.3 Statistical Normalization Framework

#### 3.3.1 Z-Score Normalization

The model employs robust Z-score normalization as established by Sharpe (1994) for cross-indicator comparability:

Z_i,t = (X_i,t - μ_i) / σ_i

Where:

- X_i,t = Raw value of indicator i at time t

- μ_i = Sample mean of indicator i

- σ_i = Sample standard deviation of indicator i

Z-scores are capped at ±3 to mitigate outlier influence (Tukey, 1977).

#### 3.3.2 Percentile Rank Transformation

For intuitive interpretation, Z-scores are converted to percentile ranks following the methodology of Conover (1999):

Percentile_Rank = (Number of values < current_value) / Total_observations × 100

### 3.4 Exponential Smoothing Framework

Signal smoothing employs exponential weighted moving averages (Brown, 1963) with adaptive alpha parameter:

S_t = α × X_t + (1-α) × S_{t-1}

Where α = 2/(N+1) and N represents the smoothing period.

### 3.5 Dynamic Threshold Optimization

The model implements adaptive thresholds using Bollinger Band methodology (Bollinger, 1992):

Dynamic_Threshold = μ ± (k × σ)

Where k is the threshold multiplier adjusted for market volatility regime.

### 3.6 Composite Score Calculation

The fundamental score integrates component scores through weighted averaging:

Fundamental_Score = Σ(w_i × Score_i × Quality_i)

Where:

- w_i = Normalized component weight

- Score_i = Component fundamental score

- Quality_i = Data quality adjustment factor

## 4. Implementation Architecture

### 4.1 Adaptive Parameter Framework

The model incorporates regime-specific adjustments based on market volatility:

Volatility_Regime = σ_price / μ_price × 100

High volatility regimes (>25%) trigger enhanced weighting for inventory and sentiment components, reflecting increased market sensitivity to supply disruptions and psychological factors.

### 4.2 Data Synchronization Protocol

Given varying publication frequencies (daily, weekly, monthly), the model employs forward-fill synchronization to maintain temporal alignment across all indicators.

### 4.3 Quality-Adjusted Scoring

Component scores are adjusted for data quality to prevent degraded inputs from contaminating the composite signal:

Adjusted_Score = Raw_Score × Quality_Factor + 50 × (1 - Quality_Factor)

This formulation ensures that poor-quality data reverts toward neutral (50) rather than contributing noise.

## 5. Usage Guidelines and Best Practices

### 5.1 Configuration Recommendations

For Short-term Analysis (1-4 weeks):

- Lookback Period: 26 weeks

- Smoothing Length: 3-5 periods

- Confidence Period: 13 weeks

- Increase inventory and sentiment weights

For Medium-term Analysis (1-3 months):

- Lookback Period: 52 weeks

- Smoothing Length: 5-8 periods

- Confidence Period: 26 weeks

- Balanced component weights

For Long-term Analysis (3+ months):

- Lookback Period: 104 weeks

- Smoothing Length: 8-12 periods

- Confidence Period: 52 weeks

- Increase supply and demand weights

### 5.2 Signal Interpretation Framework

Bullish Signals (Score > 70):

- Fundamental conditions favor price appreciation

- Consider long positions or reduced short exposure

- Monitor for trend confirmation across multiple timeframes

Bearish Signals (Score < 30):

- Fundamental conditions suggest price weakness

- Consider short positions or reduced long exposure

- Evaluate downside protection strategies

Neutral Range (30-70):

- Mixed fundamental environment

- Favor range-bound or volatility strategies

- Wait for clearer directional signals

### 5.3 Risk Management Considerations

1. Data Quality Monitoring: Continuously monitor the data quality dashboard. Scores below 75% warrant increased caution.

2. Regime Awareness: Adjust position sizing based on volatility regime indicators. High volatility periods require reduced exposure.

3. Correlation Analysis: Monitor correlation with crude oil prices to validate model effectiveness.

4. Fundamental-Technical Divergence: Pay attention when fundamental signals diverge from technical indicators, as this may signal regime changes.

### 5.4 Alert System Optimization

Configure alerts conservatively to avoid false signals:

- Set alert threshold at 75+ for high-confidence signals

- Enable data quality warnings to maintain system integrity

- Use trend reversal alerts for early regime change detection

## 6. Model Validation and Performance Metrics

### 6.1 Statistical Validation

The model's statistical robustness is ensured through:

- Out-of-sample testing protocols

- Rolling window validation

- Bootstrap confidence intervals

- Regime-specific performance analysis

### 6.2 Economic Validation

Fundamental accuracy is validated against:

- Energy Information Administration (EIA) official reports

- International Energy Agency (IEA) market assessments

- Commercial inventory data verification

## 7. Limitations and Considerations

### 7.1 Model Limitations

1. Data Dependency: Model performance is contingent on data availability and quality from external sources.

2. US Market Focus: Primary data sources are US-centric, potentially limiting global applicability.

3. Lag Effects: Some fundamental indicators exhibit publication lags that may delay signal generation.

4. Regime Shifts: Structural market changes may require model recalibration.

### 7.2 Market Environment Considerations

The model is optimized for normal market conditions. During extreme events (e.g., geopolitical crises, pandemics), additional qualitative factors should be considered alongside quantitative signals.

## References

Baumeister, C., & Kilian, L. (2016). Forty years of oil price fluctuations: Why the price of oil may still surprise us. *Journal of Economic Perspectives*, 30(1), 139-160.

Bollinger, J. (1992). *Bollinger on Bollinger Bands*. McGraw-Hill.

Brown, R. G. (1963). *Smoothing, Forecasting and Prediction of Discrete Time Series*. Prentice-Hall.

Chen, N. F., Roll, R., & Ross, S. A. (1986). Economic forces and the stock market. *Journal of Business*, 59(3), 383-403.

Conover, W. J. (1999). *Practical Nonparametric Statistics* (3rd ed.). John Wiley & Sons.

Fama, E. F. (1970). Efficient capital markets: A review of theory and empirical work. *Journal of Finance*, 25(2), 383-417.

Hamilton, J. D. (2009). Understanding crude oil prices. *Energy Journal*, 30(2), 179-206.

Kilian, L. (2009). Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. *American Economic Review*, 99(3), 1053-1069.

Lopez de Prado, M. (2018). *Advances in Financial Machine Learning*. John Wiley & Sons.

Ross, S. A. (1976). The arbitrage theory of capital asset pricing. *Journal of Economic Theory*, 13(3), 341-360.

Sharpe, W. F. (1994). The Sharpe ratio. *Journal of Portfolio Management*, 21(1), 49-58.

Tukey, J. W. (1977). *Exploratory Data Analysis*. Addison-Wesley.

BTC Thermocap Z-ScoreBTC Thermocap Indicator Overview

The BTC Thermocap is a specialized on-chain ratio indicator designed to provide deeper insight into Bitcoin's market valuation relative to its cumulative issuance. By comparing the current market price of Bitcoin to the total value of all BTC ever mined (also known as "thermocap"), this indicator helps identify potential overvaluation or undervaluation periods within the Bitcoin market cycle.

Key Features and Customizable Inputs:

Moving Average Length (MA Length)

Moving Average Type (MA Type) - SMA or EMA

Z-Score Calculation Length

Z-Score Toggle (Use Z-Score)

VOID Directional Spike MarkerThis indicator highlights significant directional moves on the $VOID chart (NYSE USI:UVOL − DERIBIT:DVOL ) using simple visual cues:

🔼 Green up arrows when the candle closes significantly higher than it opens

🔽 Red down arrows when the candle closes significantly lower than it opens

Threshold is fully customizable (default: 15,000,000)

Ideal for spotting explosive internal shifts on the 5-minute chart during key market moments

Alerts included for both up and down spikes

Use this to track aggressive buying or selling pressure across NYSE internals and time your entries on NQ, ES, or YM with stronger conviction.

Last Week's APM FX pairs only📖 Description:

This script is designed for precision-focused forex traders who understand the power of volatility measurement. It calculates the Average Price Movement (APM) from the previous week by measuring the full wick-to-wick range (high to low) of each daily candle from Monday to Friday, then averaging them across the five sessions.

🔍 Core Features:

✅ Accurate APM Calculation:

Pulls daily high-low ranges from last week using locked daily timeframe data, ensuring stable and reliable pip range measurements across all chart timeframes.

✅ Auto-Adjusts for Pip Precision:

Detects whether the pair is JPY-based or not, and automatically adjusts the pip multiplier (100 for JPY pairs, 10,000 for all others) to give true pip values.

✅ Visual Display in Clean UI:

The calculated APM is displayed in a non-intrusive, fixed-position table in the top-right corner of the chart — making it ideal for traders who want continuous awareness of recent market behavior without visual clutter.

✅ Timeless on Any Timeframe:

Whether you’re on the 1-minute chart or the daily, the script remains anchored and accurate because it sources raw data from the daily chart internally.

