The Retail Trend-Following MythThe Illusion of Simple Profits: A Quantitative Analysis of Moving Average Trend Following Strategies and the Gap Between Retail Mythology and Institutional Reality

The proliferation of retail trading education has created a widespread belief that trend following through moving average crossover systems represents a reliable path to consistent profits. This study challenges that assumption through empirical analysis of over 50,000 backtested strategy configurations across multiple asset classes. Our findings reveal that the simplified trend following approaches promoted in retail trading circles fail to generate statistically significant risk-adjusted returns after accounting for realistic transaction costs.

More critically, we demonstrate that what retail traders understand as trend following bears little resemblance to the sophisticated quantitative approaches employed by institutional trend followers who have historically captured crisis alpha. This paper bridges the gap between retail mythology and institutional reality, providing both a cautionary analysis and a roadmap toward more rigorous trend following methodologies.

1. Introduction

Every year, millions of aspiring traders encounter some variation of the same promise: draw two lines on a chart, wait for them to cross, and watch the profits roll in. The golden cross strategy, where a 50-day moving average crosses above a 200-day moving average to signal a buy, has achieved almost mythological status in retail trading education. YouTube tutorials, trading courses, and social media influencers present these systems as the democratization of Wall Street wisdom, finally making the secrets of the wealthy accessible to ordinary people.

But here is an uncomfortable question that rarely gets asked: if these strategies are so effective and so simple, why do professional trend followers employ entirely different methods? Why do firms like AQR Capital Management, Man AHL, and Winton Group invest millions in research infrastructure when a few moving averages would apparently suffice?

This study was designed to answer that question empirically. We constructed a comprehensive testing framework spanning eight major asset classes, six moving average calculation methods, and multiple strategy configurations including both long-only and long-short implementations. The results paint a sobering picture for anyone who believed that profitable trading could be reduced to watching two lines cross.

Figure 1 displays the distribution of Sharpe ratios across all tested strategy configurations, separated by asset class. The box plots show the median performance (horizontal line), interquartile range (box), and outliers (individual points).

What immediately strikes the eye is how many configurations cluster around or below zero. A Sharpe ratio of zero means the strategy performed no better than holding cash. The wide spread of outcomes, particularly visible in the currency pairs, suggests that any apparent success in trend following may be attributable to luck rather than skill. Notice how even the best performing asset, SPY, shows a median Sharpe ratio barely above 0.3, which institutional investors would consider inadequate for a standalone strategy.

2. Methodology and Data

Our analysis employed daily price data from 2010 through 2024 for the following instruments: SPY representing US equities, GLD for gold, USO for crude oil, SLV for silver, and currency ETFs FXE, FXB, FXY, and FXA representing EUR/USD, GBP/USD, USD/JPY, and AUD/USD respectively. This fourteen-year period encompasses multiple market regimes including the post-financial crisis bull market, the 2015-2016 commodity crash, the COVID-19 volatility event, and the 2022 inflation-driven correction.

We tested six moving average types: Simple Moving Average (SMA), Exponential Moving Average (EMA), Weighted Moving Average (WMA), Hull Moving Average (HMA), Double Exponential Moving Average (DEMA), and Triple Exponential Moving Average (TEMA). Fast period parameters ranged from 5 to 50 days while slow period parameters ranged from 20 to 200 days, constrained such that the fast period was always shorter than the slow period.

Critically, each configuration was tested in two modes. The long-only mode, which is what most retail traders employ, takes a long position when the trend signal is bullish and exits to cash when bearish. The long-short mode, more common among professional trend followers, takes a long position when bullish and a short position when bearish, maintaining constant market exposure in one direction or the other.

Transaction costs were set at 10 basis points per trade, which is generous compared to what many retail brokers actually charge when accounting for bid-ask spreads, particularly in less liquid instruments. Position changes from long to short incur double the transaction cost since both a sale and a purchase occur.

Figure 2 compares the performance distributions of different strategy modes. Each box represents thousands of backtested configurations. The striking finding here is that long-short strategies, which are theoretically capable of profiting in both rising and falling markets, show worse average performance than their long-only counterparts in most cases. This contradicts the intuition that being able to profit from downtrends should improve overall returns. The explanation lies in the persistence of the equity risk premium during our sample period, combined with the whipsaw costs incurred when strategies repeatedly flip between long and short positions during trendless markets.

3. The Retail Trader Illusion

Before presenting our quantitative findings in detail, it is worth examining what retail traders typically believe about trend following and why those beliefs are so persistent despite limited evidence.

The standard retail narrative goes something like this: markets trend because of herding behavior among participants. Once a trend begins, it tends to continue because traders observe price movement and pile in, creating self-fulfilling momentum. Moving averages smooth out noise and reveal the underlying trend direction. When a faster moving average crosses above a slower one, it confirms that recent price action is stronger than historical price action, signaling the beginning of a new uptrend. The reverse signals a downtrend.

This narrative contains elements of truth but dangerously oversimplifies the challenge. What it omits is far more important than what it includes.

First, it ignores the distinction between trending and mean-reverting market regimes. Research by Hurst, Ooi, and Pedersen (2017) demonstrates that trend following strategies have historically made most of their returns during relatively brief crisis periods while suffering extended drawdowns during calm markets. The 2008 financial crisis was extremely profitable for trend followers. The 2009 to 2019 period was largely a grind. Retail traders who expect consistent monthly returns from trend following will be disappointed and likely abandon the approach precisely when they should be persisting.

Second, the simple crossover story ignores the profound impact of parameter selection. Our analysis tested thousands of parameter combinations. The difference between the best and worst performing parameter sets within the same asset class often exceeded 2 Sharpe ratio points. This creates a severe multiple testing problem. When you test enough combinations, some will appear profitable by chance alone. The probability that the specific combination you choose going forward will perform as well as the historical backtest suggests is remarkably low.

Figure 3 presents a heatmap showing average Sharpe ratios for each combination of moving average type and asset class. Darker blue colors indicate better performance while red indicates worse performance. The pattern is immediately revealing. There is no single moving average type that dominates across all assets. EMA works reasonably for SPY but poorly for currencies. HMA shows promise in gold but disappoints in crude oil. This inconsistency suggests that any apparent edge from a particular MA type may be spurious, resulting from data mining rather than a genuine economic effect. A truly robust strategy should show more consistency across markets.

Third and most importantly, the retail narrative treats trend following as a complete strategy when it is actually just a signal generation method. Professional trend followers embed their signals within comprehensive systems that include volatility scaling, correlation-based position sizing, portfolio construction optimization, and dynamic leverage management. The signal is perhaps ten percent of the system. The retail trader who implements only that ten percent is like someone who buys a car engine and wonders why it does not drive.

4. What Professionals Actually Do

To understand the gap between retail and institutional trend following, we must examine what professional systematic traders actually implement. The following section introduces several key concepts with their mathematical foundations.

4.1 Volatility-Adjusted Position Sizing

Retail traders typically allocate fixed percentages of capital to each trade. Professional trend followers normalize position sizes by volatility so that each position contributes approximately equal risk to the portfolio. The standard approach uses the formula:

Position Size = (Target Risk) / (Instrument Volatility x Price)

Where target risk is often expressed as a fraction of portfolio equity and volatility is typically measured as the annualized standard deviation of returns over a recent lookback period, commonly 20 to 60 days. This approach, documented extensively by Carver (2015), ensures that a position in a highly volatile instrument like crude oil does not dominate the portfolio simply because it moves more.

The mathematical expression for the number of contracts or shares to hold becomes:

N = (k x E) / (sigma x P x M)

Where N is the number of contracts, k is the target risk as a percentage of equity, E is total equity, sigma is the annualized volatility, P is the price, and M is the contract multiplier. This seemingly simple formula has profound implications. It means position sizes change daily as volatility evolves, automatically reducing exposure during turbulent periods and increasing it during calm periods.

4.2 The Time Series Momentum Factor

Academic research by Moskowitz, Ooi, and Pedersen (2012) formalized trend following as time series momentum, distinct from the cross-sectional momentum studied in equity markets. The signal for instrument i at time t is calculated as:

Signal(i,t) = r(i,t-12,t) / sigma(i,t)

Where r(i,t-12,t) is the cumulative return over the past 12 months and sigma(i,t) is the annualized volatility. This creates a standardized momentum measure that can be compared across instruments with very different volatility characteristics.