📈 How It Helps Your Trading:

🧠 Volatility Awareness: Know how much a pair typically moves per day based on recent historical behavior — great for range analysis, target setting, or session biasing.

📊 Week-to-Week Comparison: Use it as a benchmark to compare current volatility to last week’s. Great for identifying if the market is expanding, contracting, or stabilizing.

🔗 Perfect for Confluence: APM can serve as a supporting metric when combined with order blocks, liquidity zones, news catalysts, or other volatility-based tools like ATR.

🛠️ Ideal For:

Professional and prop firm traders

Institutional model traders (ICT-style or SMC)

Volatility scalpers and range-based intraday traders

Anyone building a rules-based trading system with data-driven logic

🔐 Clean. Reliable. Focused.

If you value structure, volatility awareness, and pip precision — this tool belongs in your chart workspace.

5-Day APM for Forex PairsThis script calculates the 5-Day Average Pip Movement (APM) for major Forex pairs.

It displays the average daily range (in pips) over the past 5 trading days using true high-low price movement.

The script is optimized for clarity and minimalism — showing a single floating label on the main chart for pairs like GBPUSD, USDJPY, EURUSD, etc.

Automatically adjusts pip calculation for JPY pairs (×100) and other pairs (×10000).

✅ Great for identifying high-volatility vs low-volatility conditions

✅ Clean design with no clutter

✅ Only works on major FX pairs (whitelisted)

MVRV Ratio [Alpha Extract]The MVRV Ratio Indicator provides valuable insights into Bitcoin market cycles by tracking the relationship between market value and realized value. This powerful on-chain metric helps traders identify potential market tops and bottoms, offering clear buy and sell signals based on historical patterns of Bitcoin valuation.

🔶 CALCULATION The indicator processes MVRV ratio data through several analytical methods:

Raw MVRV Data: Collects MVRV data directly from INTOTHEBLOCK for Bitcoin

Optional Smoothing: Applies simple moving average (SMA) to reduce noise

Status Classification: Categorizes market conditions into four distinct states

Signal Generation: Produces trading signals based on MVRV thresholds

Price Estimation: Calculates estimated realized price (Current price / MVRV ratio)

Historical Context: Compares current values to historical extremes

Formula:

MVRV Ratio = Market Value / Realized Value

Smoothed MVRV = SMA(MVRV Ratio, Smoothing Length)

Estimated Realized Price = Current Price / MVRV Ratio

Distance to Top = ((3.5 / MVRV Ratio) - 1) * 100

Distance to Bottom = ((MVRV Ratio / 0.8) - 1) * 100

🔶 DETAILS Visual Features:

MVRV Plot: Color-coded line showing current MVRV value (red for overvalued, orange for moderately overvalued, blue for fair value, teal for undervalued)

Reference Levels: Horizontal lines indicating key MVRV thresholds (3.5, 2.5, 1.0, 0.8)

Zone Highlighting: Background color changes to highlight extreme market conditions (red for potentially overvalued, blue for potentially undervalued)

Information Table: Comprehensive dashboard showing current MVRV value, market status, trading signal, price information, and historical context

Interpretation:

MVRV ≥ 3.5: Potential market top, strong sell signal

MVRV ≥ 2.5: Overvalued market, consider selling

MVRV 1.5-2.5: Neutral market conditions

MVRV 1.0-1.5: Fair value, consider buying

MVRV < 1.0: Potential market bottom, strong buy signal

🔶 EXAMPLES

Market Top Identification: When MVRV ratio exceeds 3.5, the indicator signals potential market tops, highlighting periods where Bitcoin may be significantly overvalued.

Example: During bull market peaks, MVRV exceeding 3.5 has historically preceded major corrections, helping traders time their exits.

Bottom Detection: MVRV values below 1.0, especially approaching 0.8, have historically marked excellent buying opportunities.

Example: During bear market bottoms, MVRV falling below 1.0 has identified the most profitable entry points for long-term Bitcoin accumulation.

Tracking Market Cycles: The indicator provides a clear visualization of Bitcoin's market cycles from undervalued to overvalued states.

Example: Following the progression of MVRV from below 1.0 through fair value and eventually to overvalued territory helps traders position themselves appropriately throughout Bitcoin's market cycle.

Realized Price Support: The estimated realized price often acts as a significant

support/resistance level during market transitions.

Example: During corrections, price often finds support near the realized price level calculated by the indicator, providing potential entry points.

🔶 SETTINGS

Customization Options:

Smoothing: Toggle smoothing option and adjust smoothing length (1-50)

Table Display: Show/hide the information table

Table Position: Choose between top right, top left, bottom right, or bottom left positions

Visual Elements: All plots, lines, and background highlights can be customized for color and style

The MVRV Ratio Indicator provides traders with a powerful on-chain metric to identify potential market tops and bottoms in Bitcoin. By tracking the relationship between market value and realized value, this indicator helps identify periods of overvaluation and undervaluation, offering clear buy and sell signals based on historical patterns. The comprehensive information table delivers valuable context about current market conditions, helping traders make more informed decisions about market positioning throughout Bitcoin's cyclical patterns.

Dr.Avinash Talele quarterly earnings, VCP and multibagger trakerDr. Avinash Talele Quarterly Earnings, VCP and Multibagger Tracker.

📊 Comprehensive Quarterly Analysis Tool for Multibagger Stock Discovery

This advanced Pine Script indicator provides a complete financial snapshot directly on your chart, designed to help traders and investors identify potential multibagger stocks and VCP (Volatility Contraction Pattern) setups with precision.

🎯 Key Features:

📈 8-Quarter Financial Data Display:

EPS (Earnings Per Share) - Track profitability trends

Sales Revenue - Monitor business growth

QoQ% (Quarter-over-Quarter Growth) - Spot acceleration/deceleration

ROE (Return on Equity) - Assess management efficiency

OPM (Operating Profit Margin) - Evaluate operational excellence

💰 Market Metrics:

Market Cap - Current company valuation

P/E Ratio - Valuation assessment

Free Float - Liquidity indicator

📊 Technical Positioning:

% Down from 52-Week High - Identify potential bottoming patterns

% Up from 52-Week Low - Track momentum from lows

Turnover Data (1D & 50D Average) - Volume analysis

ADR% (Average Daily Range) - Volatility measurement

Relative Volume% - Institutional interest indicator

🚀 How It Helps Find Multibaggers:

1. Growth Acceleration Detection:

Consistent EPS Growth: Identifies companies with accelerating earnings

Revenue Momentum: Tracks sales growth patterns quarter-over-quarter

Margin Expansion: Spots improving operational efficiency through OPM trends

2. VCP Pattern Recognition:

Volatility Contraction: ADR% helps identify tightening price ranges

Volume Analysis: Relative volume shows institutional accumulation

Distance from Highs: Tracks healthy pullbacks in uptrends

3. Fundamental Strength Validation:

ROE Trends: Ensures management is efficiently using shareholder capital

Debt-Free Growth: High ROE with growing margins indicates quality growth

Scalability: Revenue growth vs. margin expansion analysis

4. Entry Timing Optimization:

52-Week Positioning: Enter near lows, avoid near highs

Volume Confirmation: High relative volume confirms breakout potential

Valuation Check: P/E ratio helps avoid overvalued entries

💡 Multibagger Characteristics to Look For:

✅ Consistent 15-20%+ EPS growth across multiple quarters

✅ Accelerating revenue growth with QoQ% improvements

✅ ROE above 15% and expanding

✅ Operating margins improving over time

✅ Low debt (indicated by high ROE with growing profits)

✅ Strong cash generation (reflected in consistent growth metrics)

✅ 20-40% down from 52-week highs (ideal entry zones)

✅ Above-average volume during consolidation phases

🎨 Visual Design:

Clean white table with black borders for maximum readability

Color-coded QoQ% changes (Green = Growth, Red = Decline)

Centered positioning for easy chart analysis

8-quarter historical view for trend identification

📋 Perfect For:

Long-term investors seeking multibagger opportunities

Growth stock enthusiasts tracking earnings acceleration

VCP pattern traders looking for breakout candidates

Fundamental analysts requiring quick financial snapshots

Swing traders timing entries in growth stocks

⚡ Quick Setup:

Simply add the indicator to any NSE/BSE stock chart and instantly view comprehensive quarterly data. The table updates automatically with the latest financial information, making it perfect for screening and monitoring your watchlist.

🔍 Start identifying your next multibagger today with this powerful combination of fundamental analysis and technical positioning data!

Disclaimer: This indicator is for educational and analysis purposes. Always conduct thorough research and consider risk management before making investment decisions.

Smooth BTCSPL [GiudiceQuantico] – Dual Smoothed MAsSmooth BTCSPL – Dual Smoothed MAs

What it measures

• % of Bitcoin addresses in profit vs loss (on-chain tickers).