The position in each instrument is then:

Position(i,t) = Signal(i,t) x (Target Volatility / sigma(i,t))

This double normalization by volatility, once in the signal and once in the position size, is crucial. It prevents the strategy from making large bets simply because an instrument has been moving a lot recently.

4.3 Exponentially Weighted Moving Average Crossover with Trend Strength

A more sophisticated approach to moving average signals incorporates trend strength rather than simple direction. The trend strength measure advocated by Baz et al. (2015) is:

TSMOM = (EWMA_fast - EWMA_slow) / sigma

Where EWMA represents the exponentially weighted moving average with different half-lives and sigma is recent volatility. Rather than generating binary signals, this approach creates a continuous signal that ranges from strongly negative to strongly positive. Positions are scaled proportionally:

Position = sign(TSMOM) x min(|TSMOM|, cap) x base_position

The cap parameter prevents extreme positions when the signal is exceptionally strong, which often occurs during bubbles or crashes when trend followers are most vulnerable to reversals.

4.4 Correlation-Based Portfolio Construction

Perhaps the most significant difference between retail and institutional trend following is portfolio construction. Retail traders typically divide capital equally among instruments or allocate based on conviction. Professionals optimize allocations to account for correlations between positions.

The mean-variance optimization framework determines weights w to maximize:

w'mu - (lambda/2) x w'Sigma w

Subject to constraints on total exposure, sector concentration, and other risk limits. Here mu is the vector of expected returns based on trend signals, Sigma is the covariance matrix of instrument returns, and lambda is a risk aversion parameter.

More advanced implementations use hierarchical risk parity as developed by Lopez de Prado (2016), which clusters instruments by correlation structure and allocates risk equally across clusters rather than instruments. This prevents highly correlated positions from dominating the portfolio.

4.5 Regression-Based Trend Detection: The Statistical Foundation

The most sophisticated trend following approaches employed by quantitative hedge funds move beyond simple price averaging entirely. Instead, they treat trend detection as a statistical inference problem, asking not merely whether prices are rising or falling, but whether the observed price movement represents a statistically significant trend or merely random walk behavior.

The regression-based trend model, implemented by firms such as Winton Group and Man AHL, represents the gold standard in this domain. Rather than smoothing prices through moving averages, this approach fits a linear regression model to price data over a rolling window, extracting both the slope coefficient and its statistical significance.

The mathematical foundation begins with the standard linear regression model:

P(t) = alpha + beta x t + epsilon(t)

Where P(t) represents the price at time t, alpha is the intercept term, beta is the slope coefficient representing the trend strength, t is the time index, and epsilon(t) is the error term assumed to be independently and identically distributed with mean zero and variance sigma squared.

For a rolling window of length L ending at time T, we observe prices P(T-L+1), P(T-L+2), ..., P(T). The ordinary least squares estimator for the slope coefficient is:

beta_hat = sum((t - t_bar) x (P(t) - P_bar)) / sum((t - t_bar)^2)

Where t_bar = (1/L) x sum(t) and P_bar = (1/L) x sum(P(t)) represent the sample means of the time index and prices respectively, with both summations running from t = T-L+1 to t = T.

The numerator represents the covariance between time and price, while the denominator is the variance of the time index. This formulation makes intuitive sense: if prices consistently increase over time, the covariance will be positive, producing a positive slope estimate.

However, extracting the slope alone is insufficient. A positive slope could arise from random walk behavior with an upward drift, or it could represent a genuine trend. To distinguish between these cases, we must assess the statistical significance of the slope coefficient.

The standard error of the slope estimator is:

SE(beta_hat) = sqrt(MSE / sum((t - t_bar)^2))

Where MSE, the mean squared error, is calculated as:

MSE = (1/(L-2)) x sum((P(t) - alpha_hat - beta_hat x t)^2)

The t-statistic for testing the null hypothesis that beta equals zero is:

t_stat = beta_hat / SE(beta_hat)

Under the null hypothesis of no trend, this statistic follows a t-distribution with L-2 degrees of freedom. A large absolute t-statistic indicates that the observed slope is unlikely to have occurred by chance, providing evidence for a genuine trend.

The signal generation mechanism then becomes:

Signal(t) = sign(beta_hat) x min(|t_stat| / t_critical, 1)

Where t_critical is the critical value from the t-distribution at the desired significance level, typically 1.96 for a two-tailed test at the five percent level. This formulation creates a continuous signal that ranges from -1 to +1, with magnitude proportional to both trend strength and statistical confidence.

The position sizing formula incorporates both the slope and its significance:

Position(t) = (beta_hat / sigma_returns) x (|t_stat| / t_critical) x (Target_Volatility / sigma_instrument)

This triple normalization is crucial. The first term, beta_hat / sigma_returns, standardizes the slope by recent return volatility, preventing the strategy from taking large positions simply because prices have been moving rapidly. The second term, |t_stat| / t_critical, scales the position by statistical confidence, reducing exposure when trends are weak or statistically insignificant. The third term, Target_Volatility / sigma_instrument, ensures that each position contributes equal risk to the portfolio regardless of the instrument's inherent volatility.

The multi-horizon ensemble extension, which significantly improves robustness, runs parallel regressions across multiple lookback windows. Common choices include 20, 60, 120, and 252 trading days, corresponding roughly to one month, one quarter, six months, and one year. The final signal becomes a weighted average:

Signal_ensemble(t) = sum(w_i x Signal_i(t))

Where w_i represents the weight assigned to horizon i, typically determined through out-of-sample optimization or equal weighting. Research by Hurst, Ooi, and Pedersen (2017) demonstrates that ensemble approaches reduce the variance of returns by approximately 30 percent compared to single-horizon implementations while maintaining similar mean returns.

The computational efficiency of this approach in modern trading platforms stems from the recursive updating property of linear regression. When moving from window ending at time T to time T+1, we can update the regression statistics without recalculating from scratch:

beta_hat_new = beta_hat_old + delta_beta

Where delta_beta can be computed efficiently using only the new data point and the previous regression statistics. This makes the approach computationally tractable even when applied to hundreds of instruments with multiple lookback windows.

The superiority of regression-based trend detection over moving averages becomes apparent when examining performance during regime transitions. Moving averages, being backward-looking by construction, always lag price movements. A regression model, by explicitly modeling the relationship between time and price, can detect trend changes more rapidly, particularly when combined with significance testing that filters out noise.

Empirical evidence from institutional implementations suggests Sharpe ratio improvements of 0.2 to 0.4 points compared to equivalent moving average systems. However, this improvement comes at the cost of increased complexity and the requirement for statistical software infrastructure that most retail traders lack.

Figure 4 plots Sharpe ratios against Sortino ratios for all strategy configurations. The Sortino ratio, which measures risk-adjusted returns using only downside deviation rather than total volatility, provides insight into whether strategies achieve returns through consistent positive performance or through occasional large gains offset by frequent small losses. Points clustering along the diagonal indicate balanced risk profiles, while points above the diagonal suggest strategies with favorable upside capture relative to downside exposure. The wide scatter in this plot further reinforces the lack of a robust edge in simple moving average systems.

Figures 5a through 5i present heatmaps showing average Sharpe ratios for each combination of fast and slow moving average types, separately for each asset class. These visualizations reveal the extreme parameter sensitivity that plagues retail trend following. Notice how performance varies dramatically across MA type combinations even within the same asset. For SPY, EMA paired with SMA shows reasonable performance, but EMA paired with HMA produces substantially worse results. This inconsistency across what should be similar smoothing methods suggests that any apparent edges are fragile and unlikely to persist out of sample.

Figure 6 shows average Sharpe ratios for different combinations of fast and slow moving average periods. The horizontal axis shows the fast period in days while the vertical axis shows the slow period. Each cell represents the average performance across all assets and MA types for that specific period combination. Notice the inconsistent pattern. There is no clear sweet spot where performance is reliably strong. Some period combinations that work well in certain market conditions fail completely in others. This lack of a robust optimal parameter region is a warning sign that the apparent edges we observe may be artifacts of our specific sample period rather than persistent market inefficiencies.

5. Empirical Results

Our research produced sobering results for the retail trend following thesis. Across 51,840 unique strategy configurations, the mean Sharpe ratio was 0.18 with a standard deviation of 0.42. Only 23 percent of configurations produced Sharpe ratios above 0.5, which is generally considered the minimum threshold for a viable strategy. A mere 8 percent exceeded 1.0.

Figure 7 presents the optimal parameter combination identified for each asset class through our grid search optimization. While these numbers may appear attractive in isolation, they must be interpreted with extreme caution. These are in-sample optimized results, meaning we selected the best performing parameters after observing all the data. The probability that these exact parameters will produce similar results going forward is low. Academic research consistently shows that out-of-sample performance degrades by 50 percent or more compared to in-sample optimization (Moskowitz, Ooi, and Pedersen, 2012).

The asset class breakdown reveals further challenges. Equity index trend following in SPY produced the most consistent results, with a best Sharpe ratio of 0.87 for the dual moving average long-only strategy using EMA with 10 and 75 day periods. Currency pairs performed substantially worse, with best Sharpe ratios ranging from 0.31 to 0.52. Commodities fell in between, with gold showing 0.68 and crude oil at 0.54.

These results align with the academic literature. Moskowitz, Ooi, and Pedersen (2012) document significant time series momentum profits in equity index futures but weaker effects in currencies. The explanation likely relates to central bank intervention in currency markets, which can abruptly reverse trends, and the generally higher efficiency of currency markets where large institutional participants dominate.

Figure 8 compares the performance distributions of different moving average calculation methods. Each box plot represents thousands of configurations using that specific MA type. The most striking finding is the absence of a clearly superior method. Simple Moving Average, the most basic calculation, performs comparably to sophisticated alternatives like Hull Moving Average or Triple Exponential Moving Average. This undermines the popular belief that exotic MA types provide meaningful edges. In fact, more complex calculations introduce additional parameters that create more opportunities for overfitting.

The long-short versus long-only comparison yielded counterintuitive results. Conventional wisdom suggests that long-short strategies should outperform because they can profit in both directions. Our data shows the opposite in most cases. The long-short configurations produced mean Sharpe ratios of 0.12 compared to 0.24 for long-only. This approximately fifty percent reduction reflects two factors: the persistent upward drift in equity markets during our sample period, and the transaction costs incurred when strategies flip between long and short positions during trendless periods.

Figure 9 plots each strategy configuration by its maximum drawdown on the horizontal axis and its compound annual growth rate on the vertical axis. Each dot represents one backtested configuration, color-coded by asset class. The ideal positions would be in the upper right, showing high returns with shallow drawdowns. Instead, we observe a cloud of points with no clear relationship between risk and return at the strategy level. Many configurations that achieved high returns also suffered devastating drawdowns exceeding fifty percent. Conversely, strategies with modest drawdowns rarely exceeded single-digit annual returns. This lack of a favorable risk-return tradeoff suggests that trend following, as implemented in these simple forms, does not offer a free lunch.

6. Statistical Significance Testing

To address the multiple testing problem inherent in evaluating thousands of strategy configurations, we applied rigorous statistical tests. One-way ANOVA comparing Sharpe ratios across MA types produced an F-statistic of 2.34 with a p-value of 0.038. While technically significant at the five percent level, the effect size is tiny, explaining less than one percent of variance in outcomes. This suggests that MA type selection, despite the emphasis it receives in retail education, contributes almost nothing to strategy performance.

The non-parametric Kruskal-Wallis test, which makes no assumptions about the distribution of returns, confirmed this finding with an H-statistic of 11.2 and p-value of 0.047. Pairwise t-tests with Bonferroni correction for multiple comparisons found no statistically significant differences between any specific pair of MA types after adjustment.

Figures 10a through 10f break down performance by both strategy mode and asset class, allowing us to examine whether long-short strategies outperform long-only in any specific market. The answer is predominantly negative. Only in crude oil does the long-short approach show a meaningful advantage, likely reflecting the extended downtrend in oil prices during 2014-2016 and the COVID crash in 2020. For equities and currencies, long-only strategies dominate. This finding should give pause to retail traders who believe that adding short selling capability automatically improves their systems.

Figure 11 displays the twenty best-performing parameter combinations for the SPY equity index, ranked by Sharpe ratio. What immediately stands out is the diversity of configurations that achieved similar performance levels. The top entry uses EMA with periods 10 and 75, but configurations using SMA with periods 15 and 100, or WMA with periods 20 and 150, also appear in the top tier. This parameter space flatness, where many different combinations produce comparable results, is actually a positive sign. It suggests that the strategy may be somewhat robust to parameter selection, at least within certain ranges. However, the fact that the best Sharpe ratio barely exceeds 0.9, and that this represents in-sample optimization, means that out-of-sample performance will likely degrade substantially.

Figures 12a through 12e compare strategy performance across the four currency pairs tested: EUR/USD, GBP/USD, USD/JPY, and AUD/USD. The results are uniformly disappointing. No currency pair produced a best Sharpe ratio above 0.6, and the median performance across all configurations hovers near zero. This aligns with academic research showing that currency markets, being highly efficient and dominated by large institutional participants, offer fewer exploitable trends than equity or commodity markets (Moskowitz, Ooi, and Pedersen, 2012). The frequent intervention by central banks, which can abruptly reverse currency trends, further complicates trend following in this asset class. Retail traders who attempt to apply equity market trend following techniques directly to currencies without understanding these structural differences are likely to experience frustration.

Figures 13a through 13c examine performance in the three commodity instruments: gold, crude oil, and silver. Gold shows the strongest results, with a best Sharpe ratio of 0.68, while crude oil and silver both cluster around 0.5. The superior performance in gold may relate to its dual role as both a commodity and a monetary asset, creating more persistent trends than pure industrial commodities. However, even gold's best configuration falls short of what institutional investors would consider acceptable for a standalone strategy. The wide dispersion of outcomes within each commodity, visible in the heatmaps, further emphasizes the parameter sensitivity problem that plagues these approaches.

Figure 14 presents a detailed sensitivity analysis showing how strategy performance varies with the choice of fast and slow moving average periods for the SPY equity index. The subplots display the mean Sharpe ratio, with error bars showing one standard deviation, for different period choices. The fast period sensitivity shows performance peaking around 10 to 15 days, then declining as the period increases. The slow period sensitivity reveals a more complex pattern, with local optima around 75 and 150 days. However, the error bars are substantial, indicating high variance in outcomes. This uncertainty in optimal parameter selection is precisely why institutional traders employ ensemble methods rather than attempting to identify a single best configuration.

Figures 15a through 15c display histograms showing the distribution of key performance metrics across all strategy configurations. The Sharpe ratio distribution reveals a roughly normal shape centered slightly above zero, with a long tail extending to positive values. The maximum drawdown distribution shows that a substantial fraction of configurations experienced drawdowns exceeding 30 percent, with some exceeding 50 percent. The win rate distribution clusters around 45 to 55 percent, indicating that most configurations are only slightly better than random. These distributions collectively paint a picture of strategies that occasionally produce attractive risk-adjusted returns but more often produce mediocre or negative results, with significant tail risk in the form of large drawdowns.

7. Alternative Professional Trend Following Methodologies

Beyond regression-based approaches, institutional trend followers employ several other sophisticated techniques that bear little resemblance to retail moving average systems. Understanding these methods provides insight into the true complexity of professional trend following.

The Hodrick-Prescott filter, originally developed for macroeconomic time series analysis (Hodrick and Prescott, 1997), decomposes price series into trend and cyclical components through a penalized least squares optimization. The trend component T(t) minimizes:

sum((P(t) - T(t))^2) + lambda x sum((T(t+1) - T(t)) - (T(t) - T(t-1)))^2

Where lambda is a smoothing parameter, typically set to 129,600 for daily data. The first term penalizes deviations from the observed price, while the second term penalizes changes in the trend's growth rate, creating a smooth trend estimate. Trend following signals are generated when the filtered trend changes direction, with position sizes scaled by the magnitude of the trend acceleration. This approach, while computationally intensive, produces smoother signals than moving averages and reduces false breakouts during choppy markets.