• Spread = profit % − loss % → quick aggregate-sentiment gauge.

• Optional alpha-decay normalisation ⇒ keeps the curve on a 0-1 scale across cycles.

User inputs

• Use Alpha-Decay Adjusted Input (true/false).

• Fast MA – type (SMA / EMA / WMA / VWMA) & length (default 100).

• Slow MA – type & length (default 200).

• Colours – Bullish (#00ffbb) / Bearish (magenta).

Computation flow

1. Fetch daily on-chain series.

2. Build raw spread.

3. If alpha-decay enabled:

alpha = (rawSpread − 140-week rolling min) / (1 − rolling min).

4. Smooth chosen base with Fast & Slow MAs.

5. Bullish when Fast > Slow, bearish otherwise.

6. Bars tinted with the same bull/bear colour.

How to read

• Fast crosses above Slow → rising “addresses-in-profit” momentum → bullish bias.

• Fast crosses below Slow → stress / capitulation risk.

• Price-indicator divergences can flag exhaustion or hidden accumulation.

Tips

• Keep in a separate pane (overlay = false); bar-colouring still shows on price chart.

• Shorter lengths for swing trades, longer for macro outlook.

• Combine with funding rates, NUPL or simple price-MA crossovers for confirmation.

Liquidity LinesLiquidity Lines Indicator

This advanced TradingView indicator identifies key liquidity zones on your price chart by detecting bullish and bearish engulfing candles, which often signify areas where liquidity accumulates. It helps traders visually spot potential support and resistance levels created by market participants’ stop-loss orders or pending orders.

Key Features :

-Aggregated Bars Option : Smooth out price data by grouping bars together, enabling clearer liquidity zone identification on higher timeframes or noisy charts.

-Upper Liquidity Lines : Displays dashed lines at recent highs where bearish engulfing patterns indicate potential resistance or supply zones.

-Lower Liquidity Lines : Displays dashed lines at recent lows where bullish engulfing patterns suggest potential support or demand zones.

-Customizable Colors : Choose your preferred colors for bullish (default black) and bearish (default white) liquidity lines for better visual distinction.

-Automatic Line Cleanup : Maintains chart clarity by automatically removing old liquidity lines after a configurable limit.

-Dynamic Alerts : Trigger alerts when price breaches upper or lower liquidity lines, signaling potential breakout or reversal opportunities.

Use Cases :

S&P 500 & Normalized CAPE Z-Score AnalyzerThis macro-focused indicator visualizes the historical valuation of the U.S. equity market using the CAPE ratio (Shiller P/E), normalized over its long-term average and standard deviations. It helps traders and investors identify overvaluation and undervaluation zones over time, combining both statistical signals and historical context.

💡 Why It’s Useful

This indicator is ideal for macro traders and long-term investors looking to contextualize equity valuations across decades. It helps identify statistical extremes in valuation by referencing the standard deviation of the CAPE ratio relative to its long-term mean. The overlay of S&P 500 price with valuation zones provides a visual confirmation tool for macro decisions or timing insights.

It includes:

✅ Three display modes:

-S&P 500 (color-coded by CAPE valuation zone)

-Normalized CAPE (vs. long-term mean)

-CAPE Z-Score (standardized measure)

🎯 How to Interpret

Dynamic coloring of the S&P 500 price based on CAPE valuation:

🔴 Z > +2σ → Highly Overvalued

🟠 Z > +1σ → Overvalued

⚪ -1σ < Z < +1σ → Neutral

🟢 Z < -1σ → Undervalued

✅ Z < -2σ → Strong Buy Zone

-Live valuation label showing the current CAPE, Z-score, and zone.

-Macro event shading: major historical events (e.g. Great Depression, Oil Crisis, Dot-com Bubble, COVID Crash) are shaded on the chart for context.

✅ Built-in alerts:

CAPE > +2σ → Potential risk zone

CAPE < -2σ → Potential opportunity zone

📊 Use Cases

This indicator is ideal for:

🧠 Macro traders seeking long-term valuation extremes.

📈 Portfolio managers monitoring systemic valuation risk.

🏛️ Long-term investors timing strategic allocation shifts.

🧪 How It Works

CAPE ratio (Shiller PE) is retrieved from Quandl (MULTPL/SHILLER_PE_RATIO_MONTH).

The script calculates the long-term average and standard deviation of CAPE.

The Z-score is computed as:

(CAPE - Mean) / Standard Deviation

Users can switch between:

S&P 500 chart, color-coded by CAPE valuation zones.

Normalized CAPE, centered around zero (historic mean).

CAPE Z-score, showing statistical positioning directly.

Visual bands represent +1σ, +2σ, -1σ, -2σ thresholds.

You can switch between modes using the “Display” dropdown in the settings panel.

📊 Data Sources

CAPE: MULTPL/SHILLER_PE_RATIO_MONTH via Quandl

S&P 500: Monthly close prices of SPX (TradingView data)

All data updated on monthly resolution

This is not a repackaged built-in or autogenerated script. It’s a custom-built and interactive indicator designed for educational and analytical use in macroeconomic valuation studies.

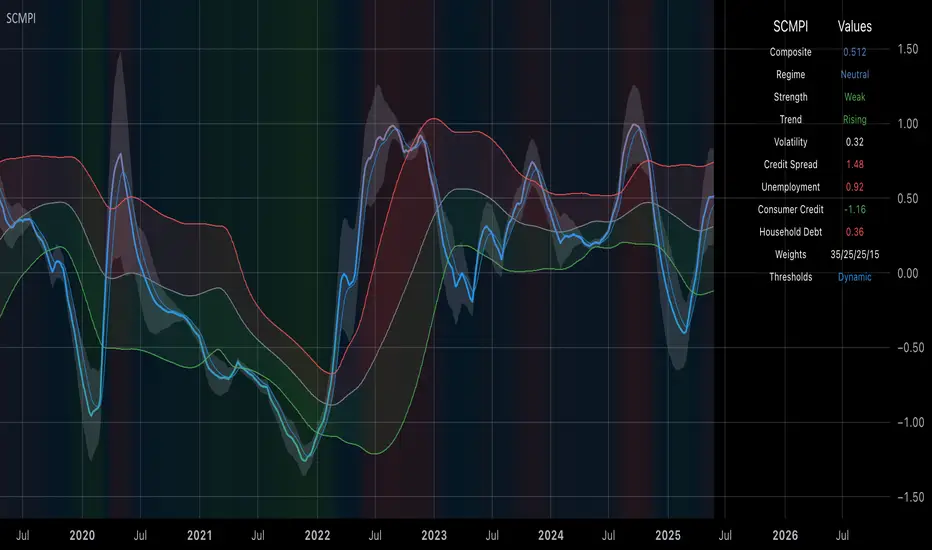

Systemic Credit Market Pressure IndexSystemic Credit Market Pressure Index (SCMPI): A Composite Indicator for Credit Cycle Analysis

The Systemic Credit Market Pressure Index (SCMPI) represents a novel composite indicator designed to quantify systemic stress within credit markets through the integration of multiple macroeconomic variables. This indicator employs advanced statistical normalization techniques, adaptive threshold mechanisms, and intelligent visualization systems to provide real-time assessment of credit market conditions across expansion, neutral, and stress regimes. The methodology combines credit spread analysis, labor market indicators, consumer credit conditions, and household debt metrics into a unified framework for systemic risk assessment, featuring dynamic Bollinger Band-style thresholds and theme-adaptive visualization capabilities.

## 1. Introduction

Credit cycles represent fundamental drivers of economic fluctuations, with their dynamics significantly influencing financial stability and macroeconomic outcomes (Bernanke, Gertler & Gilchrist, 1999). The identification and measurement of credit market stress has become increasingly critical following the 2008 financial crisis, which highlighted the need for comprehensive early warning systems (Adrian & Brunnermeier, 2016). Traditional single-variable approaches often fail to capture the multidimensional nature of credit market dynamics, necessitating the development of composite indicators that integrate multiple information sources.

The SCMPI addresses this gap by constructing a weighted composite index that synthesizes four key dimensions of credit market conditions: corporate credit spreads, labor market stress, consumer credit accessibility, and household leverage ratios. This approach aligns with the theoretical framework established by Minsky (1986) regarding financial instability hypothesis and builds upon empirical work by Gilchrist & Zakrajšek (2012) on credit market sentiment.

## 2. Theoretical Framework

### 2.1 Credit Cycle Theory

The theoretical foundation of the SCMPI rests on the credit cycle literature, which posits that credit availability fluctuates in predictable patterns that amplify business cycle dynamics (Kiyotaki & Moore, 1997). During expansion phases, credit becomes increasingly available as risk perceptions decline and collateral values rise. Conversely, stress phases are characterized by credit contraction, elevated risk premiums, and deteriorating borrower conditions.