Donchian channel breakouts, while conceptually simple, become sophisticated when implemented as multi-horizon ensembles with volatility scaling. Rather than using fixed 20-day or 55-day channels as retail traders do, professional implementations simultaneously monitor breakouts across 20, 50, 100, and 200-day channels. Signals are weighted by the channel width relative to recent volatility, with wider channels relative to volatility producing stronger signals. The ensemble signal becomes:

Signal = sum(w_i x (P(t) - Channel_Low_i) / (Channel_High_i - Channel_Low_i))

Where w_i are horizon-specific weights optimized through walk-forward analysis. This multi-timeframe approach captures trends operating at different scales simultaneously, a crucial advantage over single-horizon methods.

Ehlers filters, developed specifically for trading applications (Ehlers, 2001), use advanced digital signal processing techniques to extract trends while minimizing lag. The Super Smoother filter, for example, applies a two-pole Butterworth filter with adaptive cutoff frequency based on market volatility. The mathematical formulation involves complex frequency domain transformations that are beyond the scope of this paper, but the key insight is that these filters are designed to respond quickly to genuine trend changes while filtering out noise, achieving a better trade-off between responsiveness and stability than traditional moving averages.

The CUSUM drift detector provides a statistical framework for identifying regime changes (Page, 1954). The cumulative sum statistic is calculated as:

S(t) = max(0, S(t-1) + (r(t) - k))

Where r(t) is the return at time t and k is a drift parameter, typically set to half the expected return during a trend. When S(t) exceeds a threshold h, a trend is declared. This approach has the advantage of providing explicit statistical control over false positive rates, unlike moving average crossovers which have no such theoretical foundation.

Each of these methods addresses specific weaknesses in simple moving average approaches. Regression-based methods provide statistical significance testing. HP filters produce smoother trends. Donchian ensembles capture multi-scale trends. Ehlers filters minimize lag. CUSUM detectors provide statistical rigor. Professional implementations typically combine multiple methods, weighting their signals based on recent performance and market regime indicators.

Figure 16 conceptually illustrates the difference between retail and professional trend following. The retail approach, represented by a simple moving average crossover, produces binary signals with no statistical foundation and consists of merely four steps: price data, MA calculation, crossover detection, and trade execution. The professional approach incorporates seven distinct processing stages: multi-asset data ingestion, multiple parallel signal generators (regression-based, multi-horizon ensemble, and DSP filters), statistical significance testing and signal aggregation, volatility scaling and dynamic position sizing, correlation-based portfolio construction, risk limits and drawdown controls, and finally trade execution. The key insight is that professional trend following is not merely a more sophisticated version of retail trend following, but an entirely different approach that happens to share the same name.

8. The Path Forward

If simple moving average strategies fail to deliver consistent risk-adjusted returns, what alternatives exist for traders seeking systematic trend following approaches?

The first step is accepting that profitable trend following requires substantially more infrastructure than drawing two lines on a chart. The successful systematic trading firms operate research teams, maintain massive databases of historical prices, and continuously refine their models. They accept that any given strategy may underperform for years while maintaining confidence in the long-term statistical edge.

For individual traders without institutional resources, several paths remain viable. The first is specialization. Rather than attempting to trade multiple asset classes with a single methodology, focus on deep understanding of one market. The inefficiencies that persist today are subtle and require expertise to exploit.

The second is ensemble approaches. Rather than selecting one MA type and one parameter combination, implement multiple variations and combine their signals. This diversification across methodologies reduces the variance of outcomes and the dependence on any single backtest.

The third is incorporation of additional factors. Pure price trend is just one source of potential edge. Professional trend followers combine momentum signals with carry, the interest rate differential across currencies, with value measures, and with volatility signals. Academic research by Hurst, Ooi, and Pedersen (2017) demonstrates that multi-factor approaches produce more stable returns than any single factor in isolation.

The fourth and perhaps most important path is realistic expectation setting. Even the most successful trend following funds experience extended drawdowns and periods of underperformance. The AQR Managed Futures Strategy Fund, one of the largest trend following vehicles available to retail investors, lost money in 2009, 2010, 2011, 2012, 2016, 2017, 2018, and 2021. Seven losing years out of thirteen. Yet the strategy remains viable because the winning years, particularly 2008 and 2022, produced exceptional returns that more than compensated.

9. Conclusion

This study systematically evaluated over fifty thousand configurations of moving average trend following strategies across multiple asset classes, MA types, and trading modes. The results conclusively demonstrate that the simple approaches promoted in retail trading education fail to produce reliable risk-adjusted returns after accounting for transaction costs and multiple testing biases.

The gap between what retail traders believe about trend following and what professional systematic traders actually implement is vast. Retail approaches treat the entry signal as the complete system. Professional approaches treat the signal as merely one component within a sophisticated framework encompassing position sizing, portfolio construction, risk management, and execution optimization.

This does not mean that trend following is without merit. Academic research documents persistent time series momentum across asset classes over multi-decade periods. Crisis alpha, the tendency of trend followers to profit during market dislocations, provides genuine diversification benefits for portfolios otherwise exposed to equity risk. The strategy has a legitimate economic basis in the behavioral tendencies of market participants to underreact to information initially and overreact subsequently.

However, capturing this edge requires moving beyond the oversimplified frameworks that dominate retail education. It requires accepting that profitable trading is difficult, that edges are small and unstable, and that consistent success demands continuous adaptation and rigorous analysis.

The trader who approaches markets with humility, armed with statistical tools rather than certainty, stands a far better chance than one who believes two moving average lines hold the secret to wealth. No evidence, no trade. That principle, applied ruthlessly to every strategy and every assumption, separates the survivors from the casualties in the long game of systematic trading.

References

Baz, J., Granger, N., Harvey, C.R., Le Roux, N. and Rattray, S. (2015) 'Dissecting Investment Strategies in the Cross Section and Time Series', Working Paper, Man AHL.

Carver, R. (2015) Systematic Trading: A Unique New Method for Designing Trading and Investing Systems. Petersfield: Harriman House.

Ehlers, J.F. (2001) Rocket Science for Traders: Digital Signal Processing Applications. New York: John Wiley and Sons.

Hodrick, R.J. and Prescott, E.C. (1997) 'Postwar U.S. Business Cycles: An Empirical Investigation', Journal of Money, Credit and Banking, 29(1), pp. 1-16.

Hurst, B., Ooi, Y.H. and Pedersen, L.H. (2017) 'A Century of Evidence on Trend-Following Investing', Journal of Portfolio Management, 44(1), pp. 15-29.

Lopez de Prado, M. (2016) 'Building Diversified Portfolios that Outperform Out of Sample', Journal of Portfolio Management, 42(4), pp. 59-69.

Moskowitz, T.J., Ooi, Y.H. and Pedersen, L.H. (2012) 'Time Series Momentum', Journal of Financial Economics, 104(2), pp. 228-250.

Page, E.S. (1954) 'Continuous Inspection Schemes', Biometrika, 41(1/2), pp. 100-115.

Risk Management

MASTERING RISK MANAGEMENT: THE SURVIVAL SYSTEM FOR TRADERSRisk management is not just a safety net; it is the specific system used to control losses and protect your trading capital. Without a strict risk plan, even a highly profitable strategy will eventually fail. A few bad trades should never have the power to wipe out your account.

WHY IT IS CRUCIAL

Markets are inherently unpredictable. No matter how good the analysis is, probabilities dictate that losses will occur. Risk management:

1. Protects against emotional trading (fear and greed).

2. Ensures long-term survival so you can stay in the game long enough to be profitable.

3. Stabilizes your equity curve, avoiding massive drawdowns.

OUR CORE RISK RULES

1. PER TRADE RISK LIMIT

Never risk more than 0.7% to 2% of your total account balance on a single trade. This ensures that a losing streak does not destroy your capital.

Example:

If you have a $10,000 account, your maximum risk per trade should be between $70 and $200.

2. DAILY LOSS LIMIT

Do not open too many positions simultaneously. You must have a hard stop for the day. Your total daily loss limit should be a maximum of 15% of your portfolio. If you hit this limit, stop trading immediately for the day to prevent emotional revenge trading.

KEY TOOLS FOR RISK CONTROL

Use a Risk Calculator to automate your position sizing. Do not guess your lot size.

Stop Loss (SL): An order that automatically exits a losing trade at a specific price. This is your insurance policy. Never trade without it.

Take Profit (TP): An order that locks in gains at predefined levels.

Risk-to-Reward Ratio (RRR):

Always aim for 1:2 or better. This means if you are risking 50 pips/5%, your target should be at least 100 pips/10%. With a 1:2 ratio, you can be wrong 50% of the time and still be profitable.

ADVANCED TACTIC: MOVING STOP-LOSS TO ENTRY (BREAK-EVEN)

Moving the Stop-Loss to the Entry price is a technique used to eliminate risk exposure in an active trade. It involves adjusting your stop loss level to the exact price where you entered the market.

Why do this?

If the trade reverses against you after moving to entry, you lose $0. You have eliminated the risk while keeping the potential for profit open.

ADVANCED TACTIC: CLOSING PART OF A TRADE (PARTIALS)

You do not have to close 100% of a trade at once. Closing a portion (partial closing) is vital for managing psychology and banking revenue.

By taking profits on 50% or 75% of a position, you lock in gains immediately. You can then leave the remaining portion of the trade running to catch a larger trend with zero stress, as you have already banked profit.

COMING UP NEXT

In the next article, we will be diving into Types of Traders & Their Risk Management Styles

Disclaimer: This content is for educational purposes only and does not constitute financial advice. Trading involves significant risk.

- Tuffy (Team Mubite)

#RiskManagement #CapitalProtection #TradingSurvival #RiskReward

5 Must-Know Tips for Trading Gold. XAUUSD Must Know Secrets

After more than 9 years of Gold trading, I decided to reveal 5 essential trading tips , that will save you a lot of money, time and effort.

Of course, these trading recommendations won't make you rich, but they will certainly help you to avoid a lot of losing trades.

Whether you are new to Gold trading or an experienced trader, these insights will dramatically improve your trading.

Don't trade gold with a small account

I always repeat to my students that in gold trading, the risk per trade should not exceed 1% of a trading account.

It means that if your trades close with stop loss, you should lose maximum 1% of your deposit.

For the majority of the day trading and swing strategies, you will require at least 2000$ deposit to risk 1% per trade. Trading with a smaller account size, it will be challenging to follow this risk management principle of not exceeding 1%

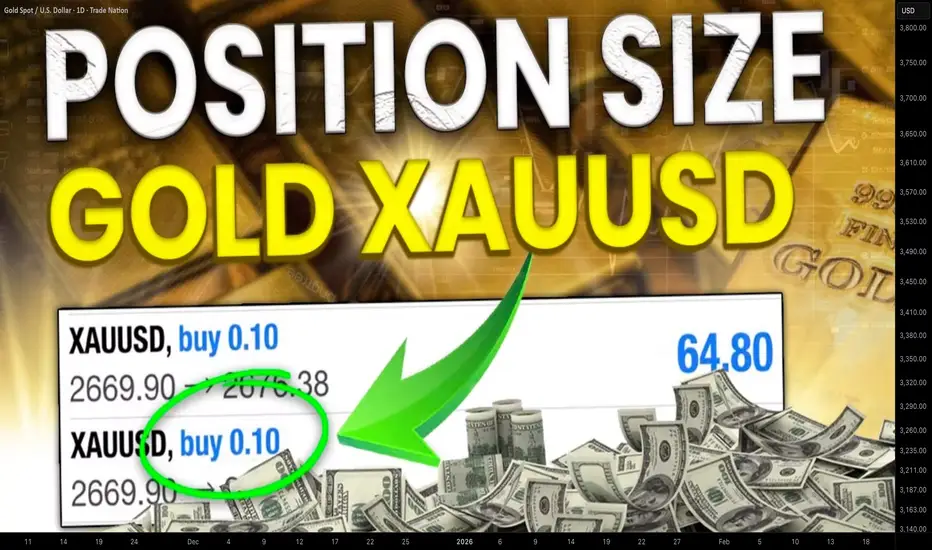

Here is a day trade on Gold.

With a stop loss of 619 pips and a trading account of 10000$,

a lot size for this trade will be 0.02.

If the trade closes on stop loss, total risk will be 100$ or 1% of a trading account.

With a 100$ account, trading with a minimal lot 0.01, your potential risk will be 50$ or half of your trading account.

Check spreads

Spread may dramatically fluctuate on Gold.

High spreads can make it difficult for day traders to catch small price movements, reducing the profit potential of their trades.

Wide spreads can lead to slippage , where day traders may end up buying at a higher price and selling at a lower price than expected, increasing the risk of losses.

Gold has the lowest spreads during London and New York sessions,

while trading the Asian session is not recommended.

Personally, I don't trade Gold if the spread exceeds 100 pips.

In the picture above, you can see a current spread on Gold.

It is 30 pips. It is a relatively low spread, so we can trade.

Don't trade on US holidays

When US banks are closed, liquidity drops substantially on Gold.

It leads to increased spreads and higher probabilities of manipulations,

reduced volatility and very slow market.

For that reason, it is better not to trade Gold during US holidays.

You can easily find the calendar of US banking holidays on Google.

Simply take a break during these trading days.

Don't trade ahead of important US news

US news may dramatically affect Gold prices.

Such events as FOMC or FED Interest rate decision may trigger a high volatility and very impulsive movements.

My recommendations to you is to stay away from trading Gold one hour ahead of the important news releases.

You can find important US news in the economic calendar .

Just sort out the calendar in a way that it would display only significant news and pay attention to them.

Above, you can see the important US news for the coming days in the economic calendar.

Do not open multiple orders

Here is what many Gold traders do wrong:

once they place an order, instead of patiently waiting for a stop loss or take profit being reached, they start opening more orders.

Please, open one single trade per your prediction.

Open a new trade if only you see a new trading setup or your initial trade is already risk-free with a stop loss move to entry level.

Here is the example, a newbie trader decides to buy Gold and opens a long positions.

The market moves in the projected direction, and a trader opens one more trade.

The one can open even dozens of positions like that.

However, the problem is that the market can always suddenly reverse and all these trades will be closed in a loss.

It can lead to a substantial account drawdown.

Open a one single trading position instead.

I truly believe that these trading tips will help you improve your gold trading. Carefully embed these rules in your trading plan and watch how your trading performance improves.

❤️Please, support my work with like, thank you!❤️

I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

A Honest Annual Trading Review: Losses, Lessons, and 2026It’s December 11th, and there are maybe ten real trading days left in the year. At this point, there isn’t much more to do. The market won’t change my year, and I won’t change the market.

So it’s the right moment for an annual review.

I’m not the kind of trader who does weekly or even monthly “performance summaries” that don’t actually mean anything. For me, the only question that matters is this:

With how much did I start the year—and with how much am I ending it?

And after fourteen consecutive positive years, this is the year I end in the red.

So the question becomes: Why?

Why did I lose this year?

Before I dive into the lessons, the mistakes, and the changes I’ll implement starting in 2026, I need to give you some context—because no trading journey exists in isolation.

From 2002 to Today: A Long Road Filled With Luck, Lessons, and Reality

I began trading in 2002, investing in stocks right after the dot-com bubble. And things went incredibly well— not because I was smart, not because I understood markets, but because I had one of the greatest advantages a trader can have:

Perfect timing after a major market collapse.

In other words: pure luck.

In 2004 I discovered Forex, and by 2007 I had shifted entirely to Forex trading.

Until 2009, everything worked almost effortlessly. Every year was green. Even the 2008 crisis was profitable for me—I happened to hold some exceptional short positions.

And then came 2009.

The market didn’t humble me. My own arrogance did.

“ I can’t be wrong. I predicted the 2008 crash. I see the market clearly. I’ve got this.”

That mindset cost me 50% of everything I had accumulated.