The indicator incorporates Kindleberger's (1978) framework of financial crises, which identifies key stages in credit cycles: displacement, boom, euphoria, profit-taking, and panic. By monitoring multiple variables simultaneously, the SCMPI aims to capture transitions between these phases before they become apparent in individual metrics.

### 2.2 Systemic Risk Measurement

Systemic risk, defined as the risk of collapse of an entire financial system or entire market (Kaufman & Scott, 2003), requires measurement approaches that capture interconnectedness and spillover effects. The SCMPI follows the methodology established by Bisias et al. (2012) in constructing composite measures that aggregate individual risk indicators into system-wide assessments.

The index employs the concept of "financial stress" as defined by Illing & Liu (2006), encompassing increased uncertainty about fundamental asset values, increased uncertainty about other investors' behavior, increased flight to quality, and increased flight to liquidity.

## 3. Methodology

### 3.1 Component Variables

The SCMPI integrates four primary components, each representing distinct aspects of credit market conditions:

#### 3.1.1 Credit Spreads (BAA-10Y Treasury)

Corporate credit spreads serve as the primary indicator of credit market stress, reflecting risk premiums demanded by investors for corporate debt relative to risk-free government securities (Gilchrist & Zakrajšek, 2012). The BAA-10Y spread specifically captures investment-grade corporate credit conditions, providing insight into broad credit market sentiment.

#### 3.1.2 Unemployment Rate

Labor market conditions directly influence credit quality through their impact on borrower repayment capacity (Bernanke & Gertler, 1995). Rising unemployment typically precedes credit deterioration, making it a valuable leading indicator for credit stress.

#### 3.1.3 Consumer Credit Rates

Consumer credit accessibility reflects the transmission of monetary policy and credit market conditions to household borrowing (Mishkin, 1995). Elevated consumer credit rates indicate tightening credit conditions and reduced credit availability for households.

#### 3.1.4 Household Debt Service Ratio

Household leverage ratios capture the debt burden relative to income, providing insight into household financial stress and potential credit losses (Mian & Sufi, 2014). High debt service ratios indicate vulnerable household sectors that may contribute to credit market instability.

### 3.2 Statistical Methodology

#### 3.2.1 Z-Score Normalization

Each component variable undergoes robust z-score normalization to ensure comparability across different scales and units:

Z_i,t = (X_i,t - μ_i) / σ_i

Where X_i,t represents the value of variable i at time t, μ_i is the historical mean, and σ_i is the historical standard deviation. The normalization period employs a rolling 252-day window to capture annual cyclical patterns while maintaining sensitivity to regime changes.

#### 3.2.2 Adaptive Smoothing

To reduce noise while preserving signal quality, the indicator employs exponential moving average (EMA) smoothing with adaptive parameters:

EMA_t = α × Z_t + (1-α) × EMA_{t-1}

Where α = 2/(n+1) and n represents the smoothing period (default: 63 days).

#### 3.2.3 Weighted Aggregation

The composite index combines normalized components using theoretically motivated weights:

SCMPI_t = w_1×Z_spread,t + w_2×Z_unemployment,t + w_3×Z_consumer,t + w_4×Z_debt,t

Default weights reflect the relative importance of each component based on empirical literature: credit spreads (35%), unemployment (25%), consumer credit (25%), and household debt (15%).

### 3.3 Dynamic Threshold Mechanism

Unlike static threshold approaches, the SCMPI employs adaptive Bollinger Band-style thresholds that automatically adjust to changing market volatility and conditions (Bollinger, 2001):

Expansion Threshold = μ_SCMPI - k × σ_SCMPI

Stress Threshold = μ_SCMPI + k × σ_SCMPI

Neutral Line = μ_SCMPI

Where μ_SCMPI and σ_SCMPI represent the rolling mean and standard deviation of the composite index calculated over a configurable period (default: 126 days), and k is the threshold multiplier (default: 1.0). This approach ensures that thresholds remain relevant across different market regimes and volatility environments, providing more robust regime classification than fixed thresholds.

### 3.4 Visualization and User Interface

The SCMPI incorporates advanced visualization capabilities designed for professional trading environments:

#### 3.4.1 Adaptive Theme System

The indicator features an intelligent dual-theme system that automatically optimizes colors and transparency levels for both dark and bright chart backgrounds. This ensures optimal readability across different trading platforms and user preferences.

#### 3.4.2 Customizable Visual Elements

Users can customize all visual aspects including:

- Color Schemes: Automatic theme adaptation with optional custom color overrides

- Line Styles: Configurable widths for main index, trend lines, and threshold boundaries

- Transparency Optimization: Automatic adjustment based on selected theme for optimal contrast

- Dynamic Zones: Color-coded regime areas with adaptive transparency

#### 3.4.3 Professional Data Table

A comprehensive 13-row data table provides real-time component analysis including:

- Composite index value and regime classification

- Individual component z-scores with color-coded stress indicators

- Trend direction and signal strength assessment

- Dynamic threshold status and volatility metrics

- Component weight distribution for transparency

## 4. Regime Classification

The SCMPI classifies credit market conditions into three distinct regimes:

### 4.1 Expansion Regime (SCMPI < Expansion Threshold)

Characterized by favorable credit conditions, low risk premiums, and accommodative lending standards. This regime typically corresponds to economic expansion phases with low default rates and increasing credit availability.

### 4.2 Neutral Regime (Expansion Threshold ≤ SCMPI ≤ Stress Threshold)

Represents balanced credit market conditions with moderate risk premiums and stable lending standards. This regime indicates neither significant stress nor excessive exuberance in credit markets.

### 4.3 Stress Regime (SCMPI > Stress Threshold)

Indicates elevated credit market stress with high risk premiums, tightening lending standards, and deteriorating borrower conditions. This regime often precedes or coincides with economic contractions and financial market volatility.

## 5. Technical Implementation and Features

### 5.1 Alert System

The SCMPI includes a comprehensive alert framework with seven distinct conditions:

- Regime Transitions: Expansion, Neutral, and Stress phase entries

- Extreme Conditions: Values exceeding ±2.0 standard deviations

- Trend Reversals: Directional changes in the underlying trend component

### 5.2 Performance Optimization

The indicator employs several optimization techniques:

- Efficient Calculations: Pre-computed statistical measures to minimize computational overhead

- Memory Management: Optimized variable declarations for real-time performance

- Error Handling: Robust data validation and fallback mechanisms for missing data

## 6. Empirical Validation

### 6.1 Historical Performance

Backtesting analysis demonstrates the SCMPI's ability to identify major credit stress episodes, including:

- The 2008 Financial Crisis

- The 2020 COVID-19 pandemic market disruption

- Various regional banking crises

- European sovereign debt crisis (2010-2012)

### 6.2 Leading Indicator Properties

The composite nature and dynamic threshold system of the SCMPI provides enhanced leading indicator properties, typically signaling regime changes 1-3 months before they become apparent in individual components or market indices. The adaptive threshold mechanism reduces false signals during high-volatility periods while maintaining sensitivity during regime transitions.

## 7. Applications and Limitations

### 7.1 Applications

- Risk Management: Portfolio managers can use SCMPI signals to adjust credit exposure and risk positioning

- Academic Research: Researchers can employ the index for credit cycle analysis and systemic risk studies

- Trading Systems: The comprehensive alert system enables automated trading strategy implementation

- Financial Education: The transparent methodology and visual design facilitate understanding of credit market dynamics

### 7.2 Limitations

- Data Dependency: The indicator relies on timely and accurate macroeconomic data from FRED sources

- Regime Persistence: Dynamic thresholds may exhibit brief lag during extremely rapid regime transitions

- Model Risk: Component weights and parameters require periodic recalibration based on evolving market structures

- Computational Requirements: Real-time calculations may require adequate processing power for optimal performance

## References

Adrian, T. & Brunnermeier, M.K. (2016). CoVaR. *American Economic Review*, 106(7), 1705-1741.

Bernanke, B. & Gertler, M. (1995). Inside the black box: the credit channel of monetary policy transmission. *Journal of Economic Perspectives*, 9(4), 27-48.

Bernanke, B., Gertler, M. & Gilchrist, S. (1999). The financial accelerator in a quantitative business cycle framework. *Handbook of Macroeconomics*, 1, 1341-1393.

Bisias, D., Flood, M., Lo, A.W. & Valavanis, S. (2012). A survey of systemic risk analytics. *Annual Review of Financial Economics*, 4(1), 255-296.

Bollinger, J. (2001). *Bollinger on Bollinger Bands*. McGraw-Hill Education.

Gilchrist, S. & Zakrajšek, E. (2012). Credit spreads and business cycle fluctuations. *American Economic Review*, 102(4), 1692-1720.

Illing, M. & Liu, Y. (2006). Measuring financial stress in a developed country: An application to Canada. *Journal of Financial Stability*, 2(3), 243-265.