That was my first real wake-up call.

It forced me to understand a truth that every long-term trader eventually learns, one way or another:

Humility in front of the market is not optional. It is survival.

That realization became the first major shift in how I approach trading.

What Changed After 2009: A Short Summary of a Long Transformation

As a brief summary of what shifted after 2009—beyond drastically reducing my appetite for risk—the biggest change was my transition toward pure price action and swing trading as the foundation of my approach.

Before that, the market felt almost binary, almost predictable.

- If NFP came in above expectations, the USD strengthened—and it stayed strong, not just for a few intraday spikes.

- When Hurricane Katrina hit, the narrative was straightforward: weak USD.

- Carry trade on JPY was the play all the way until 2008, so buy every substantial dip

- Breakouts were real breakouts—not whatever we have today, with fakeouts layered on fakeouts.

It was a different environment.

Cleaner. More directional. More narrative-driven.

And I traded it exactly as it was.

But markets evolve, and if you don’t evolve with them, you get left behind.

So I adapted.

I shifted from being a trader who reacted to news flows and macro momentum to a trader who reads structure, context, and price behavior first.

I shifted from chasing moves to waiting for high-probability rotations.

I shifted from assuming I understand the market to accepting that the market owes me nothing and can invalidate my ideas at any moment.

There’s much more to say about that transition—how painful it was, how long it took, and how it changed the way I think not just about trading, but about myself. But that’s a story for another time.

For now, it’s enough to say this:

2009 forced me to mature as a trader.

What followed shaped the next decade and a half.

It’s Not About Trump, and It’s Not About Excuses

This isn’t about Trump coming to the White House.

This isn’t about macro narratives or politics.

Yes, the markets did shift around that period — but this article is not about searching for excuses.

Because when it comes to Forex and XAUUSD, I managed the environment just fine.

I adjusted. I adapted. I traded often from instinct shaped by experience, and overall, that part of my trading year held up.

What dragged my year down — completely and undeniably — were my crypto investments.

I Was Never a “To-the-Moon” Guy — And Still Lost Substantially

I’ve never been a moonboy.

I’ve always been realistic with my targets: soft, achievable gains in the 30–50% range.

I never believed in the mythical “altcoin season.” I said repeatedly that it was wishful thinking and that the glory of past cycles would not repeat.

I didn’t gamble on new projects, I didn’t throw money at memes, and I didn’t YOLO into narratives.

And yet — I still lost.

So why?

Because I allocated too much capital, even within my fixed conservative approach.

Not because I believed in altcoin season, but because I believed we would see a meaningful recovery in the autumn.

I sized like someone expecting a bounce.

When the bounce didn’t come, instead, the flash crush from October, the weighting crushed the year( BTW, I wasn't leveraged)

Simple as that.

What I Will Change in 2026 (Crypto Edition)

The fix is straightforward:

- No more long-term investing in crypto, regardless of narrative.

- Maximum time exposure: a few days, maybe a few weeks.

- Stick strictly to major, established projects.

- Trade only what behaves cleanly from a technical perspective.

In other words, crypto will no longer be a long-term play in my portfolio.

It will be treated exactly as I should've be treated it from the beginning:

a short-term speculative instrument — nothing more, nothing less.

Forex and XAU/USD / XAG/USD: The Adjustments Going Into 2026

On the Forex and metals side, the changes are more nuanced — and in some ways, more strategic.

The core shift is this: shorter-term focus, smaller targets on Forex, larger targets on Gold, and a more active approach on Silver.

Here’s the breakdown:

1. Smaller Targets in Forex (EUR/USD as the Example)

In previous years, a 200–250 pip target on EUR/USD was perfectly reasonable.

The volatility allowed it, the market structure supported it, and the flow followed through.

But today, that kind of moves — consistently — is simply not realistic (look at it in the past 6 months).

So the adjustment is straightforward:

From 200–250 pip targets → to sub-100 pip targets.

It’s not about aiming lower.

It’s about aligning targets with actual market behavior, not nostalgia for a volatility regime that no longer exists.

2. Larger Targets on Gold (Because the Volatility Demands It)

Gold is the opposite story.

Volatility has exploded, rotations are massive, liquidity pockets run deep, and intraday swings are two or three times what they used to be.

So the shift here is:

From 300–400 → to 500+ being the new standard.

You can’t trade for 50-100 pips an instrument that behaves like a hurricane.

You adapt to its nature — or it eats you alive.

3. A More Active Approach on Silver (XAG/USD)

Silver has become a much more attractive instrument for me:

- Cleaner technical behavior

- Larger relative percentage moves

- Alignment with Gold, but with more exploitable inefficiencies

So 2026 will include more active trading on XAGUSD, treating it as a strategic middle ground between Forex and Gold volatility.

4. Integrating More ICT/SMC Into My Framework

Another important change is methodological:

I’ll incorporate more ICT/Smart Money Concepts into my analysis and execution.

Not as a religious shift — I’m not replacing classical TA and price action — but as an enhancement.

SMC concepts:

- map exceptionally well onto today’s liquidity-driven markets

- clarify sweeps, inducement, fakeouts

- explain displacement and rebalancing

- blend naturally with the price action approach I already use

In other words, this is not a stylistic change — it’s an upgrade of the internal framework.

Price action stays.

Classical TA stays.

But SMC becomes a bigger part of the decision-making process.

What This All Means for 2026: A Cleaner, Tighter, More Adapted System

When you put all these adjustments together — the crypto restructuring, the refined Forex targets, the larger Gold plays, the increased activity on Silver, and the deeper integration of SMC — the message becomes clear:

2026 won’t be about reinventing myself.

It will be about refining myself.

This year wasn’t a catastrophe ( around 15% loss overall)

It wasn’t an identity crisis.

It was a recalibration — a reminder that longevity in trading is not about perfection, but adaptation.

I didn’t lose because I became worse.

I lost because my allocation in one corner of my portfolio didn’t match the reality of the market.

And the only unforgivable mistake in trading is refusing to learn from the forgivable ones.

The markets haven’t betrayed me.

Crypto hasn’t betrayed me.

Forex and metals haven’t betrayed me.

The responsibility is mine — and so is the path forward.

In 2026, my system becomes:

- Simpler — fewer narratives, more structure.

- Tighter — smaller Forex targets.

- More opportunistic — bigger Gold moves, active Silver plays, short-term crypto speculation.

More aligned with how markets actually behave, not how past versions of me used to trade them.

And that’s the real conclusion of this year:

After almost 25 years in the markets, the only edge that never expires is the willingness to evolve.

Some years, you win because you’re right.

Some years, because you're lucky.

Some years you lose because you’re human.

But the trader who survives is the trader who adapts — again and again, without ego, without excuses.

And that’s exactly what 2026 will be about.

P.S:

And One More Thing… I Kind of Expected This After 14 Years

If I’m being completely honest, part of me always knew this moment would come.

You don’t go fourteen consecutive years without a losing one and expect the streak to last forever.

Statistically, psychologically, realistically — a red year was inevitable at some point.

So no, this wasn’t a shock.

It wasn’t a dramatic fall from grace.

It was simply… the year that was eventually going to arrive.

And that’s actually liberating!:)

Because once you accept that even long-term consistency includes the occasional step backward, you also see the bigger picture clearly:

This year doesn’t define me — the next one will.

Radio Yerevan: Is Crypto the Biggest Wealth Transfer in History?Answer: Yes. But not in the direction people hope.

In the last decade, crypto marketing has repeated one grand promise:

“This is the biggest wealth transfer in human history!”

And in classic Radio Yerevan fashion, this statement is both true and misleading.

Yes — a historic wealth transfer took place.

No — it did not empower the average investor.

Instead, it efficiently moved wealth from retail… back to the very entities retail thought it was escaping from.

Let’s break it down: structured, clear, and with just the right amount of irony.

1. The Myth: A Decentralized Financial Uprising

The early crypto narrative was simple and beautiful:

- The people would reclaim financial independence.

- The system would decentralize power.

- Wealth would flow from institutions to individuals.

The idea was inspiring — almost revolutionary.

Reality check: Revolutions are expensive.

And someone has to pay the bill.

In crypto’s case, the average investor volunteered enthusiastically.

2. The Mechanism: How the Transfer Actually Happened

To call crypto a wealth transfer is not an exaggeration.

The numbers speak loudly:

Total market cap peaked above $3+ trillion.

Most of the profit was extracted by:

- VCs who bought early,

- teams with massive token allocations,

- exchanges capturing fees on every trade,

- and whales who mastered liquidity cycles.

Retail investors, meanwhile, contributed:

- capital,

- liquidity,

- hope,

- hype

- and a remarkable tolerance for drawdowns.

It was, in essence, the perfect economic loop:

money flowed from millions → to a concentrated few → exactly like in traditional finance, only faster and with better memes.

3. The Irony: A Centralized Outcome From a Decentralized Dream

Here lies the great contradiction:

Crypto promised decentralization. Tokenomics delivered centralization.

When 5 wallets hold 60% of a token’s supply, you don’t need conspiracy theories — you need a calculator.

The “revolution” looked more like:

- Decentralized marketing

- Centralized ownership

- Retail-funded exits

- And a financial system where “freedom” was defined by unlock schedules and vesting cliffs

But packaged correctly, even a dump can look like innovation.

4. Why Retail Was Doomed From the Start

Not because people are unintelligent, but because:

- No one reads tokenomics.

- Unlock calendars sound boring.

- Supply distribution charts kill the romance.

- Liquidity mechanics are not as exciting as „next 100x gem”.

- And hype travels faster than math.

In a speculative market, psychology beats fundamentals until the moment fundamentals matter again — usually when it's too late.

5. The Real Wealth Transfer: From “Us” to “Them”

The slogan said:

“Crypto will redistribute wealth to the people!”

The chart said:

“Thank you for your liquidity, dear people.”

The actual transfer looked like this:

- Retail bought the story.

- Institutions created the tokens.

- Retail bought the bags.

- Institutions sold the bags.

- Retail called it a correction.

- Institutions called it a cycle.

Everyone had a term for it.

Only one group had consistent profits from it.

6. So, Was It the Biggest Wealth Transfer in History?

Yes.

But not because it made the average investor rich.

It was the biggest because:

- no previous financial system mobilized so many people

- so quickly

- with so little due diligence

- to transfer so much capital

- to so few beneficiaries

- under the banner of liberation.

It wasn’t a scam.

It wasn’t a conspiracy.

It was simply financial physics meeting human psychology.

7. The Lesson: Crypto Isn’t the Problem — Expectations Are

- Blockchain remains a brilliant invention.

- Tokenization has real use cases.

- DeFi is a groundbreaking paradigm.

- And so on

The issue wasn’t the technology.

It was the narrative that convinced people that buying a token was equivalent to buying financial freedom.

Real freedom comes from:

- understanding liquidity,

- reading tokenomics,

- respecting supply dynamics,

- and asking the only question that matters:

“If I’m buying… who is selling?”

In markets — especially crypto — this question is worth more than any airdrop.

8. Final Radio Yerevan Clarification

Question: Will the next crypto cycle finally deliver the wealth transfer to the masses?

Answer: In principle, yes.

In practice… only if the masses stop donating liquidity.

How to Use ATR in TradingViewMaster ATR using TradingView's powerful charting tools in this step-by-step tutorial from Optimus Futures.

ATR, or Average True Range, is a volatility indicator that helps traders measure market movement, set appropriate stop losses, and adjust position sizing based on current market conditions.

What You'll Learn:

Understanding ATR as a volatility measurement tool that tracks price movement regardless of direction

How ATR calculates the average range between highs and lows over a specified period — typically 14

Why rising ATR signals increasing volatility and larger price swings

Why falling ATR indicates decreasing volatility and quieter market conditions

Using ATR to set dynamic stop losses that adjust to current volatility rather than arbitrary dollar amounts

How to calculate stop distances by multiplying ATR by factors like 2x or 3x

Applying ATR for position sizing to maintain consistent risk across different volatility environments

Setting profit targets based on ATR multiples to align with actual market movement

Filtering trade setups using ATR levels to avoid low-volatility periods or confirm breakout momentum

How to add ATR on TradingView via the Indicators menu

Understanding the default 14-period setting and how shorter or longer periods affect responsiveness

Practical examples using the E-mini S&P 500 futures chart

Applying ATR across daily, weekly, and intraday timeframes for risk management and trade planning

This tutorial is designed for futures traders, swing traders, and risk-focused analysts who want to integrate volatility-based risk management into their trading approach.

The methods discussed may help you set smarter stops, size positions appropriately, and adapt your trading strategy to changing market conditions across multiple markets and timeframes.

Learn more about futures trading with TradingView: optimusfutures.com

Disclaimer

There is a substantial risk of loss in futures trading. Past performance is not indicative of future results. Please trade only with risk capital.

We are not responsible for any third-party links, comments, or content shared on TradingView. Any opinions, links, or messages posted by users on TradingView do not represent our views or recommendations.

Please exercise your own judgment and due diligence when engaging with any external content or user commentary.

This video represents the opinion of Optimus Futures and is intended for educational purposes only. Chart interpretations are presented solely to illustrate objective technical concepts and should not be viewed as predictive of future market behavior.

In our opinion, charts are analytical tools, not forecasting instruments.

Risk Management Basics 95% of Traders IgnoreWhen traders try to improve their results, they often jump straight to indicators, new setups, or refined entries.

But here’s the uncomfortable truth:

Most traders don’t fail because of their strategy — they fail because they don’t control their risk.

Let’s break down the two fundamentals that separate professionals from the 95%:

1️⃣ The 1% Rule: Your Built-In Survival System

Most beginners risk 5–20% per trade.

Professionals risk a maximum of 1%. Why?

Because the goal isn’t to win every trade — the goal is to stay in the game long enough for your edge to play out.

Risking only 1% means:

✔ A losing streak won’t destroy your account

✔ Your emotions stay stable and rational

✔ Your system has room to unfold statistically

✔ You avoid the #1 account killer: overexposure

Here’s the key mindset shift:

Risk management is not about fear — it’s about increasing your probability of long-term profitability.

2️⃣ Positive Expectancy: The Math Behind Winning Traders

Most traders judge a setup based on the last one or two trades.

Professionals evaluate it based on expectancy — the average profit per trade across a large sample.

Here’s a simple example:

Win rate: 40%

Average win: +60 pips

Average loss: –30 pips

Expectancy =

(0.4 × 60) – (0.6 × 30) = +6 pips per trade

Meaning:

You can lose more trades than you win — and still be profitable.

This is the principle beginners never understand.

A system with positive expectancy + 1% risk per trade becomes extremely powerful.

You stop caring about individual losses and start thinking in probabilities, not emotions.

The Truth Most Traders Miss

➡️ Risk management is the strategy.

➡️ Expectancy matters more than your win rate.

➡️ Risking 1% won’t make you rich fast — but it will prevent you from blowing up.

➡️ Trading becomes easier when you remove the illusion of certainty.

If traders spent more time understanding expectancy and risk instead of chasing “perfect setups,” half of their frustration would disappear overnight.

Thanks for reading — and have a disciplined start to your trading week!

If you found this post valuable, let me know in the comments.

I might create a full series on applied risk management and expectancy modeling.

Jonas Lumpp

Speechless Trading

Disclaimer: This tutorial is for educational purposes only and does not constitute financial advice. Its goal is to help traders develop a professional mindset, improve risk management, and make more structured trading decisions.

AI Revolution: How the Retail Trader Can Finally WinA step-by-step guide for traders who want to stop staring at charts and start letting AI do the heavy lifting.

For years, trading meant one thing:

Sit at your desk.

Stare at charts.

Wait.

Hope.

React.

Repeat.

But in 2025, that’s ancient history.

AI has changed everything.

Now any retail trader — even a complete beginner — can create a TradingView strategy, test it, refine it, and fully automate execution to MT5 or cTrader using webhooks… without writing a single line of code.

If you can type instructions, you can build an automated trading system.

Here’s the full blueprint — updated with the crucial Step 0 that most people don’t even know exists.