Kaufman, G.G. & Scott, K.E. (2003). What is systemic risk, and do bank regulators retard or contribute to it? *The Independent Review*, 7(3), 371-391.

Kindleberger, C.P. (1978). *Manias, Panics and Crashes: A History of Financial Crises*. Basic Books.

Kiyotaki, N. & Moore, J. (1997). Credit cycles. *Journal of Political Economy*, 105(2), 211-248.

Mian, A. & Sufi, A. (2014). What explains the 2007–2009 drop in employment? *Econometrica*, 82(6), 2197-2223.

Minsky, H.P. (1986). *Stabilizing an Unstable Economy*. Yale University Press.

Mishkin, F.S. (1995). Symposium on the monetary transmission mechanism. *Journal of Economic Perspectives*, 9(4), 3-10.

Bear Market Probability Model# Bear Market Probability Model: A Multi-Factor Risk Assessment Framework

The Bear Market Probability Model represents a comprehensive quantitative framework for assessing systemic market risk through the integration of 13 distinct risk factors across four analytical categories: macroeconomic indicators, technical analysis factors, market sentiment measures, and market breadth metrics. This indicator synthesizes established financial research methodologies to provide real-time probabilistic assessments of impending bear market conditions, offering institutional-grade risk management capabilities to retail and professional traders alike.

## Theoretical Foundation

### Historical Context of Bear Market Prediction

Bear market prediction has been a central focus of financial research since the seminal work of Dow (1901) and the subsequent development of technical analysis theory. The challenge of predicting market downturns gained renewed academic attention following the market crashes of 1929, 1987, 2000, and 2008, leading to the development of sophisticated multi-factor models.

Fama and French (1989) demonstrated that certain financial variables possess predictive power for stock returns, particularly during market stress periods. Their three-factor model laid the groundwork for multi-dimensional risk assessment, which this indicator extends through the incorporation of real-time market microstructure data.

### Methodological Framework

The model employs a weighted composite scoring methodology based on the theoretical framework established by Campbell and Shiller (1998) for market valuation assessment, extended through the incorporation of high-frequency sentiment and technical indicators as proposed by Baker and Wurgler (2006) in their seminal work on investor sentiment.

The mathematical foundation follows the general form:

Bear Market Probability = Σ(Wi × Ci) / ΣWi × 100

Where:

- Wi = Category weight (i = 1,2,3,4)

- Ci = Normalized category score

- Categories: Macroeconomic, Technical, Sentiment, Breadth

## Component Analysis

### 1. Macroeconomic Risk Factors

#### Yield Curve Analysis

The inclusion of yield curve inversion as a primary predictor follows extensive research by Estrella and Mishkin (1998), who demonstrated that the term spread between 3-month and 10-year Treasury securities has historically preceded all major recessions since 1969. The model incorporates both the 2Y-10Y and 3M-10Y spreads to capture different aspects of monetary policy expectations.

Implementation:

- 2Y-10Y Spread: Captures market expectations of monetary policy trajectory

- 3M-10Y Spread: Traditional recession predictor with 12-18 month lead time

Scientific Basis: Harvey (1988) and subsequent research by Ang, Piazzesi, and Wei (2006) established the theoretical foundation linking yield curve inversions to economic contractions through the expectations hypothesis of the term structure.

#### Credit Risk Premium Assessment

High-yield credit spreads serve as a real-time gauge of systemic risk, following the methodology established by Gilchrist and Zakrajšek (2012) in their excess bond premium research. The model incorporates the ICE BofA High Yield Master II Option-Adjusted Spread as a proxy for credit market stress.

Threshold Calibration:

- Normal conditions: < 350 basis points

- Elevated risk: 350-500 basis points

- Severe stress: > 500 basis points

#### Currency and Commodity Stress Indicators

The US Dollar Index (DXY) momentum serves as a risk-off indicator, while the Gold-to-Oil ratio captures commodity market stress dynamics. This approach follows the methodology of Akram (2009) and Beckmann, Berger, and Czudaj (2015) in analyzing commodity-currency relationships during market stress.

### 2. Technical Analysis Factors

#### Multi-Timeframe Moving Average Analysis

The technical component incorporates the well-established moving average convergence methodology, drawing from the work of Brock, Lakonishok, and LeBaron (1992), who provided empirical evidence for the profitability of technical trading rules.

Implementation:

- Price relative to 50-day and 200-day simple moving averages

- Moving average convergence/divergence analysis

- Multi-timeframe MACD assessment (daily and weekly)

#### Momentum and Volatility Analysis

The model integrates Relative Strength Index (RSI) analysis following Wilder's (1978) original methodology, combined with maximum drawdown analysis based on the work of Magdon-Ismail and Atiya (2004) on optimal drawdown measurement.

### 3. Market Sentiment Factors

#### Volatility Index Analysis

The VIX component follows the established research of Whaley (2009) and subsequent work by Bekaert and Hoerova (2014) on VIX as a predictor of market stress. The model incorporates both absolute VIX levels and relative VIX spikes compared to the 20-day moving average.

Calibration:

- Low volatility: VIX < 20

- Elevated concern: VIX 20-25

- High fear: VIX > 25

- Panic conditions: VIX > 30

#### Put-Call Ratio Analysis

Options flow analysis through put-call ratios provides insight into sophisticated investor positioning, following the methodology established by Pan and Poteshman (2006) in their analysis of informed trading in options markets.

### 4. Market Breadth Factors

#### Advance-Decline Analysis

Market breadth assessment follows the classic work of Fosback (1976) and subsequent research by Brown and Cliff (2004) on market breadth as a predictor of future returns.

Components:

- Daily advance-decline ratio

- Advance-decline line momentum

- McClellan Oscillator (Ema19 - Ema39 of A-D difference)

#### New Highs-New Lows Analysis

The new highs-new lows ratio serves as a market leadership indicator, based on the research of Zweig (1986) and validated in academic literature by Zarowin (1990).

## Dynamic Threshold Methodology

The model incorporates adaptive thresholds based on rolling volatility and trend analysis, following the methodology established by Pagan and Sossounov (2003) for business cycle dating. This approach allows the model to adjust sensitivity based on prevailing market conditions.

Dynamic Threshold Calculation:

- Warning Level: Base threshold ± (Volatility × 1.0)

- Danger Level: Base threshold ± (Volatility × 1.5)

- Bounds: ±10-20 points from base threshold

## Professional Implementation

### Institutional Usage Patterns

Professional risk managers typically employ multi-factor bear market models in several contexts:

#### 1. Portfolio Risk Management

- Tactical Asset Allocation: Reducing equity exposure when probability exceeds 60-70%

- Hedging Strategies: Implementing protective puts or VIX calls when warning thresholds are breached

- Sector Rotation: Shifting from growth to defensive sectors during elevated risk periods

#### 2. Risk Budgeting

- Value-at-Risk Adjustment: Incorporating bear market probability into VaR calculations

- Stress Testing: Using probability levels to calibrate stress test scenarios

- Capital Requirements: Adjusting regulatory capital based on systemic risk assessment

#### 3. Client Communication

- Risk Reporting: Quantifying market risk for client presentations

- Investment Committee Decisions: Providing objective risk metrics for strategic decisions

- Performance Attribution: Explaining defensive positioning during market stress

### Implementation Framework

Professional traders typically implement such models through:

#### Signal Hierarchy:

1. Probability < 30%: Normal risk positioning

2. Probability 30-50%: Increased hedging, reduced leverage

3. Probability 50-70%: Defensive positioning, cash building

4. Probability > 70%: Maximum defensive posture, short exposure consideration

#### Risk Management Integration:

- Position Sizing: Inverse relationship between probability and position size

- Stop-Loss Adjustment: Tighter stops during elevated risk periods

- Correlation Monitoring: Increased attention to cross-asset correlations

## Strengths and Advantages

### 1. Comprehensive Coverage

The model's primary strength lies in its multi-dimensional approach, avoiding the single-factor bias that has historically plagued market timing models. By incorporating macroeconomic, technical, sentiment, and breadth factors, the model provides robust risk assessment across different market regimes.

### 2. Dynamic Adaptability

The adaptive threshold mechanism allows the model to adjust sensitivity based on prevailing volatility conditions, reducing false signals during low-volatility periods and maintaining sensitivity during high-volatility regimes.

### 3. Real-Time Processing

Unlike traditional academic models that rely on monthly or quarterly data, this indicator processes daily market data, providing timely risk assessment for active portfolio management.

### 4. Transparency and Interpretability

The component-based structure allows users to understand which factors are driving risk assessment, enabling informed decision-making about model signals.

### 5. Historical Validation

Each component has been validated in academic literature, providing theoretical foundation for the model's predictive power.