⭐ STEP 0 — Build Your Master AI Prompt (The Secret Weapon)

Before you write a single strategy rule…

Before you ask AI to code…

Before you try to automate anything…

You MUST build a Master Prompt.

This is the “operating system” for the AI — it tells the model:

how to write the Pine Script

how to structure entries & exits

how to format alerts

how to avoid compile errors

how to respond when you paste broken code

how to preserve your logic perfectly

Without a Master Prompt, AI guesses.

With a Master Prompt, AI produces clean, professional, error-free trading systems consistently.

Here’s the master prompt you’ll use:

🔥 MASTER PROMPT (Copy + Paste Into ChatGPT Before Giving Your Strategy Rules)

You are now my expert TradingView Pine Script v5 strategist, quant developer, and compiler-level debugging assistant.

Your job is to:

1. Build a complete TradingView strategy() script based on the rules I give you.

2. Ensure the script compiles with ZERO errors.

3. Write clean, structured, commented code using professional conventions.

4. Include:

– strategy.entry()

– strategy.exit() with SL & TP

– Input parameters

– alertcondition() for webhook automation

5. Structure alerts so they work with strategy.order.action.

6. NEVER change my trading logic. Follow it EXACTLY.

7. If the code fails to compile:

– Identify the REAL root cause

– Fix only what’s necessary

– Return a fully corrected script

8. When I ask for improvements, optimize the code without altering the core idea.

After loading this master prompt, wait for my rules before generating the strategy.

Now your AI assistant is fully “trained” before it begins coding.

Once Step 0 is done?

The real fun begins.

🚀 STEP 1 — Decide What You Want Your Strategy To Do

Define the basics:

What triggers your entry?

What ends the trade?

What confirms the setup?

How much risk?

Example simple idea:

Buy when price closes above the 20 EMA after RSI oversold.

Sell when price closes below the 20 EMA after RSI overbought.

Stop = 1 ATR.

Take profit = 2 ATR.

Once you define this?

You're ready for the AI to code it.

🤖 STEP 2 — Use AI to Turn Your Idea Into a TradingView Strategy

Paste your Master Prompt.

Then paste your rules.

Example instruction:

“Build the strategy using my Master Prompt.

Here are the rules…”

AI outputs a ready-to-paste Pine Script.

If it errors?

You tell it:

“Fix all compile errors without changing my trading logic.”

This is the magic of Step 0 — the AI already understands exactly how to fix your code properly.

📊 STEP 3 — Backtest Directly on TradingView

Paste the script.

Add to chart.

Open Strategy Tester.

Check:

Win rate

Drawdown

Profit factor

Stability

Number of trades

If it sucks?

Ask AI:

“Improve this strategy’s performance. Keep the overall concept but add filters.”

AI gives you Version 2.

⚙️ STEP 4 — Turn Your Strategy Into Webhook Alerts

Click Alerts → Condition → Your Strategy Name

Choose:

Strategy Entry Long

Strategy Exit Long

Strategy Entry Short

Strategy Exit Short

Turn on Webhook URL.

Use structured JSON:

{

"signal": "{{strategy.order.action}}",

"symbol": "{{ticker}}",

"price": "{{close}}",

"position_size": "0.10"

}

Now TradingView is alert-ready.

🌐 STEP 5 — Send Alerts to MT5 or cTrader Using Webhooks

You need a bridge.

Best options:

PineConnector

TradeConnector

cTrader Open API bot

Make/Zapier → Python Server → MT5 EA

Example webhook:

{

"action": "BUY",

"symbol": "XAUUSD",

"lot": 0.10,

"sl": 50,

"tp": 100

}

🧠 STEP 6 — Use AI to Build the MT5 or cTrader Execution Robot

If you want a custom bot instead of PineConnector:

Ask:

“Write an MT5 EA that receives webhook commands in JSON format and executes market orders with SL and TP.”

Or:

“Write a cTrader cBot that listens for webhook signals and places trades automatically.”

AI builds your execution engine.

🔁 STEP 7 — Your Fully Automated Trading Pipeline

STEP 0 — Build your Master AI Prompt

STEP 1 — Define your strategy

STEP 2 — AI generates TradingView strategy

STEP 3 — Backtest & refine

STEP 4 — Create alert webhooks

STEP 5 — Bridge → MT5/cTrader

STEP 6 — AI builds execution bot

STEP 7 — Enjoy hands-free AI-powered trading

🎯 Final Thoughts — This Is the New Era

The trader who wins is the one who:

uses AI

automates everything

removes emotion

builds systems, not guesses

executes consistently

Tools like TradingView + AI + MT5/cTrader automation are the biggest level-up in retail history.

And it all starts with:

STEP 0 — Build your Master Prompt.

Let the fun begin

Get Funded and make $20 000 Monthly. Complete plan for 2026.Hey traders let's have a look at prop trading again. It's a great opportunity for the skilled traders who has good strategy, discipline and mastered risk management. Let's start with the numbers which many traders and misunderstood.

📌 Prop firm facts

- $100K account with 10% max drawdown means you got $10K account, not $100K

- Goal of 10% to pass phase 1 while you can risk 10% means 100% gain

- Goal of 5% to pass Phase 2 while you can risk 10% adds another 50% gain.

- You will literally be funded after making 150% not 10% and 5%

⁉️ Does it mean it's impossible to get funded ?

Yes it's possible, next to good strategy you need, discipline and mainly you just need to adjust your risk management. If you make 150% in year as a Hedge fund manager you will be a superstar trader. Yet people still want to pass prop challenge in a less than week or in a few trades which means not sticking to the risk management.

🔗 Click to the picture below to Learn more about Prop Risk management 📌 How to make $20 000 a month ? Magic of 3%

Yes, you actually need to make only a 3% a month. Is it difficult ? No, It's not. You need 3 wins with 1:2 RR while risking 0.5% Risk.

1️⃣Your Ultimate goal - -$100K Funded account - 3% Gain - 80% Profit split = $2400 Payout

2️⃣Let's take it to $20 000 a Month

Don't try to increase your % gains per month, increase your capital under management

- Get another 4 x $ 100K Challenges pass them - You will have $500K AUM:

- $ 500 000 - 3% Gain - 80% Profit split = $12 000

3️⃣Reinvest buy another 3 - 5 challenges aim for $ 1000 000 funded across few solid props firms. 🎯 $ 1000 000 - 3% gain - 80% Profit Split = $24 000 Payout

📌 Have a long term plan

this is not gonna happen in few months. It's a year plan - But you got this... 💪

With approximate cost of $500 - $600 per $100K challenge you will need to spend apron. $5500 to get $1000 000 funding. You will fail some, its unavoidable, so let's count with more might $10K. But still , you can start with first $100K an then reinvest to another challenges. You dont need $10K investment right now. But later this $10K and 3% gain and 80% profit split is $24 000, even more then $20K.

📌 Difficulty is not technical, but in patience

I speak from experiences that my biggest mistakes was trying to pass quickly or when I was in drawdown I started to gamble. Be patient and stick to the rules. If we stick to 3% a month without progressive risk management it would be 4 months to get funded. If you do progressive risk management you can do it faster, and once you are confident you can run multiple challenges at the same time.

📌 Long term plan requires perfect planning

Find 60 minutes just for yourself and this about these questions below, write the answers to to the paper, think about the execution of your project. I know you didn't do it now, but come back to this and do it again. You need to visualize your future successful yourself and remind that visualization every day. I recommend a book - Psycho-cybernetics from Maxwell Maltz it will help you define your self-image of successful trader in the fact this book will change your life.

📌 Essential Rules for Prop Trading

-Its not a straight forward game

-Reduce number of trades - Only A+ Setups

- Grow Your Capital Under management in multiple firms not % gains

- 3% is a golden profit in prop space to live from trading

❌ Dont do this

If you don't trade well on small account, getting prop firm will not change it.

Don't expect it to be a solution to bad financial situation. It's extension. 🧪 Trading is not hard we often overcomplicate it

I believe you already few great trades in a month, but you also have many unnecessary ones, look at your last few month results and check if would be able to make 3% if you excluded those unnecessary trades. I sure you could ant thats what you have to do