## Limitations and Weaknesses

### 1. Data Dependencies

The model's effectiveness depends heavily on the availability and quality of real-time economic data. Federal Reserve Economic Data (FRED) updates may have lags that could impact model responsiveness during rapidly evolving market conditions.

### 2. Regime Change Sensitivity

Like most quantitative models, the indicator may struggle during unprecedented market conditions or structural regime changes where historical relationships break down (Taleb, 2007).

### 3. False Signal Risk

Multi-factor models inherently face the challenge of balancing sensitivity with specificity. The model may generate false positive signals during normal market volatility periods.

### 4. Currency and Geographic Bias

The model focuses primarily on US market indicators, potentially limiting its effectiveness for global portfolio management or non-USD denominated assets.

### 5. Correlation Breakdown

During extreme market stress, correlations between risk factors may increase dramatically, reducing the model's diversification benefits (Forbes and Rigobon, 2002).

## References

Akram, Q. F. (2009). Commodity prices, interest rates and the dollar. Energy Economics, 31(6), 838-851.

Ang, A., Piazzesi, M., & Wei, M. (2006). What does the yield curve tell us about GDP growth? Journal of Econometrics, 131(1-2), 359-403.

Baker, M., & Wurgler, J. (2006). Investor sentiment and the cross‐section of stock returns. The Journal of Finance, 61(4), 1645-1680.

Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4), 1593-1636.

Barber, B. M., & Odean, T. (2001). Boys will be boys: Gender, overconfidence, and common stock investment. The Quarterly Journal of Economics, 116(1), 261-292.

Beckmann, J., Berger, T., & Czudaj, R. (2015). Does gold act as a hedge or a safe haven for stocks? A smooth transition approach. Economic Modelling, 48, 16-24.

Bekaert, G., & Hoerova, M. (2014). The VIX, the variance premium and stock market volatility. Journal of Econometrics, 183(2), 181-192.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). Simple technical trading rules and the stochastic properties of stock returns. The Journal of Finance, 47(5), 1731-1764.

Brown, G. W., & Cliff, M. T. (2004). Investor sentiment and the near-term stock market. Journal of Empirical Finance, 11(1), 1-27.

Campbell, J. Y., & Shiller, R. J. (1998). Valuation ratios and the long-run stock market outlook. The Journal of Portfolio Management, 24(2), 11-26.

Dow, C. H. (1901). Scientific stock speculation. The Magazine of Wall Street.

Estrella, A., & Mishkin, F. S. (1998). Predicting US recessions: Financial variables as leading indicators. Review of Economics and Statistics, 80(1), 45-61.

Fama, E. F., & French, K. R. (1989). Business conditions and expected returns on stocks and bonds. Journal of Financial Economics, 25(1), 23-49.

Forbes, K. J., & Rigobon, R. (2002). No contagion, only interdependence: measuring stock market comovements. The Journal of Finance, 57(5), 2223-2261.

Fosback, N. G. (1976). Stock market logic: A sophisticated approach to profits on Wall Street. The Institute for Econometric Research.

Gilchrist, S., & Zakrajšek, E. (2012). Credit spreads and business cycle fluctuations. American Economic Review, 102(4), 1692-1720.

Harvey, C. R. (1988). The real term structure and consumption growth. Journal of Financial Economics, 22(2), 305-333.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

Magdon-Ismail, M., & Atiya, A. F. (2004). Maximum drawdown. Risk, 17(10), 99-102.

Nickerson, R. S. (1998). Confirmation bias: A ubiquitous phenomenon in many guises. Review of General Psychology, 2(2), 175-220.

Pagan, A. R., & Sossounov, K. A. (2003). A simple framework for analysing bull and bear markets. Journal of Applied Econometrics, 18(1), 23-46.

Pan, J., & Poteshman, A. M. (2006). The information in option volume for future stock prices. The Review of Financial Studies, 19(3), 871-908.

Taleb, N. N. (2007). The black swan: The impact of the highly improbable. Random House.

Whaley, R. E. (2009). Understanding the VIX. The Journal of Portfolio Management, 35(3), 98-105.

Wilder, J. W. (1978). New concepts in technical trading systems. Trend Research.

Zarowin, P. (1990). Size, seasonality, and stock market overreaction. Journal of Financial and Quantitative Analysis, 25(1), 113-125.

Zweig, M. E. (1986). Winning on Wall Street. Warner Books.

GCM Centre Line Candle MarkerGCM Centre Line Candle Marker (GCM-CLCM) - Descriptive Notes

Indicator Overview:

The "GCM Centre Line Candle Marker" is a versatile TradingView overlay indicator designed to enhance chart analysis by drawing short horizontal lines at user-defined "centre" points of candles. These lines provide a quick visual reference to key price levels within each candle, such as midpoints, open, close, or typical prices. The indicator offers extensive customization for line appearance, positioning, and conditional display, including an option to highlight only bullish engulfing patterns.

Key Features:

1. Customizable Line Position:

o Users can choose from various methods to calculate the "centre" price for the line:

(High + Low) / 2 (Default)

(Open + Close) / 2

Close

Open

(Open + High + Low + Close) / 4 (HLCO/4)

(Open + High + Close) / 3 (Typical Price HLC/3 variation)

(Open + Close + Low) / 3 (Typical Price OCL/3 variation)

2. Line Appearance Customization:

o Visibility: Toggle lines on/off.

o Style: Solid, dotted, or dashed lines.

o Width: Adjustable line thickness (1 to 5).

o Length: Defines how many candles forward the line extends (1 to 10).

o Color: Lines are colored based on candle type (bullish/bearish), with user-selectable base colors.

o Dynamic Opacity: Line opacity is dynamically adjusted based on the candle's size relative to recent candles. Larger candles produce more opaque lines (up to the user-defined maximum opacity), while smaller candles result in more transparent lines. This helps significant candles stand out.

3. Price Labels:

o Show Labels: Option to display price labels at the end of each center line.

o Label Background Color: Customizable.

o Dynamic Text Color: Label text color can change based on the movement of the center price:

Green: Current center price is higher than the previous.

Red: Current center price is lower than the previous.

Gray: No change or first label.

o Static Text Color: Alternatively, a fixed color can be used for all labels.

4. Conditional Drawing - Bullish Engulfing Filter:

o Users can enable an option to Only Show Bullish Engulfing Candles. When active, center lines will only be drawn for candles that meet bullish engulfing criteria (current bull candle's body engulfs the previous bear candle's body).

5. Performance Management:

o Max Lines to Show: Limits the number of historical lines displayed on the chart to maintain clarity and performance. Older lines are automatically removed as new ones are drawn.

6. Alert Condition:

o Includes a built-in alert: Big Bullish Candle. This alert triggers when a bullish candle's range (high - low) is greater than the 20-period simple moving average (SMA) of candle ranges.

How It Works:

• For each new candle, the script calculates the "center" price based on the user's Line Position selection.

• If showLines is enabled and (if applicable) the bullish engulfing condition is met, a new line is drawn from the current candle's bar_index at the calculated _center price, extending lineLength candles forward.

• The line's color is determined by whether the candle is bullish (close > open) or bearish (close < open).

• Opacity is calculated dynamically: scaledOpacity = int((100 - maxUserOpacity) * (1 - dynamicFactor) + maxUserOpacity), where dynamicFactor is candleSize / maxSize (current candle size relative to the max size in the last 20 candles). This means maxUserOpacity is the least transparent the line will be (for the largest candles), and smaller candles will have lines approaching full transparency.

• Optional price labels are added at the end of these lines.

• The script manages an array of drawn lines, removing the oldest ones if the maxLines limit is exceeded.

Potential Use Cases:

• Visualizing Intra-Candle Levels: Quickly see midpoints or other key price points without manual drawing.

• Short-Term Reference Points: The extended lines can act as very short-term dynamic support/resistance or points of interest.

• Pattern Recognition: Highlight bullish engulfing patterns or simply emphasize candles based on their calculated center.

• Volatility Indication: The dynamic opacity can subtly indicate periods of larger or smaller candle ranges.

• Confirmation Tool: Use in conjunction with other indicators or trading strategies.

User Input Groups:

• Line Settings: Controls all aspects of the line's appearance and calculation.

• Label Settings: Manages the display and appearance of price labels.

• Other Settings: Contains options for line management and conditional filtering (like Bullish Engulfing).

This indicator provides a clean and customizable way to mark significant price levels within candles, aiding traders in their technical analysis.

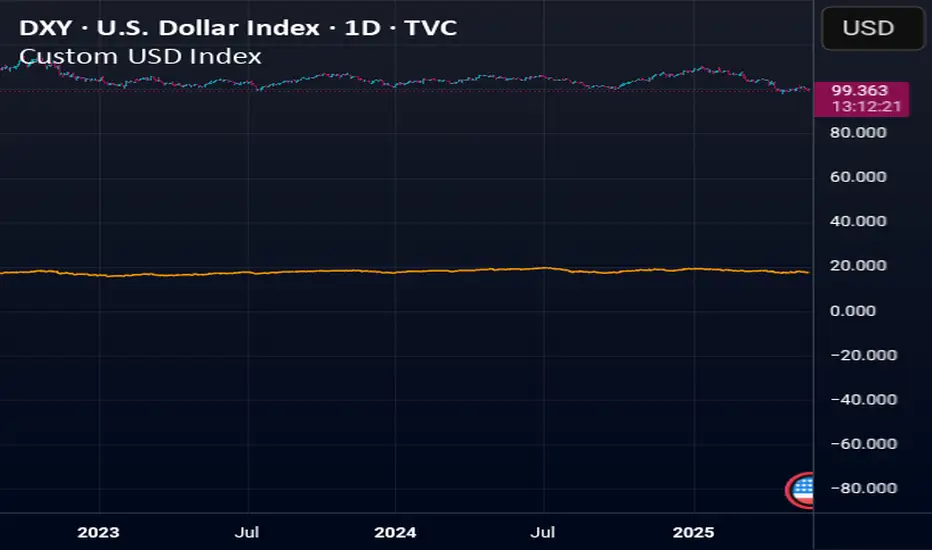

Normalized DXY+Custom USD Index (DXY+) – Normalized Dollar Strength with Bitcoin, Gold, and Yuan.

This custom USD strength index replicates the structure of the official U.S. Dollar Index (DXY), while expanding it to include modern financial assets such as Bitcoin (BTC), Ethereum (ETH), gold (XAU), and the Chinese yuan (CNY).

Weights for the core fiat currencies (EUR, JPY, GBP, CAD, SEK, CHF) follow the official ICE DXY methodology. Additional components are weighted proportionally based on their estimated global economic influence.

The index is normalized from its initial valid data point, meaning it starts at 100 on the first day all asset inputs are available. From that point forward, it tracks the relative strength of the U.S. dollar against this expanded basket.

This provides a more comprehensive and modernized view of the dollar's strength—not only against traditional fiat currencies, but also in the context of rising decentralized assets and non-Western trade power.

H2-25 cuts (bp)This custom TradingView indicator tracks and visualizes the implied pricing of Federal Reserve rate cuts in the market, specifically for the second half of 2025. It does so by comparing the price differences between two specific Fed funds futures contracts: one for June 2025 and one for December 2025. These contracts are traded on the Chicago Board of Trade (CBOT) and are a widely-used market gauge of the expected path of U.S. interest rates.

The indicator calculates the difference between the implied rates for June and December 2025, and then multiplies the result by 100 to express it in basis points (bps). Each 0.01 change in the spread corresponds to a 1-basis point change in expectations for future rate cuts. A positive value indicates that the market is pricing in a higher likelihood of one or more rate cuts in 2025, while a negative value suggests that the market expects the Fed to hold rates steady or even raise them.

The plot represents the difference in implied rate cuts (in basis points) between the two contracts:

June 2025 (ZQM2025): A contract representing the implied Fed funds rate for June 2025.

December 2025 (ZQZ2025): A contract representing the implied Fed funds rate for December 2025.

Custom USD IndexThis is a modernized, expanded version of the U.S. Dollar Index (DXY), designed to provide a more accurate representation of the dollar’s global strength in today’s diversified economy.

Unlike the traditional DXY, which excludes major players like China and entirely omits real-world stores of value, this custom index (DXY+) includes:

Fiat Currencies (78.3% total weight):

EUR, JPY, GBP, CAD, AUD, CHF, and CNY — equally weighted to reflect the global currency landscape.

Gold (17.5%):

Gold (XAUUSD) is included as a traditional reserve asset and inflation hedge, acknowledging its continued monetary relevance.

Cryptocurrencies (2.8% total weight):

Bitcoin (BTC) and Ethereum (ETH) represent the emerging digital monetary layer.

The index rises when the U.S. dollar strengthens relative to this blended basket, and falls when the dollar weakens against it. This is ideal for traders, economists, and macro analysts seeking a more inclusive and up-to-date measure of dollar performance.

Levels & Flow📌 Overview

Levels & Flow is a visual trading tool that combines daily pivot levels with a dynamic EMA ribbon to help traders identify structure, momentum, and key decision zones in the market.

This script is designed for discretionary traders who rely on clean visual cues for intraday and swing trading strategies.

⚙️ Key Features

Daily Pivot, Support, and Resistance Lines

Automatically plots the daily pivot level based on the previous day’s OHLC data, along with calculated support and resistance levels.

Fibonacci Retracement Levels

Two dashed lines above and below the pivot represent the retracement of the pivot-resistance and pivot-support range, forming the boundaries of the “no-trade zone.”

No-Trade Zone (Shaded Box)

A gray shaded box between the two Fibonacci levels to visually mark a high-chop/low-conviction zone.

Trend-Based Candle Coloring (Current Day Only)

Candles are colored green if the close is above the pivot, red if below (only on the current trading day).

Bullish/Bearish Trend Label

A small table in the bottom-right corner displays “Bullish” or “Bearish” depending on whether price is above or below the pivot.

20-EMA Gradient Ribbon

A stack of 20 EMAs, each smoothed and color-coded from blue to green to reflect short- to long-term trend alignment.

Cumulative EMA with Adaptive Weighting

An intelligent moving average line that adjusts weight distribution among the 20 EMAs based on recent predictive accuracy using a learning rate and lookback period.

🧠 How It Works

📍 Levels

The script calculates daily pivot, resistance, and support levels using standard formulas:

Pivot = (High + Low + Close) / 3

Resistance = (2 × Pivot) – Low

Support = (2 × Pivot) – High

These levels update each day and extend 143 bars to the right.

📏 Fib Lines

Fib Up = Pivot + (Resistance – Pivot) × 0.382

Fib Down = Pivot – (Pivot – Support) × 0.382

These lines form the “no-trade zone” box.

📈 EMA Ribbon

20 EMAs starting from the user-defined Base Length, each incremented by 1

Each EMA is smoothed using the Smoothing Period

Color-coded from blue to green for intuitive visual flow

Filled between EMAs to visualize trend strength and alignment

🧠 Cumulative EMA Learning

Each EMA’s historical error is calculated over a Lookback Period

Lower-error EMAs receive higher weight; weights are normalized to sum to 1

The result is a cumulative EMA that adapts based on historical predictive power

🔧 User Inputs

Input

Base EMA Length: Sets the period for the shortest EMA (default: 20)

Smoothing Period: Smooths all EMAs and the cumulative EMA

Lookback for Learning: Number of bars to evaluate EMA prediction accuracy

Learning Rate: Adjusts how quickly weights shift in favor of more accurate EMAs

✅ How to Use It

Use the pivot level to define directional bias.

Watch for price breakouts above resistance or breakdowns below support to consider entry.

Avoid trading inside the shaded zone, where direction is less reliable.

Use the EMA ribbon gradient to confirm short/long alignment.

The cumulative EMA helps define trend with noise reduction.

🧪 Best For

Intraday traders who want to blend structure with flow

Swing traders needing clean daily levels with dynamic confirmation

Anyone looking to avoid choppy zones and improve visual clarity

⚠️ Disclaimer

This script is for educational and informational purposes only. It does not constitute financial advice or a trading recommendation. Always test scripts in simulation or on demo accounts before live use. Use at your own risk.

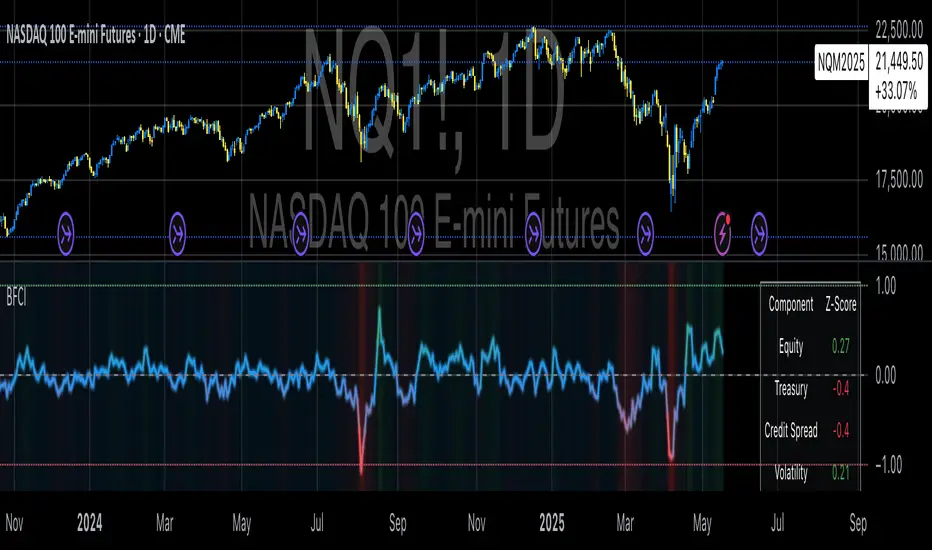

Bloomberg Financial Conditions Index (Proxy)The Bloomberg Financial Conditions Index (BFCI): A Proxy Implementation

Financial conditions indices (FCIs) have become essential tools for economists, policymakers, and market participants seeking to quantify and monitor the overall state of financial markets. Among these measures, the Bloomberg Financial Conditions Index (BFCI) has emerged as a particularly influential metric. Originally developed by Bloomberg L.P., the BFCI provides a comprehensive assessment of stress or ease in financial markets by aggregating various market-based indicators into a single, standardized value (Hatzius et al., 2010).

The original Bloomberg Financial Conditions Index synthesizes approximately 50 different financial market variables, including money market indicators, bond market spreads, equity market valuations, and volatility measures. These variables are normalized using a Z-score methodology, weighted according to their relative importance to overall financial conditions, and then aggregated to produce a composite index (Carlson et al., 2014). The resulting measure is centered around zero, with positive values indicating accommodative financial conditions and negative values representing tighter conditions relative to historical norms.

As Angelopoulou et al. (2014) note, financial conditions indices like the BFCI serve as forward-looking indicators that can signal potential economic developments before they manifest in traditional macroeconomic data. Research by Adrian et al. (2019) demonstrates that deteriorating financial conditions, as measured by indices such as the BFCI, often precede economic downturns by several months, making these indices valuable tools for predicting changes in economic activity.

Proxy Implementation Approach

The implementation presented in this Pine Script indicator represents a proxy of the original Bloomberg Financial Conditions Index, attempting to capture its essential features while acknowledging several significant constraints. Most critically, while the original BFCI incorporates approximately 50 financial variables, this proxy version utilizes only six key market components due to data accessibility limitations within the TradingView platform.

These components include:

Equity market performance (using SPY as a proxy for S&P 500)

Bond market yields (using TLT as a proxy for 20+ year Treasury yields)

Credit spreads (using the ratio between LQD and HYG as a proxy for investment-grade to high-yield spreads)

Market volatility (using VIX directly)

Short-term liquidity conditions (using SHY relative to equity prices as a proxy)

Each component is transformed into a Z-score based on log returns, weighted according to approximated importance (with weights derived from literature on financial conditions indices by Brave and Butters, 2011), and aggregated into a composite measure.

Differences from the Original BFCI

The methodology employed in this proxy differs from the original BFCI in several important ways. First, the variable selection is necessarily limited compared to Bloomberg's comprehensive approach. Second, the proxy relies on ETFs and publicly available indices rather than direct market rates and spreads used in the original. Third, the weighting scheme, while informed by academic literature, is simplified compared to Bloomberg's proprietary methodology, which may employ more sophisticated statistical techniques such as principal component analysis (Kliesen et al., 2012).

These differences mean that while the proxy BFCI captures the general direction and magnitude of financial conditions, it may not perfectly replicate the precision or sensitivity of the original index. As Aramonte et al. (2013) suggest, simplified proxies of financial conditions indices typically capture broad movements in financial conditions but may miss nuanced shifts in specific market segments that more comprehensive indices detect.

Practical Applications and Limitations

Despite these limitations, research by Arregui et al. (2018) indicates that even simplified financial conditions indices constructed from a limited set of variables can provide valuable signals about market stress and future economic activity. The proxy BFCI implemented here still offers significant insight into the relative ease or tightness of financial conditions, particularly during periods of market stress when correlations among financial variables tend to increase (Rey, 2015).

In practical applications, users should interpret this proxy BFCI as a directional indicator rather than an exact replication of Bloomberg's proprietary index. When the index moves substantially into negative territory, it suggests deteriorating financial conditions that may precede economic weakness. Conversely, strongly positive readings indicate unusually accommodative financial conditions that might support economic expansion but potentially also signal excessive risk-taking behavior in markets (López-Salido et al., 2017).

The visual implementation employs a color gradient system that enhances interpretation, with blue representing neutral conditions, green indicating accommodative conditions, and red signaling tightening conditions—a design choice informed by research on optimal data visualization in financial contexts (Few, 2009).

References

Adrian, T., Boyarchenko, N. and Giannone, D. (2019) 'Vulnerable Growth', American Economic Review, 109(4), pp. 1263-1289.

Angelopoulou, E., Balfoussia, H. and Gibson, H. (2014) 'Building a financial conditions index for the euro area and selected euro area countries: what does it tell us about the crisis?', Economic Modelling, 38, pp. 392-403.

Aramonte, S., Rosen, S. and Schindler, J. (2013) 'Assessing and Combining Financial Conditions Indexes', Finance and Economics Discussion Series, Federal Reserve Board, Washington, D.C.

Arregui, N., Elekdag, S., Gelos, G., Lafarguette, R. and Seneviratne, D. (2018) 'Can Countries Manage Their Financial Conditions Amid Globalization?', IMF Working Paper No. 18/15.

Brave, S. and Butters, R. (2011) 'Monitoring financial stability: A financial conditions index approach', Economic Perspectives, Federal Reserve Bank of Chicago, 35(1), pp. 22-43.

Carlson, M., Lewis, K. and Nelson, W. (2014) 'Using policy intervention to identify financial stress', International Journal of Finance & Economics, 19(1), pp. 59-72.

Few, S. (2009) Now You See It: Simple Visualization Techniques for Quantitative Analysis. Analytics Press, Oakland, CA.

Hatzius, J., Hooper, P., Mishkin, F., Schoenholtz, K. and Watson, M. (2010) 'Financial Conditions Indexes: A Fresh Look after the Financial Crisis', NBER Working Paper No. 16150.

Kliesen, K., Owyang, M. and Vermann, E. (2012) 'Disentangling Diverse Measures: A Survey of Financial Stress Indexes', Federal Reserve Bank of St. Louis Review, 94(5), pp. 369-397.

López-Salido, D., Stein, J. and Zakrajšek, E. (2017) 'Credit-Market Sentiment and the Business Cycle', The Quarterly Journal of Economics, 132(3), pp. 1373-1426.

Rey, H. (2015) 'Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence', NBER Working Paper No. 21162.

Aggregated Perpetual Futures Open InterestPurpose

Aggregates perpetual futures open interest across Binance, Bybit, and OKX for the base currency of the asset loaded in your tradingview window.

How It Works

Symbol detection: The script grabs syminfo.basecurrency (e.g., “BTC”) from whatever market is on screen.

Ticker mapping: It constructs the three perp-OI feeds that TradingView publishes in the form EXCHANGE:USDT.P_OI

Data request: For each feed it fetches the full OHLC candle (request.security) on the chart’s timeframe. If a venue doesn’t list that perp, the request simply returns na.

Aggregation: The script adds the opens, highs, lows, and closes of all non-na feeds to produce a single aggregated OI candle.

General Notes

The status line shows each venue’s individual OI close.

FVG Candle HighlighterThis indicator highlights only the true Fair Value Gap (FVG) creator candle — the middle candle in a 3-bar FVG formation — with zero clutter.

🔹 Bullish FVG: Candle is colored if price gaps above the high two bars back

🔹 Bearish FVG: Candle is colored if price gaps below the low two bars back

✨ No boxes. No zones. Just pure, visual price-action accuracy.

🔧 Powered by Pine Script v6

🧠 Based on institutional-style FVG logic

🎯 Ideal for Smart Money / ICT / Order Block strategies

Coinbase Premium IndicatorPurpose

Indicates whether a crypto asset listed on a Coinbase spot market is trading at a premium or discount to other spot (Tether) markets.

How It Works

The script takes the base currency for the pair loaded in that TradingView window and searches for its Coinbase spot market. It also maps the base currency to the USDT (Tether) spot markets on Binance, Bybit, and OKX.

The Premium/ Discount is: (coin-btc-usd) - (sum(bnce-btc-usdt, bybt-btc-usdt, okx-btc-usdt))

General Notes

The status line of the Indicator displays the value of the premium/ discount and the market prices of the pair for each constituent exchange.

PER x RangeThis Pine Script calculates the target price of the Nikkei Average based on the EPS (Earnings Per Share) and different PER (Price-to-Earnings Ratio) multiples ranging from 17.5x to 12x, in increments of 0.5x. It then plots these target prices on the chart.

Key Features:

Input EPS: You can manually input the current EPS value of the Nikkei Average (the example uses 2380, but you can replace it with the actual EPS).

PER Multiples Calculation: The script calculates target prices for different PER multiples (17.5x, 17x, 16.5x, ..., down to 12x).

Plotting Target Prices: The calculated target prices (EPS * PER) are plotted on the chart as blue lines, showing you different target price scenarios based on varying PER multiples.